Anheuser-Busch InBev (JSE: ANH), more commonly known as AB InBev, is the brewing behemoth behind around 500 beer brands celebrated worldwide. With a staggering array of beloved brews in its arsenal, this beer titan commands a staggering 25% slice of the global beer consumption pie, asserting its dominance in the world of alcoholic beverages. Armed with this market muscle and buoyed by fervent consumer demand for its iconic brands, the company has brewed up success through innovative digital transformations and revenue-boosting strategies. These efforts have proven resilient, even in the face of the recent frothy controversy surrounding Bud Light, allowing AB InBev to continue to tap into a lucrative future.

In its latest earnings report on the 3rd of August, the company slightly missed consensus on its top line after reporting revenue growth of 7.2% to $15.12Bn, with the market looking for $15.73Bn. On the bottom line, earnings per share (EPS) declined from $0.73 in the year-ago period to $0.72. However, due to its strong market positioning, the company benefitted from price increases, which resulted in a 9% expansion of revenue per hectolitre (hl). Total volumes were down 1.4%, mainly driven by a decline in US volumes due to the Bud Light controversy. Still, strong growth in its other geographic markets offset these declines, resulting in a 5% expansion in its EBITDA.

Technical

On the weekly chart, the share price has entered a consolidatory phase after a breakdown at the dynamic support of an ascending channel. The consolidation ranges between R1027.86 and R1090.10, with the daily pivot support at R1077.87 underpinning the upside potential.

If the consolidation continues, there could be a bounce off the R1090.10 resistance in the upcoming session, where the share price could retest the 38.2% Fibonacci retracement at R1061.29. The 50-SMA provides additional support at this level, but a breakdown could catalyse a shift out of the consolidation rectangle toward R1013.70, the Fibonacci midpoint. The golden ratio could then provide support at R966.10 if the downside pressure persists.

The 25-SMA (green line) is currently trading above the 50-SMA (blue line), suggesting the existence of bullish medium-term momentum. However, a break above the consolidation resistance could be tricky on declining volumes, considering the 25-SMA resistance is just a short distance above. However, if the R1090.10 level gets breached, there could be a retest of the 23.6% Fibonacci retracement at R1120.18 from the late April peak. The estimated fair value at R1181.29 is not far out of reach from this level, presenting a 9.3% potential upside from the current price.

Fundamental

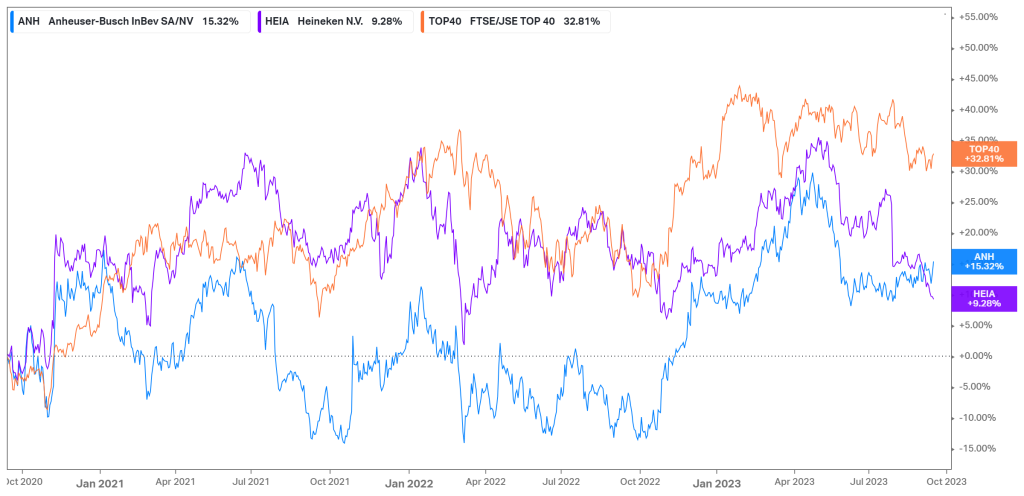

Over the last three years, AB InBev has returned a modest 15.32% in price appreciation. However, during the COVID-19 lockdown in 2020 and 2021, the company suffered a significant slump due to the ban on alcohol that was implemented over several geographies. The company’s sales took a considerable hit, trickling through to its share price. However, due to its geographical diversification, it was able to weather the storm and start its path to recovery. Despite some medium-term headwinds, such as the Bud Light scandal, the company has outperformed its main competitor, Heineken (9.28%) over the same time horizon. However, both companies lag behind the JSE Top 40 index, which has returned 32.81% over the same period, without the single stock risk.

