Spur Corporation Limited (JSE: SUR), a South African restaurant franchisor known for its family-friendly brands like Spur and John Dory’s, recently reported a strong financial performance for the first half of 2024. Revenue and profit both increased year-over-year, driven by growth in the core Spur brand and other franchise businesses. The company also successfully acquired Doppio Collection, expanding its portfolio and strengthening its market position.

Looking ahead, Spur Corporation acknowledges the challenging economic climate and is taking proactive steps to mitigate supply chain disruptions and capture market share through innovative customer relationship management strategies and a continued focus on exceptional service and product quality. With its resilient business model and experienced leadership team, Spur appears well-positioned to navigate the uncertain market environment and deliver sustainable growth for its shareholders.

Technical

Spur displays a promising technical outlook on the 1-day chart, signalling potential recovery after a two-day decline. Trading around the 23.60% retracement level and the 50-SMA, the share price demonstrates resilience. The 100-SMA (orange line) and 200-SMA (red line) provide additional support, while the 50-SMA (blue line) acts as a current hurdle. Notably, the shorter-term 50-SMA holds a favourable position above both the 100-SMA and 200-SMA, indicating positive momentum.

The Relative Strength Index (RSI) at 53.46, trending upwards after surpassing the 50.00 level, further supports the bullish sentiment. Therefore, a sustained push above the 23.60% retracement level and the 50-day SMA could lead to a test of the 3,149 cents resistance level. A successful bridge of the initial resistance on significant volume could trigger a run, with the 7-year high of 3,299 cents (green horizontal line) at a discount of 2.03% from the company’s discounted cash flow estimated fair value of 3,366 cents (blue line) acting as the next significant level higher.

However, failure to sustain a push above the 23.60% Fibonacci retracement level would leave the dynamic support and the 38.20% Fibonacci retracement level (2,898 cents) next in play. A break below the initial 38.20% Fibonacci retracement level on significant volume would leave the 50.00% Fibonacci retracement level (2,774 cents) and 61.80% Fibonacci retracement level (2,651 cents) within the bears’ reach in the near term.

Fundamental

Spur Corporation, the South African restaurant powerhouse behind brands like Spur and John Dory’s, recently reported a seemingly positive financial performance for the first half of fiscal 2024. Revenue and profit both witnessed growth, but a closer examination reveals a nuanced picture for potential investors.

Profitability with Nuance

While headline figures boast growth, a deeper dive unveils factors influencing profitability. The gap between profit before tax and operating profit stems from non-cash adjustments like depreciation and IFRS charges. Additionally, a closer look at cash flow reveals an outflow of R74.7 million due to working capital movements. This outflow is partially driven by increased inventory to meet festive season demand and higher accounts receivable reflecting December trade. These factors highlight the company’s efforts to manage short-term cash flow while investing in future growth.

It is worth mentioning that Spur Corporation’s financial health is robust, boasting R288 million in unrestricted cash, providing a solid foundation for future investments and operational needs.

Doppio Acquisition and Growth Ambitions

Spur Corporation’s recent acquisition of Doppio Collection, a coffee shop chain, signals its intent to diversify beyond its core restaurant offerings. The R122 million acquisition, valued at a 4.5x EBITDA multiple, signifies confidence in the potential of this new venture. Furthermore, the company’s ambitious plans to open 53 new restaurants in the current fiscal year underscore its commitment to geographical expansion and market share growth.

Navigating Uncertainties

Spur Corporation acknowledges the unpredictable market conditions, particularly concerning consumer spending. The company is proactively mitigating supply chain challenges and has identified four key drivers for growth:

- Tech-driven sales activation: Leveraging technology to boost sales through targeted marketing and customer engagement.

- Enhanced customer relationship management: Building stronger relationships with customers through loyalty programs and personalized experiences.

- Continuous restaurant and product innovation: Keeping menus and dining experiences fresh and exciting to attract and retain customers.

