The South African retail sector, a pivotal player in the nation’s economy, faces a complex web of challenges and opportunities.

Despite being the third-largest sector in the country, recent hurdles have impeded its growth trajectory. Eskom’s power disruptions have cast a shadow, dampening the sector’s momentum. Compounding this, the ripple effects of the Russia-Ukraine conflict have reverberated through supply chains, fostering inflationary pressures that have tested consumer resilience.

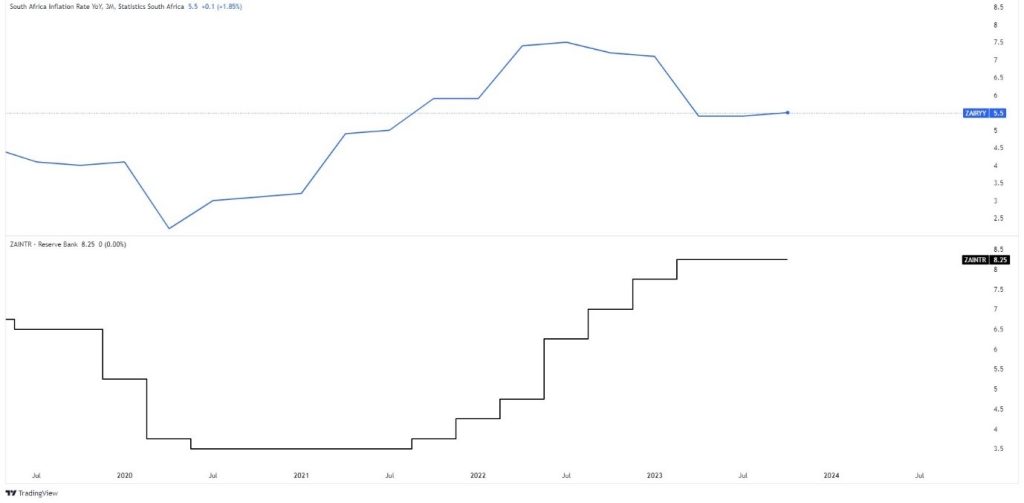

Stats SA’s report revealed a concerning trend, with a second year-on-year retail sales decline of 0.9% in June 2023. However, a silver lining emerges amidst these challenges. With South Africa’s inflation cooling to 5.5% from a peak of 7.63% YoY in Q3 2022, potentially signalling a plateau in interest rates, a hopeful window materializes. This shift might empower consumers, fostering improved spending habits and potentially revitalizing the retail landscape.

Source: Trive – TradingView, Nkosilathi Dube

Technical

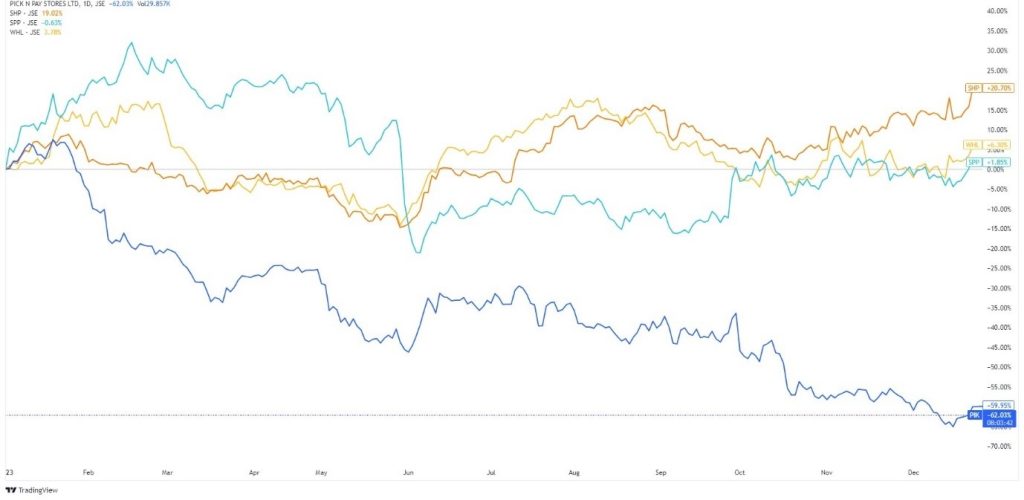

Among the major South African retail stocks serving the food retail market, giants like Pick n Pay (PIK), Shoprite (SHH), Spar (SPP), and Woolworths (WHL) witnessed a tumultuous first half of 2023, with investor confidence waning amidst declining market values.

