Troubled by recent events by Sibanye Stillwater Limited, the miner has been given a poor hand as the share price has fallen. The company has gone through a period of bad luck and has been affected by theft, load shedding, strikes in South Africa, and floods in Montana, United States of America. Platinum Group Metals, Gold, and other minerals have historically been the primary sources of income for Sibanye-Stillwater, a gold and platinum miner with a comprehensive portfolio of operations and assets spread over five continents. PGM production at Sibanye is responsible for roughly 50% of sales and 75% of earnings. At the article’s writing, the company has not released its interim results.

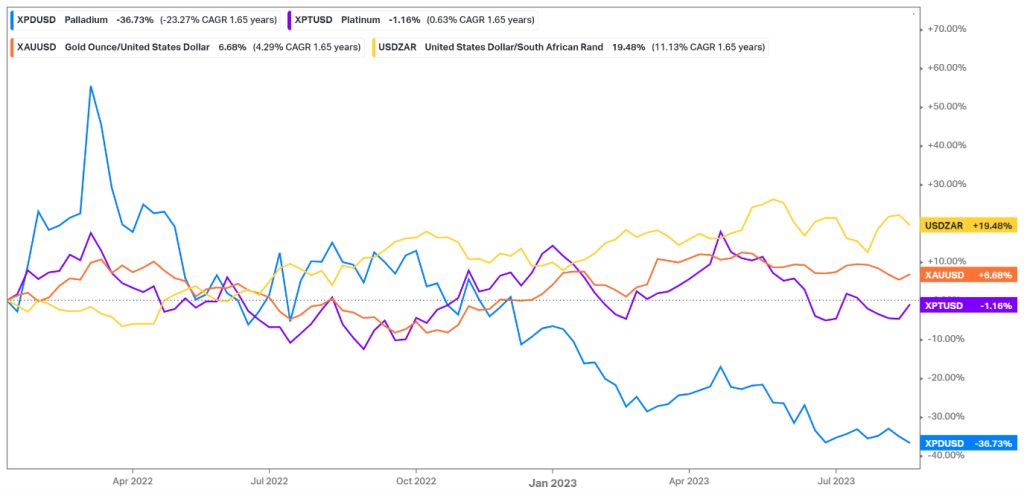

Figure 1: Performance of Platinum, Palladium, Gold, and the USDZAR cross

Starting from the beginning of 2022, the price movements of commodity prices have been a roller coaster ride. PGMs have been in the red over the period that started in 2022, and in the same period, the rand against the greenback has weekend by nearly 20%. While gold prices have remained stable between $1900 and $2000 throughout 2023, the price of palladium has been falling.

Technical

Figure 2: Daily candle stick chart for Sibanye Stillwater Limited since the beginning of 2022

Since February 2022, when the price was approximately R78 per share, the share price has dropped precipitously. From May 2022 to May 2023, the price movement was also in a channel between R36 and R52. The share price declined the next month, reaching the new range between R28.50 and R36. If we narrow our gaze slightly, a double bottom played out to completion in July of this year. Taking a step back, from the start of June to the present, another double-bottom pattern may develop.

Using the indicators, we can see that the candlestick ended above the 50-day exponential moving average following yesterday’s trading session and that the 200-day moving average is comfortably distant should the price decide to challenge it. The MACD also shows some intriguing signs, with the signal line pointing upward and both MACD moving averages just below the neutral line but aiming to cross it.

Fundamentals

Operational issues

At Sibanye’s Stillwater mine in Montana, severe floods in June delayed operations for seven weeks, resulting in a 23% drop in production from the previous year. Sibanye’s South African gold operations saw a 63% decrease in production, primarily due to a wage strike between March and June. Sibanye dug in its heels as it realized that every percentage point in salary increases surrendered now adds up to a potentially fatal blow to the company’s future. In its gold operations, wages make up around 50% of overall costs, and in its more fully mechanized PGM businesses, they make up about 40%.

Notwithstanding power outages, cable theft, and safety-related stoppages, production from the SA PGM facilities was somewhat lower than anticipated for 2022. Platinum group metal (PGM) production in South Africa could decrease by as much as 20% this year as unstable power supplies impact processing capacity.