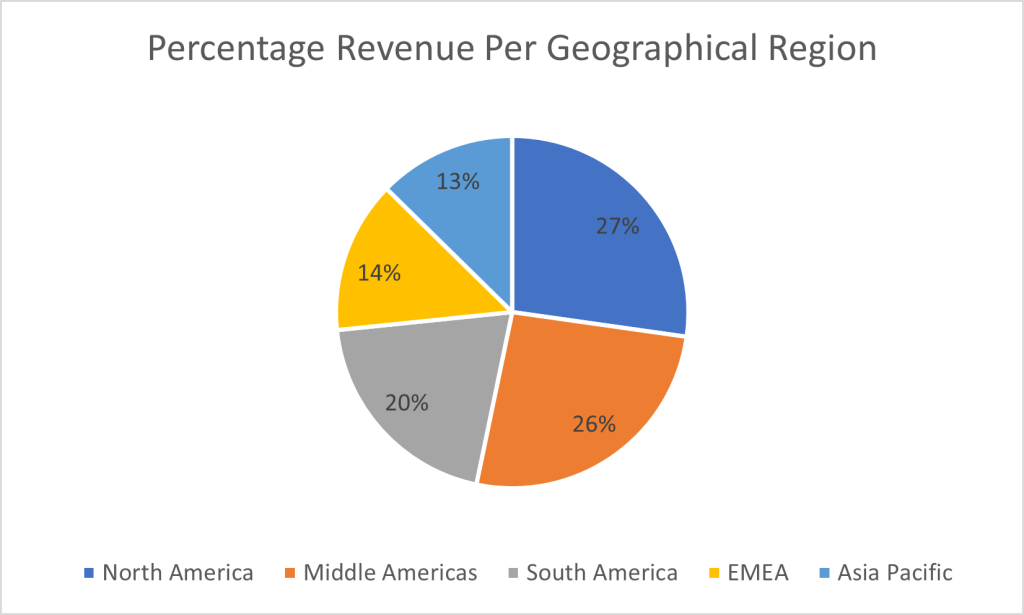

AB InBev has steadily grown its revenue over the last few quarters, benefitting from pricing actions and premiumisation of its well-known brands. In the latest quarter, its North America segment, including the United States and Canada, experienced a 14.1% volume reduction, causing a 9% drop in revenue. The volume reduction in Bud Light heavily impacted the performance in this segment. However, its net revenue/hl was up 5.9%, suggesting strong performance if volume returns to normalisation. While this affected the company’s top and bottom lines, the graph below shows the geographical diversification in its revenue stream, with solid performance in its other geographies offsetting the US decline. In the Middle Americas, including Mexico and Colombia, volumes were stable, with net revenue increasing 10.2%, with a 9.9% expansion in net revenue/hl. In South America, through Brazil and Argentina, volumes declined slightly, but due to price increases, net revenue/hl was up 26.2%, resulting in a 23.8% expansion in net revenue. Similarly, its EMEA segment, which includes Europe and South Africa, expanded its top line by 12% with stable volumes. Strong volume growth in China further boosted the top line, as its net revenue increased by 14.5% on 9.5% higher volumes.

The company’s resilient top-line performance resulted from pricing actions, its premiumisation initiatives, and other revenue management strategies. Its global brands, including Corona, Stella Artois, and Budweiser, delivered 18.4% revenue growth outside their home markets, where the brands command a premium price. Corona’s revenue advanced 23.7% outside of Mexico, Stella Artois expanded 14.5% outside of Belgium, and Budweiser grew 16.9% outside of the US. Its digital transformation techniques have also been effective, as its business-to-business (B2B) digital platforms now account for 64% of the company’s revenue. One of its initiatives, BEES, has stood out with its lucrative growth. This B2B e-commerce platform allows store owners and retailers to place orders anytime, schedule deliveries, and gain points for purchases that could eventually be traded in for merchandise. This platform provides the benefits that consumers gain from online shopping to its retailers and has already gained 3.3 million customers, with a digital retention rate of over 98%. Additionally, the company is focusing on expanding its Beyond Beer portfolio, which is currently contributing $385M to its revenue.