- Best-in-class customer service: Delivering exceptional service to create loyal brand advocates.

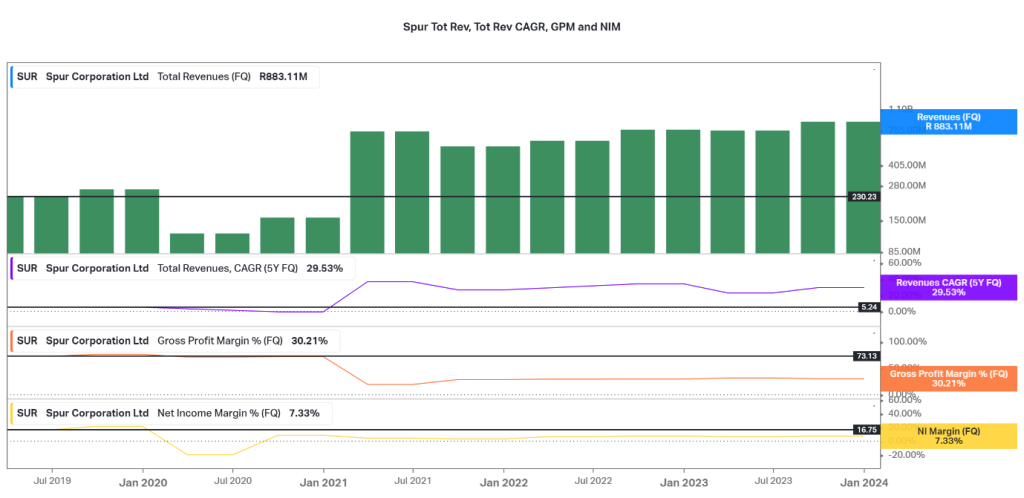

The picture above shows that the corporation’s recent financial performance presents a contrasting picture. Revenue growth shines brightly, boasting a five-year compound annual growth rate (CAGR) of 29.53%, exceeding the performance of major South African indices. This suggests strong demand for Spur’s offerings and potential for future market share gains.

However, a shadow lurks in the form of declining profitability margins. Both gross and net income margins have fallen significantly, raising concerns about the company’s ability to translate revenue growth into sustainable profits. This decline could be attributed to rising input costs, increased competition, or inefficiencies in operations.

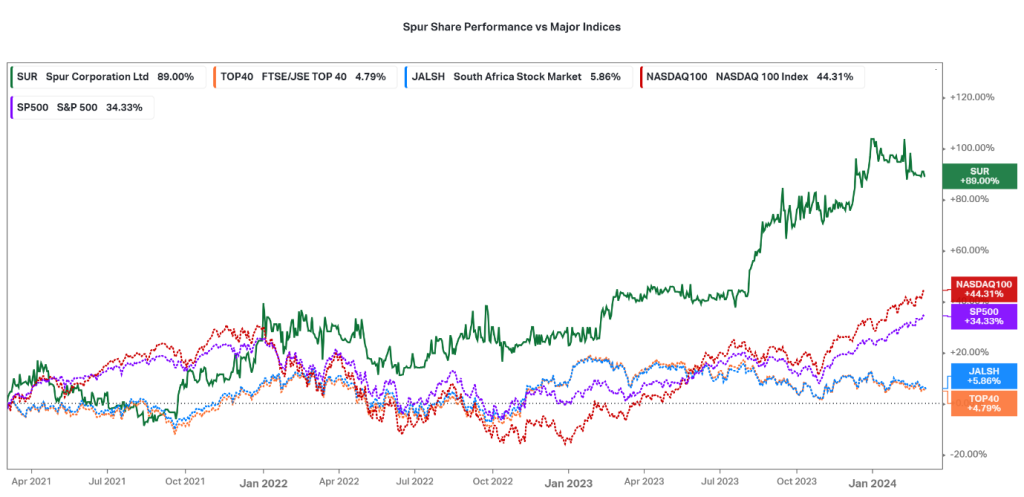

The picture above also shows that while Spur’s three-year total return is an impressive 89%, its recent performance has been less inspiring. Year-to-date, the share price has declined 7.19%, underperforming the JSE Top 40 Index’s 6.56% dip. This suggests cautious market sentiment, with investors likely waiting to see if Spur can address its profitability concerns and translate its top-line growth into sustainable financial performance.

