MTN Group Limited (JSE: MTN) is a South African telecommunications giant with a presence across 19 African markets. The company’s share price has depreciated over 21% year-to-date and over 27% in the past year, primarily due to the devaluation of the Nigerian naira, its biggest earner. Despite the recent decline, MTN maintains its medium-term outlook, targeting service revenue growth in the mid-teens (constant currency).

Technical Analysis

The daily chart shows that MTN is currently trading slightly higher around its 50-SMA (blue line) following its earnings release. However, the stock remains below the key 100-SMA (orange line) and 200-SMA (red line), indicating a short-term downtrend. The shorter-term 50-SMA and 100-SMA are also sloping downwards, further highlighting the bearish sentiment.

Short-term trading opportunities could arise toward the initial support at 7,753 cents should the 23.60% Fibonacci retracement-enforced 50-SMA provide significant resistance. A successful bridge of the initial support on significant volume could trigger a run, with the 6,787 cents price level acting as the next significant level lower.

However, with the RSI (58.09) firmly trading above the 50.00 level, a sustained break above the 50-SMA would leave the 38.20% Fibonacci retracement level (10,254 cents) as the initial resistance. A break above the initial resistance on significant volume would leave the 50.00% Fibonacci retracement level (11,026) and 61.80% Fibonacci retracement level (11,789), a discount of 11.37% and 4.18% from the company’s discounted cash flow estimated fair value of 12,282 cents (yellow line), within the bulls’ reach in the near term.

Fundamentals Analysis

MTN’s recent financial results were significantly impacted by the devaluation of the Nigerian naira. The company reported a 72.3% decline in full-year profits as its Nigerian unit suffered a loss. Despite these headwinds, MTN’s service revenue grew by 6.9% year-on-year to ZAR 210.1 billion, driven by a 9% increase in active data subscribers and a 5% rise in active Mobile Money (MoMo) users.

Table: Quarter on Quarter Subscribers (‘000)

Source: Excel, Mfanafuthi Mhlongo

Source: Excel, Mfanafuthi Mhlongo

Despite the headwinds impacting profitability, MTN experienced steady subscriber growth across its African markets. This is a positive indicator of the company’s long-term potential. Year-on-year, MTN added over 9 million subscribers, reaching a total of 295 million. Notably, the number of active data users surged by more than 9%, reflecting the continent’s growing demand for internet connectivity.

Additionally, MTN’s mobile money platform, MoMo, witnessed a remarkable 32.2% increase in transaction volumes, highlighting the increasing adoption of financial technology solutions in Africa. This subscriber base expansion across core services positions MTN to capitalize on the rising digital demands across its footprint.