AB InBev has also put a lot of focus on expanding its digital direct-to-consumer (DTC) business. This business made over $115M in revenue for the second quarter, including 16.5M online orders for the quarter, as they have reached 9.8M active consumers. Z Delivery is a rewards program that launched in April and gained 1.6M rewards members in its first 45 days, while its TaDa Delivery service has received approximately 2M orders in the second quarter of 2023, up 116% year on year. The growth in its B2B and DTC businesses through digital transformation highlights management’s commitment to innovatively grow its top line to maintain its positioning at the top of the industry.

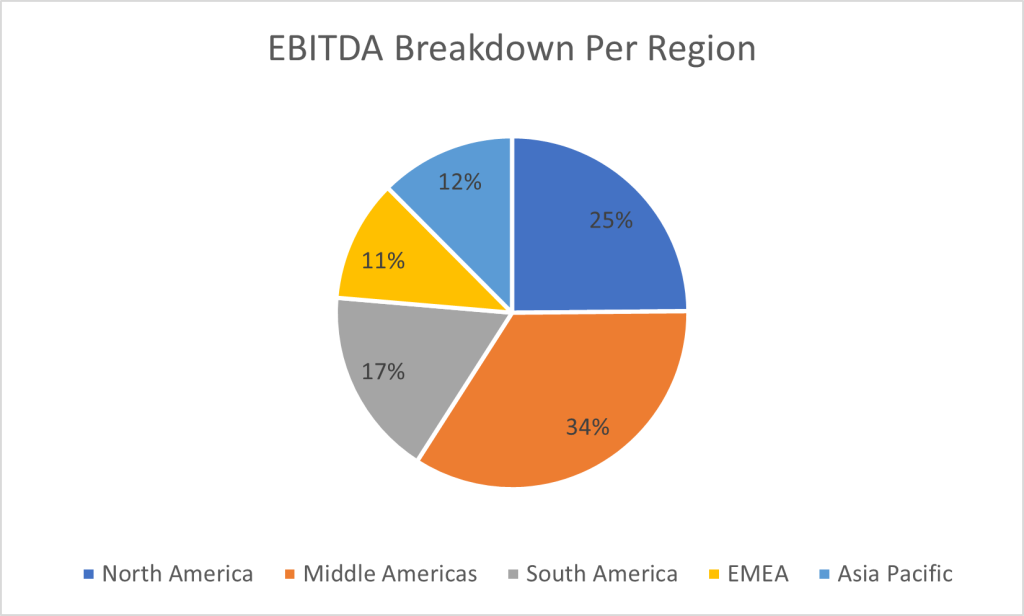

While North America contributes most of the company’s top line, the Middle Americas is the main profit generator in the company’s portfolio. Attributing 34% of its EBITDA, this geography expanded its organic EBITDA by 15.4% in the latest quarter. At the same time, its second-biggest profit generator, North America, suffered a 24.4% contraction in EBITDA, with its EBITDA margin falling to 30.1%, compared to 46.9% in the Middle Americas. South America and Asia Pacific expanded their organic EBITDA by 47.2% and 10.7%, respectively, further offsetting the profit reduction from the US.

