Shoprite Holdings LTD (JSE: SHP) has displayed a strategic masterclass in recent years, finding the sweet spot between innovation and affordability. However, the retail battleground is ablaze with fierce competition, where every move is a strategic step in the quest for market domination. As the company moves to capture share in alternative markets, macroeconomic challenges persist, potentially hindering its ability to continuously capture share against other higher-margin businesses.

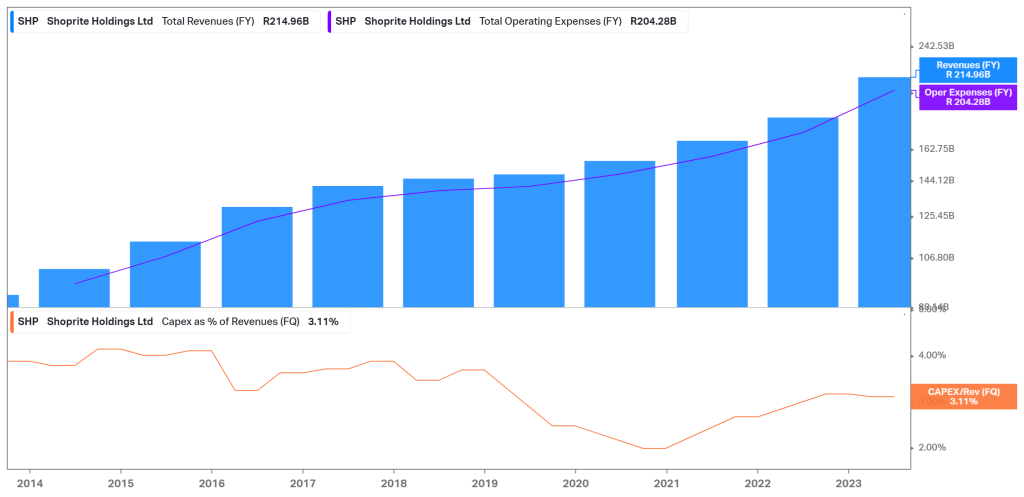

In its latest financial report for the 52 weeks ended July 2023, the company reported a 16.9% revenue expansion to R215.0Bn, with a 10.6% like-for-like increase. Gross profit advanced 14.8% to R51.7Bn, bringing the gross profit to 24.1%. Adjusted headline earnings per share increased 3.8% to 1,161.2 cents, rounding off a solid year. However, the market has high expectations for South Africa’s largest supermarket group, causing the share price to slump 5.64% on the earnings date, as management guided cautiously for the opening six weeks of the 2024 year, as selling price inflation is falling from its peak.

Technical

On the 1D chart, the earnings report initiated a breakdown at the dynamic support of an ascending channel, with the share price pushing through the 50-SMA (blue line) before finding support at R238.67, the 38.2% Fibonacci retracement from the peak of the uptrend.

Since then, the share price has retraced toward the breakdown point of the channel, retesting resistance at the 25-SMA (green line) in an attempt to advance above the R259.42 resistance. With the recent formation of a golden cross, the medium-term momentum supports the buying pressure, which could induce an additional leg up to R266.37 before converging with the estimated fair value of R283.44, presenting an 11.07% potential upside from current levels.

However, if the 25-SMA resistance proves too strong, a breakdown of the R248.98 could confirm a new downtrend toward R238.67 and R229.50. Lower support at R224.23 could then prevent convergence with the Fibonacci golden ratio at R221.30, where the potential upside widens to 28% from the estimated fair value.

