The famous athleisure company has lost momentum after the latest earnings, which seems to have investors running Nike’s share price into the dirt.

Nike, Inc. (NYSE: NKE) reported their third-quarter earnings for the 2023 financial year after the bell on Tuesday, with a rare double-beat of estimates signalling a solid financial quarter for the footwear giant. However, the company continues to face inventory problems, with its margins suffering, enticing investors to run the share price to a 4,68% daily contraction on Wednesday.

Although the company has beaten revenue estimates across all their geographical segments while growing its top line, investors expressed concern over its ability to expand its margins. Inventory markdowns and foreign currency headwinds resulted in a 330bps contraction in their gross margin in the latest quarter. Management expects this metric to be down by 250bps for the 2023 fiscal year, toward the higher end of their previous projection. This headwind overshadowed the positive revenue guidance that got revised up from mid-single-digit growth to high single-digit gain as investors turned bearish.

Technicals

The price action on Nike has seen short-term bullish momentum come to an end and started to consolidate at the start of the year, with more macroeconomic headwinds on the cards for the bulls. Last Wednesday, the 5% leg down on the share price found support around the $118.00 (black dotted) share level, which will be watched closely for another leg lower. If support fails, then we could possibly see the $112.90 (red line) support as a focal point for the bears.

The estimated fair value of the stock is $139,96 (green line) on a discounted cash flow basis. Therefore, when the market provides support, the bulls could be in for attractive upsides, as the price currently trades at a 17% discount to the estimated fair value. If lower support at $112,90 gets tested, a 25% potential upside could be realised when the share price converges to fair value.

Fundamental

For the third quarter of 2023, the company generated $12,39Bn in revenue to beat the $11,48Bn consensus. This revenue reflects a growth rate of 14% from the same quarter last year. Earnings per share contracted to $0,79 from $0,87 the year before, although it still beat the $0,55 estimate. Revenue for the NIKE brand came in at $11,8Bn, while Converse generated revenue of $612M, reflecting growth of 14% and 8%, respectively.

Nike has shifted their business model away from wholesale toward a direct-to-consumer-based model. The expansion of their direct sales is evident, with NIKE Direct Sales up 17% in the latest quarter, with their wholesale segment also realising revenue growth of 12%. NIKE Brand Digital Sales also expanded by 20% to round up solid top-line performance. From a geographical standpoint, North America, EMEA and Asia Pacific stood out, with revenue growth of 27%,17% and 10% more than offsetting the 8% fall in Chinese sales. It is clear that the top line is robust, but investor concerns were around margins.

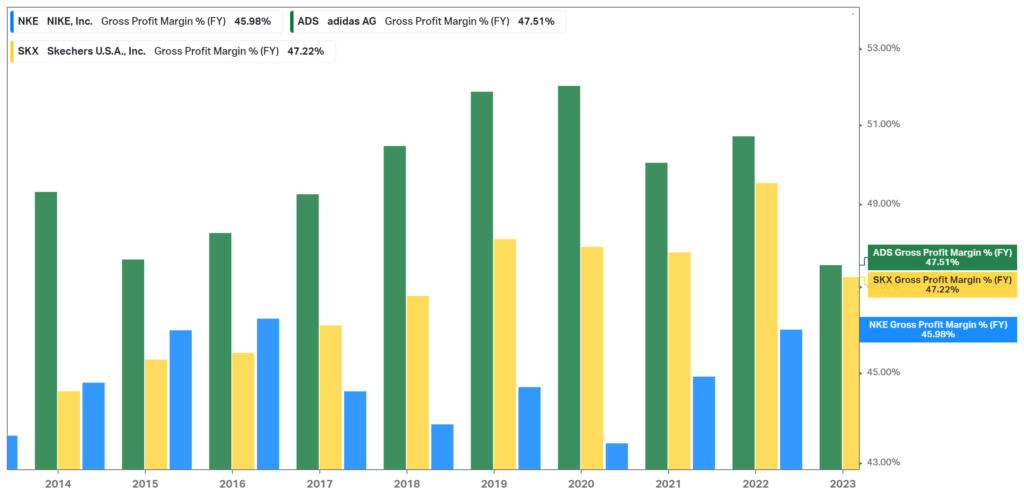

In the graph below, Nike’s gross profit margin is compared to its competitors, highlighting the low margins at which the company operates. Due to an overload of inventories, the company’s bottom line has suffered due to discounting as it attempted to get its inventory numbers down. In the latest quarter, inventories grew by 16% year on year. Management saw this as a massive improvement from the 43% growth in the previous quarter, but it could remain a headwind. The company reflected this headwind in their downward revised guidance for their gross margin, which is now expected to contract by 250bps in the 2023 fiscal year.