Source: Trive Financial – Koyfin, Mfanafuthi Mhlongo

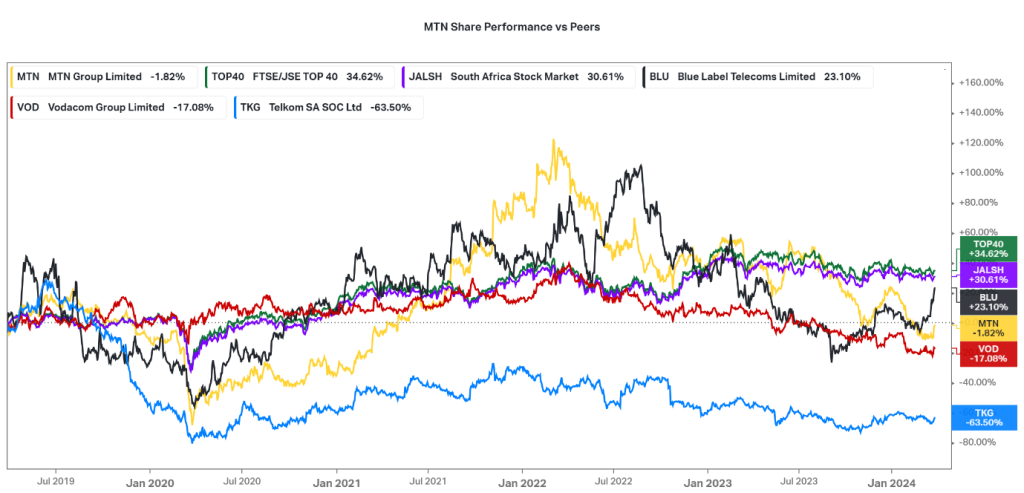

MTN’s share performance paints a concerning picture compared to its peers and major indices over the past three years. While the broader JSE Top 40 and All-Share Indices enjoyed significant growth (over 30%), MTN’s share price has declined by over 1.8%. Even amongst its direct competitors, MTN emerges as a laggard. Vodacom’s share price dipped, but the decline was less severe (down over 17%). Telkom’s share price suffered the most significant drop (down over 63%) within the comparison group. Interestingly, the beverage company Blu Label, with partial exposure to Africa’s mobile network operators, defied the trend and witnessed a share price increase of over 23% during the same period. This suggests that investors’ sentiment towards the broader African telecoms sector might be cautious.

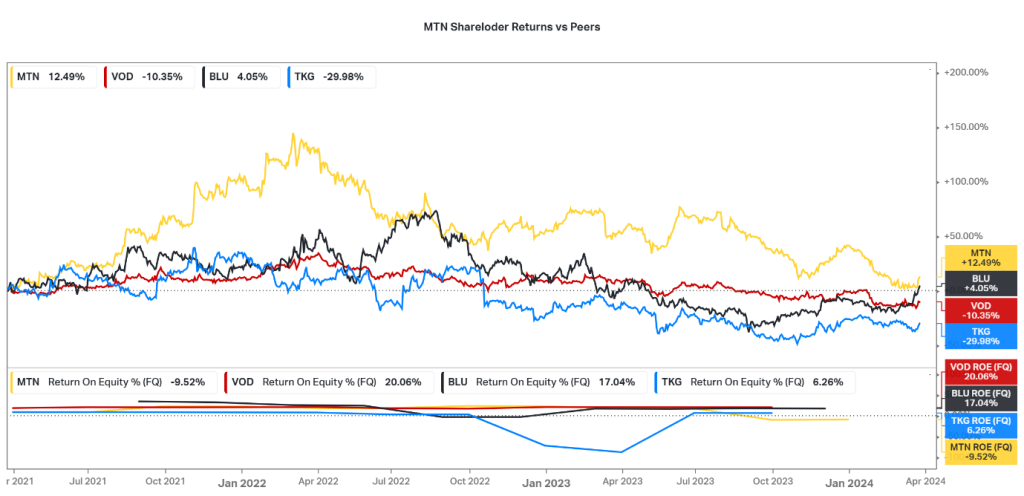

On a positive note, MTN outperformed its peers in terms of total shareholder return, with a return of 12.49% over the past three years. Vodacom offered negative returns (-10.35%), and Telkom’s total return was even worse (-29.98%). However, MTN’s negative ROE during this timeframe raises concerns about the company’s ability to generate shareholder value. While MTN boasts superior profitability margins compared to Vodacom and Telkom, translating those margins into shareholder returns remains a challenge.

Source: Trive Financial – Koyfin, Mfanafuthi Mhlongo

Analyzing MTN’s past financial performance against its peers reveals a mixed picture. On the one hand, MTN demonstrates clear strengths in profitability metrics. Compared to competitors like Vodacom and Telkom, MTN boasts a superior gross profit margin (64.58%) and EBIT margin (25.39%) for the previous financial year. This indicates MTN’s efficiency in converting revenue into profit. However, MTN’s negative return on equity (ROE) over the past three years stands in stark contrast. This metric suggests that despite healthy profit margins, MTN struggles to translate those profits into returns for shareholders. This could be due to factors like a high debt burden or a large reinvestment of profits back into the business for expansion.

Further dissecting the performance, Vodacom emerges with a positive ROE (20.06%) but with slightly lower profitability margins compared to MTN. Telkom, on the other hand, trails behind in both aspects, exhibiting negative ROE and lower margins. While MTN’s profitability is commendable, addressing the negative ROE is crucial to enhancing shareholder value in the long run.

