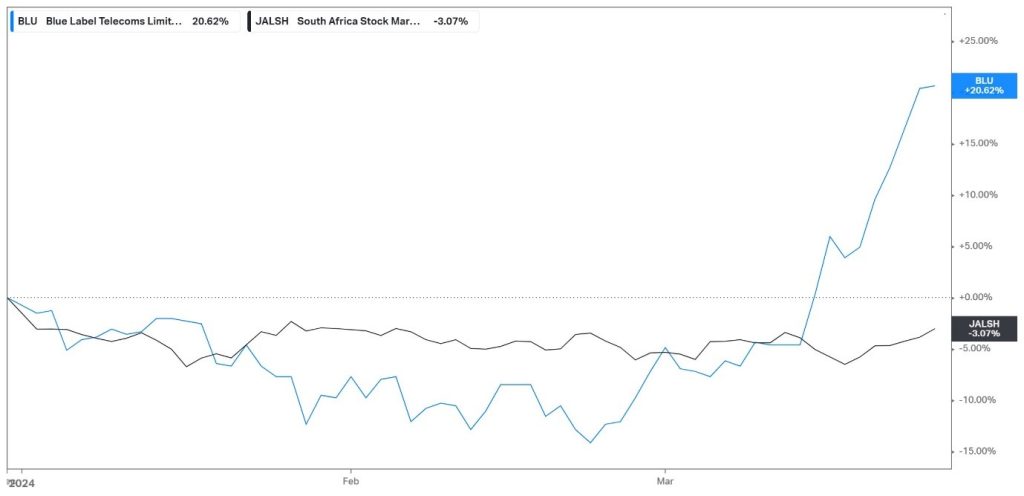

Blue Label Telecoms Ltd (JSE: BLU) has emerged as a beacon of resilience and growth in the dynamic landscape of South Africa’s stock market. With a remarkable 21% surge in share price year-to-date, Blue Label Telecoms is poised to break free from a two-year downturn, showcasing a robust performance that defies broader market trends. Blue Label Telecoms stands tall despite the South African Stock market experiencing a 3% decline, reflecting growing investor confidence in its fundamental strength and potentially promising earnings outlook.

Source: Trive – Koyfin, Nkosilathi Dube

At the heart of this positive sentiment lies the company’s latest interim results for the six months ending 30 November 2023. These results unveiled a compelling narrative of progress, with a notable uptick in all-inclusive revenue, gross profits, and margins. However, amidst these triumphs, Blue Label Telecoms confronts challenges typical of its operational terrain. Rising interest rates have strained consumer spending power, while power outages have hindered crucial revenue streams such as prepaid electricity and airtime sales.

Blue Label Telecoms commands a significant presence in South Africa’s telecommunications landscape, serving as the largest shareholder in Cell C (49.5%), the nation’s fourth-largest mobile network service provider. Moreover, its dominance extends to approximately 60% of the prepaid airtime market and about 50% of the prepaid electricity market. This success is underpinned by a business model centred on high-volume, low-margin distribution and sale of prepaid products and services, catering to a diverse clientele spanning socioeconomic spheres. As investors flock to capitalize on Blue Label Telecoms’ ascent, the company’s narrative indicates resilience, innovation, and market leadership, beckoning stakeholders to explore its compelling trajectory further.

Technical

Blue Label Telecoms has been riding a wave of success in the stock market, showcasing five consecutive days of gains and recently reaching a one-year high. This impressive rally is underpinned by robust technical indicators, with the share price trading above the 100-day moving average and following an ascending channel pattern.

Notably, the emergence of support at the R3.20 per share level, accompanied by a bullish hammer formation, signalled the market’s rejection of further downside, propelling the price upwards. Currently, Blue Label Telecoms is closing in on a significant resistance level at R5.20 per share, a point of interest dating back to the first quarter of 2023.

However, amidst this bullish momentum, caution is warranted as the Relative Strength Index (RSI) indicates overbought conditions. This suggests that while buyers are present, the market may be due for a correction. Therefore, investors should remain vigilant, particularly in anticipation of a potential downturn. Should a breakout above the ascending channel pattern occur on high volumes, it could signify intensified bullish momentum, with the R5.20 per share level becoming a focal point for further gains.

Fundamental

Blue Label Telecoms has showcased a commendable performance in the half-year period ending November 2023, marked by notable improvements across key financial metrics.

The company’s gross revenue experienced a healthy uptick, rising by 12% year-over-year to reach R43.8 billion, driven by robust performances in PINless top-ups, prepaid electricity, ticketing, and universal vouchers. This growth trajectory is further underscored by a 4% increase in gross profit, which climbed to R1.60 billion, attributed to enhanced margins. Notably, the gross profit margin expanded significantly from 15.67% to 21.08%, reflecting the company’s efficient cost management and revenue optimization strategies.

In terms of earnings, Blue Label Telecoms demonstrated remarkable progress, with core headline earnings for the period amounting to R420 million, translating to core headline earnings of 47.15 cents per share. This represents a substantial improvement from the comparative period, where core headline earnings stood at R35 million, equivalent to 3.94 cents per share. However, it’s important to note that the previous period’s earnings were impacted by negative contributions stemming primarily from the recapitalization transaction of Cell C.

Despite these challenges, Blue Label Telecoms’ brand resilience remained intact, evidenced by an increased customer base and a notable boost in Average Revenue Per User (ARPU). The company reported a total of 8.5 million customers, marking an increase of 300,000, while the blended ARPU surged by 11% to R89. This robust performance underscores Blue Label Telecoms’ ability to effectively capitalize on market opportunities and navigate through adversities, positioning itself as a formidable player in the telecommunications landscape.

