The alcoholic beverages industry boasts a substantial economic presence, recording a noteworthy revenue of €1,029.0 billion in 2022, according to Statista. Within this dynamic sector, Anheuser-Busch InBev and Diageo PLC emerge as prominent entities, each distinguished by its unique product portfolio, thereby securing a significant presence in the global markets.

Anheuser-Busch InBev, recognized as the largest global brewer, engages in the production, manufacturing, marketing, and sale of a diverse array of beers and beverages spanning an extensive portfolio of approximately 500 brands. Among its notable global brands are Budweiser, Stella Artois, and Michelob Ultra, supplemented by other well-known labels such as Beck’s, Hoegaarden, Leffe, Bud Light, Castle, Modelo, and Skol.

In contrast, Diageo PLC, while also involved in the production, marketing, and sale of beer, is more prominently established in the spirits market. Its offerings encompass a comprehensive selection of scotch, gin, vodka, rum, liqueur, wine, and tequila, featuring renowned brands like Johnnie Walker, Guinness, Tanqueray, Baileys, Smirnoff, Captain Morgan, and Don Julio.

Both Anheuser-Busch InBev and Diageo PLC wield global influence, standing as formidable leaders within the alcoholic beverage sector. The exploration of their respective strengths and characteristics serves as a key aspect in understanding their individual contributions to this thriving industry.

Industry Breakdown

According to an analysis done by Statista, the alcoholic drinks market is expected to grow with a compound annual growth rate (CAGR) of 4.12% from 2023 through 2028. Notably, the largest segment within this market is the Spirits market, which is dominated by Diageo and holds a market volume of €375.7Bn in 2023. In addition to this, the consumer trend within the market revolves around the increased demand for unique and premium beverages, which has boosted the demand for craft beers and spirits. While the average volume per person in the alcoholic beverage market is expected to reach 28.61L this year, volume growth is expected to grow at a mere 2% in 2023. This has led to a certain level of divergence in the share price of AB InBev, which has a portfolio highly concentrated in beer, compared to Diageo, which has a more diversified portfolio in terms of product type. Over the last 20 years, both companies have appreciated significantly in value, with AB InBev realizing an 182% price appreciation, while Diageo has reigned supreme with a 285% expansion. While AB InBev has dealt with company-specific events that have dented its share price over recent years, certain macroeconomic events have strained the industry, most notably the COVID-19 pandemic, as well as the recent inflation surge, which has dented the consumer’s disposable income, and reduced the demand for non-essential goods, such as alcohol.

Source: Trive – Koyfin, Tiaan van Aswegen

Size and Global Reach

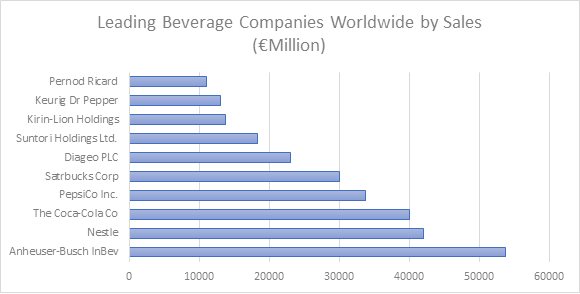

In terms of size, AB InBev reigns supreme. With its market cap of €116.64Bn, it stood tall as the leading beverage company worldwide by sales, as seen in the chart below, with sales over €53Bn in 2022. The company was founded in 2008 before the acquisition of SABMiller in 2015 expanded its brand portfolio. As the world’s largest brewer, the company produced 595 million hectolitres of beer in 2022, and due to its size, the company controls over 40% of the American beer market with its brands. However, this presence is threatened by the entrance of smaller brands and the emergence of craft beers that have integrated themselves into the market. On the other hand, Diageo falls in the top ten leading beverage companies by sales as well, despite having a much smaller market cap of around €73.72Bn.

Source: Trive – Statista, Tiaan van Aswegen

Geographic Diversification

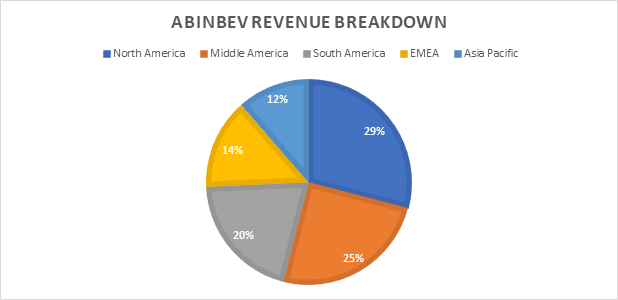

Due to its global reach, both companies are well diversified geographically, minimizing country-specific risk on their operations. The chart below depicts North America as the biggest revenue contributor for AB InBev, with 29%, while Middle America contributes an additional 25%. Along with the 20% contribution from South America, its top three geographies account for 74% of its revenue, while EMEA and Asia Pacific account for the remainder.

Source: Trive – Anheuser-Busch InBev SA/NV

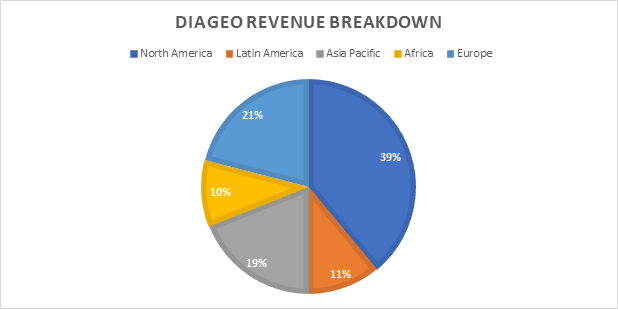

While Diageo is well diversified as well, its top three regions account for 80% of its revenue, and the company is a lot more reliant on its North American and European businesses. However, it holds a large exposure to the fast-growing Asia Pacific region, which could benefit its growth trajectory as we advance. On the downside, its Latin American business is facing severe headwinds, and in its latest half-year earnings, the company acknowledged an expected slump in demand from its business in that geography.

Source: Trive – Diageo PLC, Tiaan van Aswegen

Summary

While Anheuser-Busch InBev and Diageo are not direct competitors in terms of their product portfolios, they both stand as the market leaders in their respective segments and, therefore, face off in the fight for global market share in the alcoholic beverage industry. AB InBev, with its sheer size and dominant market positioning, remains well diversified in its geographic and brand exposure, while Diageo has its foot firmly placed in the faster-growing spirits market, making for an intriguing battle between brews and spirits in the lucrative alcoholic beverage market.

Sources: Koyfin, Statista, Anheuser-Busch InBev SA/NV, Diageo PLC

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.