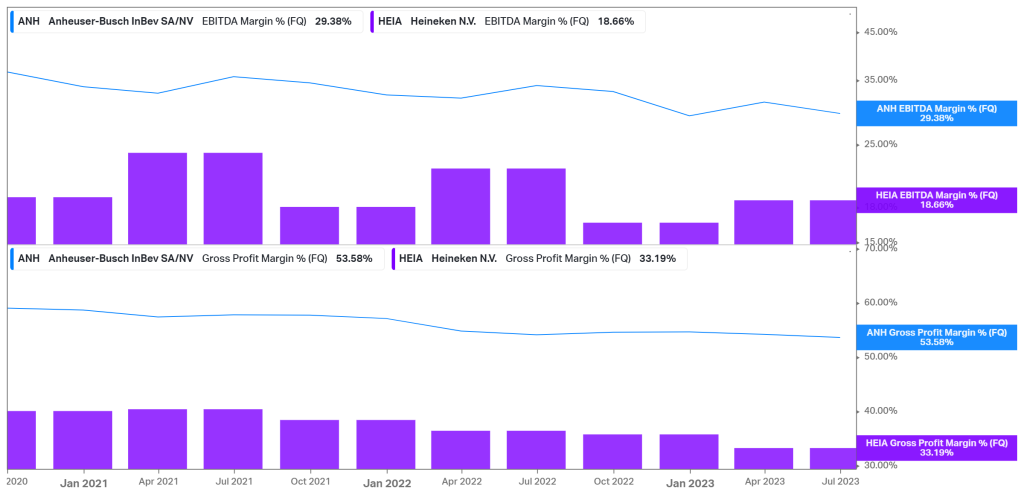

With healthy EBITDA expansion across most of its geographies, it is no surprise that the company’s margins are healthy. Despite the controversy around Bud Light, commodity cost headwinds, and an increase in sales and marketing expenses, the company’s EBITDA margin (29.38%) and its gross profit margin (53.58%) remain significantly higher than Heineken’s, which operates with an EBITDA margin of only 18.66% and a gross profit margin of only 33.19%. This results from AB InBev’s enormous scale, allowing it to run its breweries more efficiently at a lower cost, resulting in an economic moat, as its massive presence provides considerable barriers to entry to any potential competitors.

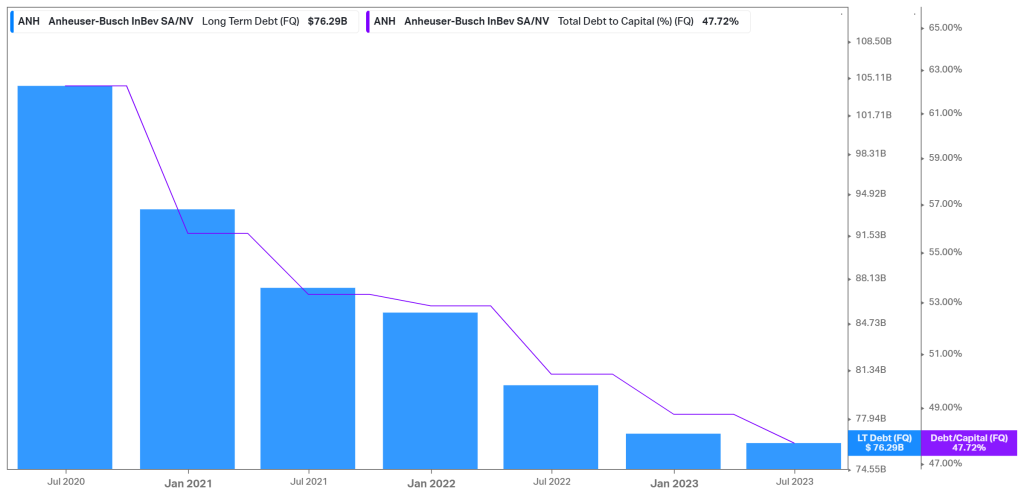

Another optimistic development in the company’s recent performance has been its continuous effort toward deleveraging. The graph below shows the sharp reduction in the debt levels over the last few quarters, with long-term debt falling from $104.35Bn in 2020 to $76.29Bn in the latest quarter. With only $3Bn in debt maturing through 2025, the company operates with minimal short-term refinancing needs, allowing it to continue investing in capital expenditures and marketing while maintaining its deleveraging process. As a result, the company’s capital structure has shifted, with its debt to capital falling from the low 60% range to only 47.72%, as it continues to take some risk off the balance sheet.

Summary

AB InBev holds a significant presence in the alcoholic beverage market. While it has recently faced some headwinds, management has shown commitment to innovate, which ultimately helped the company navigate some stormy seas. With solid performance over most of its diverse geographic segments, the company is accelerating its digital transformation while leveraging its pricing power over its large customer base. If the strength across its segments continues in upcoming quarters, the normalisation in its US operations could propel the revenue growth, potentially catalysing convergence with its estimated fair value at R1181.29 for a 9.3% potential upside from current levels.

Sources: Koyfin, Tradingview, Reuters, Anheuser-Busch InBev SA/NV.

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.