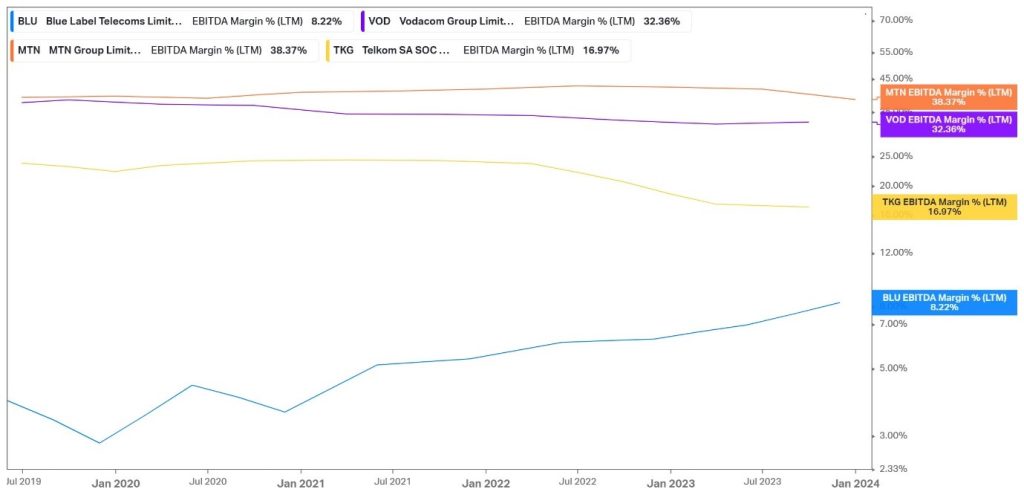

Source: Trive – Koyfin, Nkosilathi Dube

Blue Label Telecoms’ EBITDA margin of 8.22% falls notably below the industry average of 23.98%, positioning it at the lower end among competitors. This discrepancy can be attributed to several factors: Firstly, its smaller presence in the telecoms sector compared to industry giants like Vodacom and MTN limits its economies of scale. Additionally, the costly recapitalization of Cell C, along with its high-volume, low-margin strategy, impacts profitability. While Blue Label Telecoms has exhibited steady growth, addressing these challenges through strategic cost management and market expansion initiatives will likely be crucial to enhancing profitability and competitiveness in the sector.

Source: Trive – Koyfin, Nkosilathi Dube

Blue Label Telecoms’ robust Return on Equity (ROE) of 17.23% significantly surpasses the industry average of 2.06%, underscoring its superior performance in generating profits relative to shareholders’ equity. This exceptional ROE reflects Blue Label Telecoms’ effective utilization of shareholders’ investments to generate earnings, outpacing its competitors in terms of profitability. Such a high ROE indicates the company’s ability to create value for shareholders and signifies efficient management of assets to generate returns.

Summary

Blue Label Telecoms demonstrates resilience and growth, showcased by a 21% surge in share price, despite challenges like EBITDA margin below the industry average at 8.22%. Its ascending channel pattern and support at R3.20 indicate potential for further gains, while addressing challenges can enhance profitability and maintain its competitive edge.

Sources: Blue Label Telecoms Ltd, MoneyWeb, IOL, My Broadband, TradingView

Piece Written By Nkosilathi Dube, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd (hereinafter referred to as “Trive SA”), with registration number 2005/011130/07, is an authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act, 37 of 2002. Trive SA is authorised and regulated by the South African Financial Sector Conduct Authority (FSCA) and holds FSP number 27231. Trive Financial Services Ltd (hereinafter referred to as “Trive MU”) holds an Investment Dealer (Full-Service Dealer, excluding Underwriting) Licence with licence number GB21026295 pursuant to section 29 of the Securities Act 2005, Rule 4 of the Securities Rules 2007, and the Financial Services Rules 2008. Trive MU is authorized and regulated by the Mauritius Financial Services Commission (FSC) and holds Global Business Licence number GB21026295 under Section 72(6) of the Financial Services Act. Trive SA and Trive MU are collectively known and referred to as “Trive Africa”.

Market and economic conditions are subject to sudden change which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. Trive Africa and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered. Please consider the risks involved before you trade or invest. All trades on the Trive Africa platform are subject to the legal terms and conditions to which you agree to be bound. Brand Logos are owned by the respective companies and not by Trive Africa. The use of a company’s brand logo does not represent an endorsement of Trive Africa by the company, nor an endorsement of the company by Trive Africa, nor does it necessarily imply any contractual relationship. Images are for illustrative purposes only and past performance is not necessarily an indication of future performance. No services are offered to stateless persons, persons under the age of 18 years, persons and/or residents of sanctioned countries or any other jurisdiction where the distribution of leveraged instruments is prohibited, and citizens of any state or country where it may be against the law of that country to trade with a South African and/or Mauritius based company and/or where the services are not made available by Trive Africa to hold an account with us. In any case, above all, it is your responsibility to avoid contravening any legislation in the country from where you are at the time.

CFDs and other margin products are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how these products work and whether you can afford to take the high risk of losing your money. Professional clients can lose more than they deposit. See our full Risk Disclosure and Terms of Business for further details. Some or all of the services and products are not offered to citizens or residents of certain jurisdictions where international sanctions or local regulatory requirements restrict or prohibit them.