The sector grappled with subdued consumer spending amid soaring inflation and elevated interest rates, triggering a notable sell-off. However, the latter half of the year painted a different picture. These stocks staged a noteworthy rebound, marking gains ranging between 1% and 20% for most, except for the outlier, Pick n Pay, which shed nearly 60% of its market value and stood apart from the pack.

Source: Trive – TradingView, Nkosilathi Dube

Fundamental

Pick n Pay, a significant player in South Africa’s grocery landscape, weathered a formidable storm with a staggering 60% share plunge in 2023, stemming from a nearly R600 million loss in the half year of fiscal 2024.

The company found itself grappling amidst cutthroat competition, trailing behind retail giants Shoprite and Woolworths. These industry leaders tactfully utilized discounts and precise targeting strategies, bolstering consumer spending on their offerings and further squeezing Pick n Pay’s market standing.

Amidst a challenging landscape, Pick n Pay faced multifaceted hurdles. The burden of record-breaking load shedding, escalating operational costs, and a staggering 14% food inflation marked the highest in 14 years. Concurrently, interest rates surged to their highest point since 2009, amplifying pressures on already strained customers.

Source: Trive – Koyfin, Nkosilathi Dube

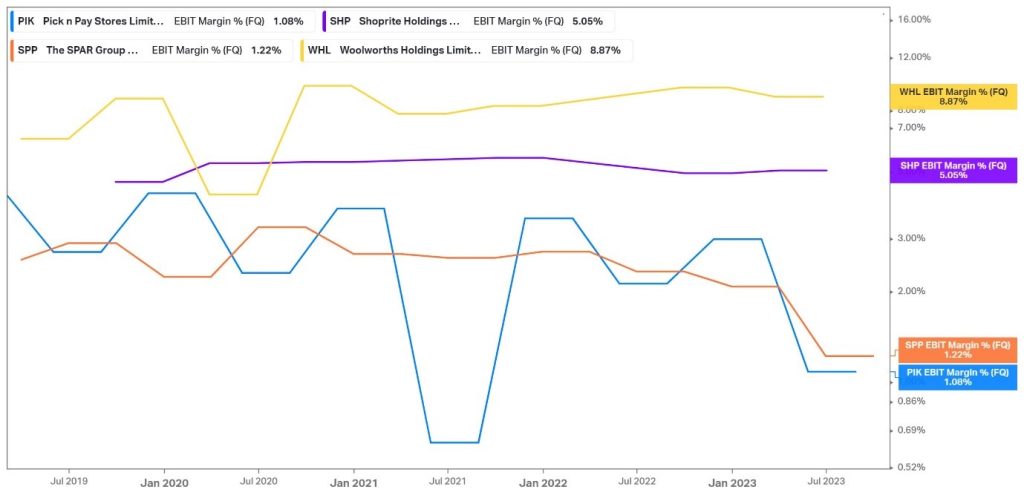

Pick n Pay faced a notable downturn in its EBIT margin, sliding from 2.98% to 1.08% within a quarter, signalling a concerning shift in profitability. The sharp decline stemmed from a significant 14% surge in operating costs, exerting immense pressure on their earnings. Interestingly, only Spar group experienced a similar setback, whereas Woolworths and Shoprite managed to navigate this challenging terrain relatively unscathed.