Comparing Spur’s performance against major international indices like the Nasdaq 100 and S&P 500 reveals a similar trend of underperformance year-to-date, indicating broader market concerns about the company’s ability to navigate the current economic climate.

Looking ahead, Spur Corporation aligns its strategic initiatives with an evolving market, emphasizing resilience and nimbleness in response to unpredictable short- and medium-term scenarios. The plan to open 41 new restaurants in South Africa and 12 internationally by the end of fiscal ’24 demonstrates ambitious growth targets. In a consumer spending landscape where additional funds are limited, Spur focuses on robust sales activation, tech-led customer relationship management, and innovation, recognizing that market share growth hinges on exceptional customer service, product quality, and added value.

This forward-looking approach positions Spur Corporation Limited as an exciting prospect for investors seeking exposure to a well-managed, innovative company in the dynamic restaurant industry.

Summary

Spur Corporation Limited (JSE: SUR) demonstrates robust growth with a compelling 29.53% Total Revenue CAGR. Strategic acquisitions, like the Doppio Collection, enhance its market presence. Despite margin adjustments, Spur’s proactive expansion plans and resilience in legal matters position it optimally. Technical analysis suggests short-term opportunities, making Spur a stock to watch. In a market driven by innovation, Spur’s focus on sales activation and tech-led CRM sets a promising trajectory for the company, even though but downside risks remain.

Sources: TradingView, MarketScreener, Reuters, Spur, Timeslive, Bloomberg.

Piece written by Mfanafuthi Mhlongo, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd (hereinafter referred to as “Trive SA”), with registration number 2005/011130/07, is an authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act, 37 of 2002. Trive SA is authorised and regulated by the South African Financial Sector Conduct Authority (FSCA) and holds FSP number 27231. Trive Financial Services Ltd (hereinafter referred to as “Trive MU”) holds an Investment Dealer (Full-Service Dealer, excluding Underwriting) Licence with licence number GB21026295 pursuant to section 29 of the Securities Act 2005, Rule 4 of the Securities Rules 2007, and the Financial Services Rules 2008. Trive MU is authorized and regulated by the Mauritius Financial Services Commission (FSC) and holds Global Business Licence number GB21026295 under Section 72(6) of the Financial Services Act. Trive SA and Trive MU are collectively known and referred to as “Trive Africa”.

Market and economic conditions are subject to sudden change which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. Trive Africa and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered. Please consider the risks involved before you trade or invest. All trades on the Trive Africa platform are subject to the legal terms and conditions to which you agree to be bound. Brand Logos are owned by the respective companies and not by Trive Africa. The use of a company’s brand logo does not represent an endorsement of Trive Africa by the company, nor an endorsement of the company by Trive Africa, nor does it necessarily imply any contractual relationship. Images are for illustrative purposes only and past performance is not necessarily an indication of future performance. No services are offered to stateless persons, persons under the age of 18 years, persons and/or residents of sanctioned countries or any other jurisdiction where the distribution of leveraged instruments is prohibited, and citizens of any state or country where it may be against the law of that country to trade with a South African and/or Mauritius based company and/or where the services are not made available by Trive Africa to hold an account with us. In any case, above all, it is your responsibility to avoid contravening any legislation in the country from where you are at the time.

CFDs and other margin products are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how these products work and whether you can afford to take the high risk of losing your money. Professional clients can lose more than they deposit. See our full Risk Disclosure and Terms of Business for further details. Some or all of the services and products are not offered to citizens or residents of certain jurisdictions where international sanctions or local regulatory requirements restrict or prohibit them.