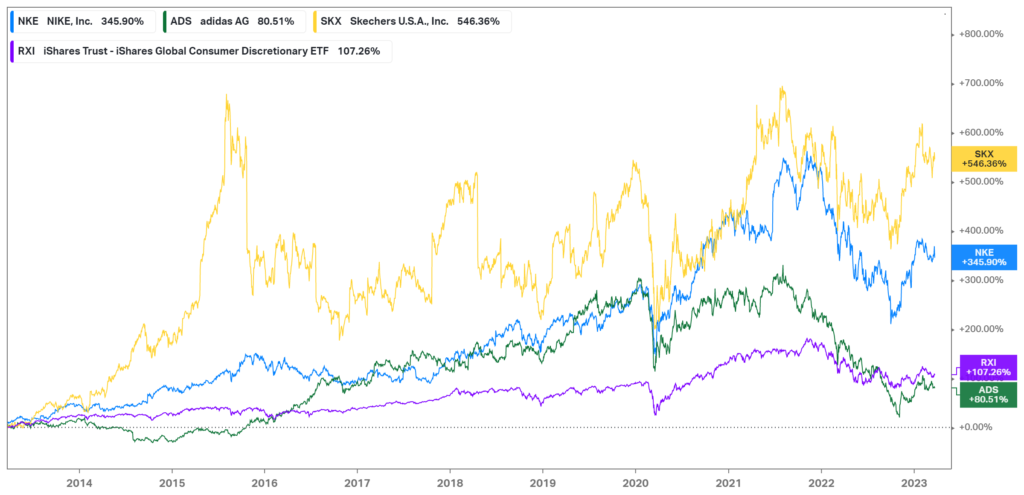

Despite these concerns, there is room for optimism in their share price performance over the last ten years. Although they underperformed relative to Skechers, robust outperformance compared to Adidas and a consumer discretionary ETF is a positive sign for investors, as conditions have not necessarily suited the industry in recent years. Their resilient performance could be a result of their strong balance sheet.

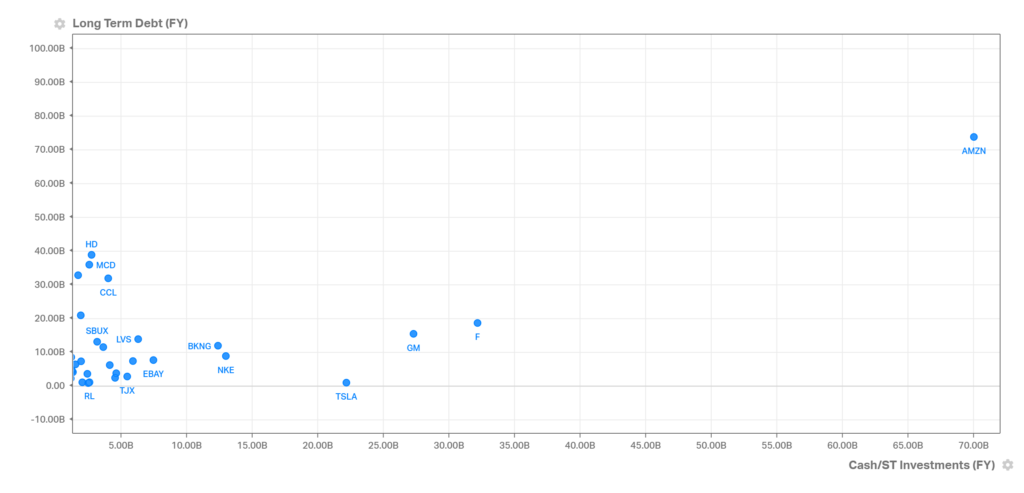

Their balance sheet strength is shown below compared to major competitors in the discretionary industry. The company lies toward the lower end of the debt spectrum while having a solid stockpile of cash and short-term investments. These factors could affect the company’s ability to navigate the recessionary waters the broader economy might soon face.

It is no secret that the company faces macroeconomic headwinds in the near-term future as discretionary demand remains under pressure. However, the company also faces tailwinds that could aid the share price in unlocking its potential value. These include the Chinese economic reopening, which could further boost their top line. One of its main competitors, Adidas, is also losing popularity in its famous Yeezy brand, which could hand Nike some market share. Their innovation and digital transformation could also boost future growth as the economy inevitably recovers and turns to growth.

Summary

While the company is growing its top-line performance across the board, robust inventories continue to pressure its margin and, as a result, its share price. However, even with the discretionary industry not looking attractive in the current macroeconomic conditions, it could open up opportunities for long-term investors. The eventual ease of demand pressures could relieve the margin stress and aid its top-line growth, catalysing a convergence to the $139,96 estimated fair value.

Sources: Koyfin, Tradingview, Yahoo Finance, Nike, Inc., Reuters, CNBC

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.