Source: Trive – Koyfin, Nkosilathi Dube

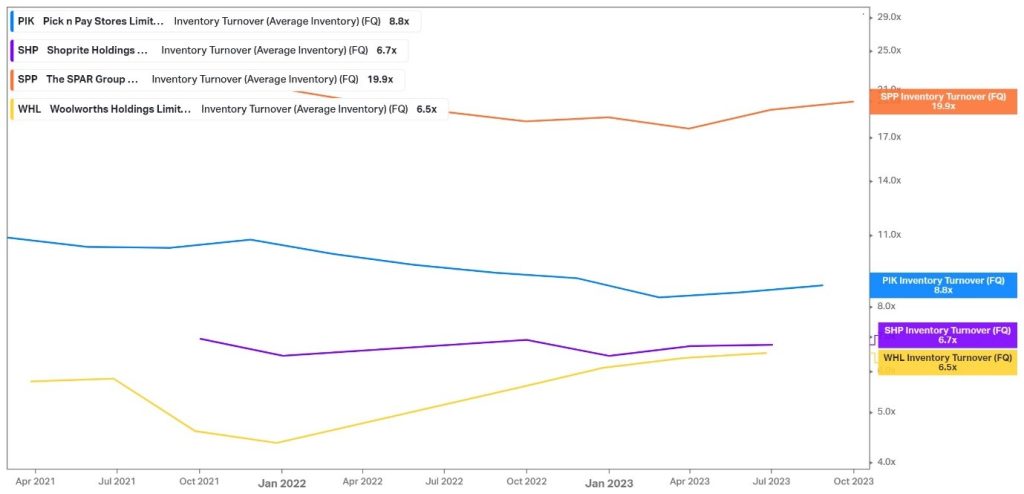

Pick n Pay’s inventory turnover of 8.8x signifies a different approach to managing its inventory compared to its peers. While it trails Spar’s notably high turnover of 19.9x, it surpasses Shoprite and Woolworths. This metric measures how efficiently a company is managing its inventory—the higher the turnover, the quicker goods are sold and replaced. Pick n Pay’s ratio indicates a moderate pace, striking a balance between inventory control and ensuring product availability. Spar’s exceptionally high turnover could reflect rapid sales or leaner inventory management strategies. The company’s approach to inventory turnover reflects its unique operational and market dynamics in the competitive retail landscape.

Source: Trive – Koyfin, Nkosilathi Dube

Pick n Pay’s Price-to-earnings (P/E) ratio, standing at 73.70x, portrays a comparatively higher valuation relative to its earnings compared to peers. This elevated ratio signifies that investors are willing to pay a premium for Pick n Pay’s earnings compared to Spar, Shoprite, and Woolworths. Such a high P/E ratio might indicate heightened investor expectations for future growth and profitability.

Summary

Within the competitive retail sector, Pick n Pay stands as a notable contender facing a distinct set of challenges. Despite a staggering share plunge and profitability concerns, its resilience in maintaining buoyant turnover reflects its robust market positioning. However, with a notably higher Price-to-earnings ratio compared to peers, investors could exhibit confidence in Pick n Pay’s future growth potential, potentially indicating optimistic projections.

Sources: Reuters, Statistics South Africa, Deloitte, KPMG, BusinessDay, TradingView, Koyfin

Piece Written By Nkosilathi Dube, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd (hereinafter referred to as “Trive SA”), with registration number 2005/011130/07, is an authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act, 37 of 2002. Trive SA is authorised and regulated by the South African Financial Sector Conduct Authority (FSCA) and holds FSP number 27231. Trive Financial Services Ltd (hereinafter referred to as “Trive MU”) holds an Investment Dealer (Full-Service Dealer, excluding Underwriting) Licence with licence number GB21026295 pursuant to section 29 of the Securities Act 2005, Rule 4 of the Securities Rules 2007, and the Financial Services Rules 2008. Trive MU is authorized and regulated by the Mauritius Financial Services Commission (FSC) and holds Global Business Licence number GB21026295 under Section 72(6) of the Financial Services Act. Trive SA and Trive MU are collectively known and referred to as “Trive Africa”.

Market and economic conditions are subject to sudden change which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. Trive Africa and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered. Please consider the risks involved before you trade or invest. All trades on the Trive Africa platform are subject to the legal terms and conditions to which you agree to be bound. Brand Logos are owned by the respective companies and not by Trive Africa. The use of a company’s brand logo does not represent an endorsement of Trive Africa by the company, nor an endorsement of the company by Trive Africa, nor does it necessarily imply any contractual relationship. Images are for illustrative purposes only and past performance is not necessarily an indication of future performance. No services are offered to stateless persons, persons under the age of 18 years, persons and/or residents of sanctioned countries or any other jurisdiction where the distribution of leveraged instruments is prohibited, and citizens of any state or country where it may be against the law of that country to trade with a South African and/or Mauritius based company and/or where the services are not made available by Trive Africa to hold an account with us. In any case, above all, it is your responsibility to avoid contravening any legislation in the country from where you are at the time.

CFDs and other margin products are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how these products work and whether you can afford to take the high risk of losing your money. Professional clients can lose more than they deposit. See our full Risk Disclosure and Terms of Business for further details. Some or all of the services and products are not offered to citizens or residents of certain jurisdictions where international sanctions or local regulatory requirements restrict or prohibit them.