After deciding to stop operating the loss-making mines, the JSE-listed miner completed Section 189 consultations in 2023. Of the approximately 2,000 job cuts that Sibanye-Stillwater had initially anticipated, 168 employees will be let go when it closes operations at its Beatrix and Kloof shafts. However, 1 136 of those employees chose to be reassigned to other positions within the firm in South Africa. Due to infrastructural damage, Sibanye Stillwater has stopped mining at its South African Kloof 4 shaft, which accounts for 14% of the miner’s gold output.

Opportunities

Following the acquisition of an initial investment in February, the diversified South African miner gained control of the Finnish manufacturer of battery chemicals Keliber last October when it increased its shareholding to 85%. The business will begin with building a lithium hydroxide refinery in the Kokkola Industrial Park in Finland, from which the company intends to supply the European battery market. In order to jointly develop the Rhyolite Ridge lithium project in the United States, Sibanye has partnered with Loneer of Australia. After completing a favourable Feasibility Study, the Finnish Keliber Project was given the go-ahead to begin construction. Due to our rise in Keliber ownership to 84.96% (2021: 26.6%) and successful exploration, there is a 248% increase in Li mineral resources.

The competition to supply battery metals to the expanding electric vehicle industry is highlighted by Sibanye Stillwater’s 2021 agreement to pay $1 billion in cash for nickel and copper mines in Brazil. A crucial ingredient in lithium-ion batteries is nickel, often used to manufacture stainless steel.

The latest results are still to be released to show how the company has weathered the storm in the first half of the financial year. The company did release a trading statement on the 18th of August. It stated that they expect a drop in the EPS of between 35% and 42% due to a 22% decline in PGM prices, lower production, and higher unit costs from the US PGM operations.

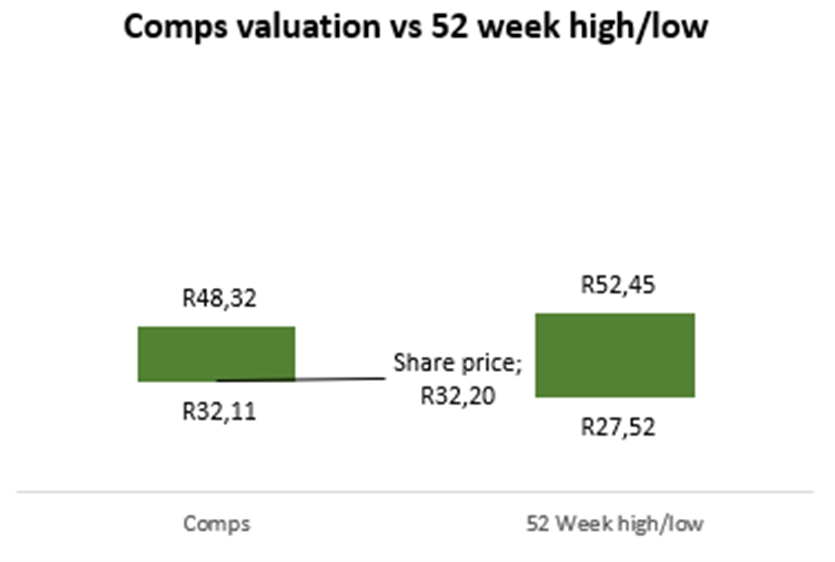

Figure 3: Comparative valuation analysis for Sibanye Stillwater Limited

The comparative valuation analysis shows some upside for the company’s share price if you look at the EV/Revenue ratio. The target of the ratio is R48.32, whereas EV/EBIT and the P/E ratio are around R32.

Summary

The business is in sound shape but has had an unfortunate turn with many issues that have occurred to slow its momentum. If the organization manages the storm well, there are still plenty of opportunities for the business to seize. Strengthening the role of investment commodities in the global monetary system, commodity applications, and energy solutions to combat climate change and the environment are some potential the company has recognized.

Sources: Sibanye Stillwaters; MoneyWeb, Business Day; KoyFin and TradingView

Author: Odwa Magwentshu

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.