Source: Trive Financial – Koyfin, Mfanafuthi Mhlongo

When it comes to shareholder return performance, MTN presents a conflicting story compared to its major competitors. While MTN boasts superior profitability margins, translating that strength into shareholder returns hasn’t been as successful. Over the past three years, MTN’s share price has declined by over 1.8%, significantly lagging behind the broader JSE Top 40 and All-Share Indices, which witnessed substantial growth (over 30%). Even amongst direct competitors, MTN falls behind. Vodacom experienced a share price decline as well but to a lesser extent (down over 17%). Interestingly, beverage company Blu Label, with indirect exposure to African mobile operators, saw a share price increase of over 23% during the same period. This suggests a potential lack of investor confidence in MTN’s ability to convert profits into shareholder value despite its strong margins.

On a brighter note, MTN outperformed its direct telecoms competitors in terms of total shareholder return. Over the past three years, MTN delivered a return of 12.49%, while Vodacom offered negative returns (-10.35%), and Telkom’s total return was even worse (-29.98%). However, this positive statistic is overshadowed by MTN’s negative ROE during this timeframe. This metric indicates that despite generating profits, MTN struggles to translate them into meaningful returns for shareholders. Until MTN addresses this issue, its total shareholder return might not be enough to compete effectively with its peers in the long run.

Encouragingly, MTN declared a final dividend of 330 cents per share, maintaining its payout ratio despite the profit decline. The company is also seeking new minority investments in its fast-growing fintech business, which witnessed a 32.2% surge in transaction volumes. MTN recently partnered with Mastercard to further accelerate fintech growth.

Summary

MTN’s share price is currently under pressure due to the Nigerian naira devaluation. However, the company’s resilient service revenue growth, expanding fintech business, and commitment to shareholder returns offer promising long-term prospects. Technically, a break above the 50-day SMA could trigger a bullish rally towards the Fibonacci retracement levels.

Sources: TradingView, MTN, Business Live, MoneyWeb, KoyFin, BusinessTech.

Piece written by Mfanafuthi Mhlongo, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd (hereinafter referred to as “Trive SA”), with registration number 2005/011130/07, is an authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act, 37 of 2002. Trive SA is authorised and regulated by the South African Financial Sector Conduct Authority (FSCA) and holds FSP number 27231. Trive Financial Services Ltd (hereinafter referred to as “Trive MU”) holds an Investment Dealer (Full-Service Dealer, excluding Underwriting) Licence with licence number GB21026295 pursuant to section 29 of the Securities Act 2005, Rule 4 of the Securities Rules 2007, and the Financial Services Rules 2008. Trive MU is authorized and regulated by the Mauritius Financial Services Commission (FSC) and holds Global Business Licence number GB21026295 under Section 72(6) of the Financial Services Act. Trive SA and Trive MU are collectively known and referred to as “Trive Africa”.

Market and economic conditions are subject to sudden change which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. Trive Africa and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered. Please consider the risks involved before you trade or invest. All trades on the Trive Africa platform are subject to the legal terms and conditions to which you agree to be bound. Brand Logos are owned by the respective companies and not by Trive Africa. The use of a company’s brand logo does not represent an endorsement of Trive Africa by the company, nor an endorsement of the company by Trive Africa, nor does it necessarily imply any contractual relationship. Images are for illustrative purposes only and past performance is not necessarily an indication of future performance. No services are offered to stateless persons, persons under the age of 18 years, persons and/or residents of sanctioned countries or any other jurisdiction where the distribution of leveraged instruments is prohibited, and citizens of any state or country where it may be against the law of that country to trade with a South African and/or Mauritius based company and/or where the services are not made available by Trive Africa to hold an account with us. In any case, above all, it is your responsibility to avoid contravening any legislation in the country from where you are at the time.

CFDs and other margin products are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how these products work and whether you can afford to take the high risk of losing your money. Professional clients can lose more than they deposit. See our full Risk Disclosure and Terms of Business for further details. Some or all of the services and products are not offered to citizens or residents of certain jurisdictions where international sanctions or local regulatory requirements restrict or prohibit them.