Transaction Capital Limited (JSE: TCP) recently experienced a volatile market journey marked by significant fluctuations. In its latest financial report, the company disclosed a headline loss per share (HEPS) of 99 cents from continuing operations, showcasing a 144% reduction compared to the 224.4 cent profit reported in the previous fiscal year. The challenges were notably driven by the ongoing restructuring of its SA Tax business, aimed at securing the company’s stability.

Despite these hurdles, a glimmer of optimism surrounds Transaction Capital Limited. The potential for a separate listing of its WeBuyCars business, distinct from the challenges faced by the SA Taxi business, became a catalyst for a remarkable surge in the company’s stock price. This surge, exceeding 9% on Tuesday, marked the highest closing price observed in the past seven months. The market’s response underscores the intriguing possibilities ahead for Transaction Capital Limited as it navigates through its current uncertainty.

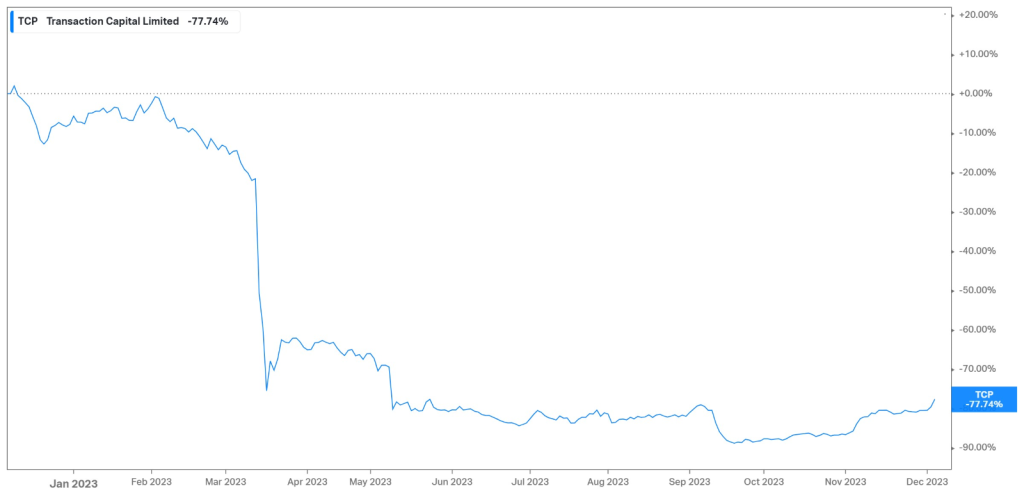

As seen in the chart below, the company’s share price has contracted close to 80% over the last year. It is no secret that the company is struggling with a massive debt burden, with the catalyst of the selloff being a trading statement earlier in the year, which alerted investors to the struggles of its taxi business. This business was hit hard by the Covid-19 pandemic, which placed ongoing restrictions on travel, floods in Kwazulu-Natal, ongoing fuel price increases, and the struggles posed by load shedding, as the lack of working robots have increased the average trip time, limiting the amounts of trips that taxis can complete during any given day. Further adding to the woes are higher interest rates, constraining the consumer’s ability to spend on travelling, while the business faces difficulty in passing the brunt of higher interest charges onto its customers.

Technical

On the 1D chart, an ascending channel has emerged, with the price initially pushing toward R8.18 before meeting resistance in a temporary retreat. The 25-SMA (green line) trades above the 50-SMA (blue line) and 100-SMA (orange line), confirming the presence of buyers in the short term. However, the RSI indicates overbought conditions, opening the door for a potential pullback in the upcoming sessions.

Support was found at R7.17 before the market retraced its initial correction. Should this trend continue and the selloff be completely wiped out, the market could retest the resistance at R8.18. While it poses a psychological level, a breakthrough could trigger an additional advance toward higher resistance at R8.80.

Conversely, if the market fails to initiate a breakthrough at R8.18, the ascending channel pattern may be sustained into the next few sessions. While support at R7.17 has previously prevented a channel breakdown, failure to do so on a second attempt could see the sellers enter to push the price toward R6.59, a support level backed by the 25-SMA. The Fibonacci midpoint and golden ratio are established not far below at R6.16 and R5.64, respectively, which could hold some buyers if the breakdown persists.

Fundamental

The company’s SA Taxi business made a headline loss from continuing operations of R3.7Bn, driven primarily by an additional R1.1Bn of repossessed vehicle write-downs in the second half of 2023. This business has started the process of aggressive restructuring, driven by a new management team, and is targeted for completion in the opening months of 2024. The restructuring is centered around cost reductions and repositioning within the pre-owned taxi market. The company has decided to move away from financing new minibus taxis to financing only pre-owned vehicles to create affordability in this segment. The business will strategically focus on these pre-owned taxis at lower volumes, and progress has been made in simplifying and downscaling the auto refurbishment and repair facilities, which has led to the decision of management to not sell this business after being classified as discontinued operations in the first half of the year.

The segment’s gross loans and advances were up 7% to R16.4Bn, while the number of loans originated were down 30%. The company now focuses on originating loans of higher credit quality since collection ratios have lagged pre-Covid levels. Net interest margin declined from 10.8% to 7.3% due to the inability to pass interest rate increases onto taxi operators.

In the latest earnings report, the company acknowledged that progress has been made in the restructuring of SA Taxi’s balance sheet. There is active engagement with debt funders to agree on a sustainable restructuring of the balance sheet by March of next year, which is crucial to the business’s survival. Currently, SANTACO owns 25% of SA Taxi through an industry SPV, and the business intends to restructure this holding with SANTACO’s funders and Transaction Capital, with Transaction Capital holding a R285M contractual commitment in this regard.

The WeBuyCars segment saw its earnings contract by 14% to R658M. This segment had to adapt to market conditions by reducing trade in high-end vehicles to focus more on lower priced vehicles, negatively impacting margins. The number of vehicles bought was up 9% to 142,337, while the number of vehicles sold advanced by 13% to 141,851. Its Nutun business was the standout performer for the year, with its core earnings from continuing operations advancing by 10% to R479M.

Summary

It has been a volatile few sessions for Transaction Capital, mainly due to the dynamic changes in its SA Taxi business. With headwinds no doubt remaining in the upcoming six months, the share price could realize a pullback from its seven-month highs. Resistance at R8.18 could be the level to watch in the upcoming sessions to determine whether the recent buying momentum could be sustained in the long term.

Sources: Koyfin, Tradingview, Reuters, BusinessLive, Moneyweb, Transaction Capital Limited

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.