Fundamental

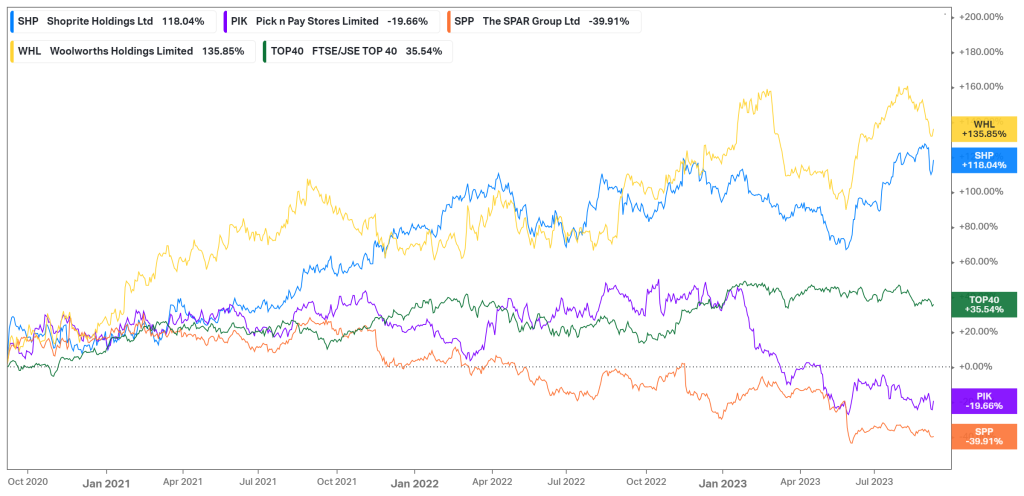

Over the last three years, Shoprite has returned 118.04% to its shareholders, outperforming Pick n Pay (-19.66%) and Spar (-39.91%), which have rapidly lost market share. Shoprite has taken the retail market by storm, targeting lower LSM consumers while attempting to move into the higher-income markets to compete with Woolworths. Its innovative ways to capture consumers, such as the Xtra Savings Programme and its Checkers Sixty60 offerings, have set it apart in terms of technological innovation, allowing growth in excess of the market, as the FTSE/JSE Top 40 returned 35.54% over the same period.

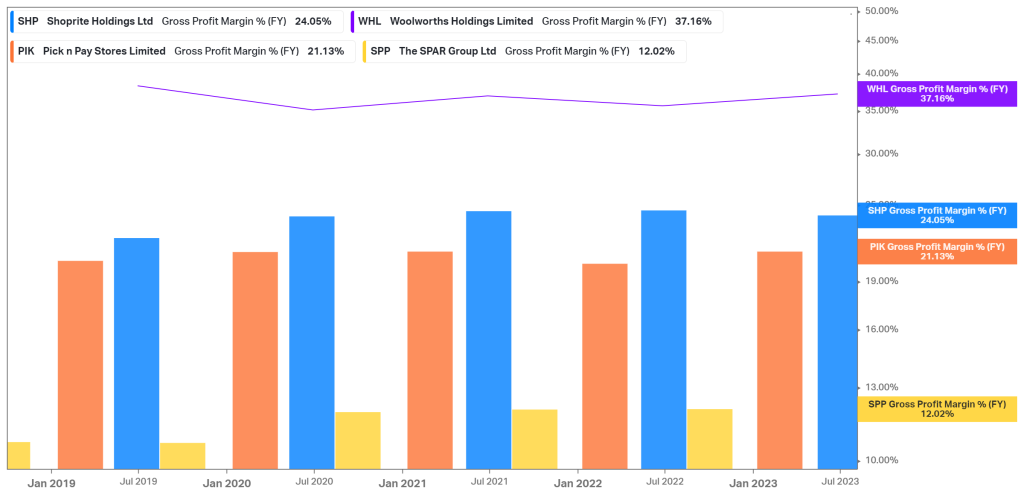

However, due to its value and affordability focus, the company can not pass rising costs onto the consumer across all of its brands in the same capacity as Woolworths. In the latest financial year, Shoprite reported internal inflation of its South African supermarkets at 10.1% for the year, compared to the country’s 12.3% official food inflation. As a result, the company’s 24.1% gross profit margin falls below the 37.16% of Woolworths due to the nature of their respective markets. However, compared to other lower-income-focused retailers such as Spar and Pick n Pay, Shoprite operates with higher margins due to its impressive economies of scale and lower production costs due to the well-developed supply chain infrastructure the company has invested in.

In the latest financial year, the company’s 16.5% revenue expansion resulted from efficiency across the board, with all its brands performing well. The Checkers and Checkers Hyper brands realized R69.3Bn in revenue, up 18% from the year-ago period, with this segment holding 14.8% of the share in the South African market. With 10.6M Xtra Savings members, Checkers boasts the number-one retail rewards program in the country, showing South African consumers’ loyalty to its affordable quality products. On the lower LSM side, the Usave and Shoprite brands added another R90Bn to the company’s top line, up 15.6%. Its Xtra Savings members amount to 17.2M, adding to the massive base of its Checkers Xtra Savings members. In total, the Supermarkets RSA segment grew by 17.8%, with Checkers on top of the list of the fastest-growing grocers in the premium food segment. Customer visits in the year were up 13.2%, with the basket size growing by 3.9%. Volumes were also up 4.9%, painting a positive demand picture for the company’s products.

However, with the revenue growth, operating expenditures have also grown, mainly due to the R1.3Bn spent on diesel required to operate generators in the South African stores due to the high levels of load-shedding. As a result, its bottom line has faced some challenges, but the company has some industry-leading opportunities that could drive its bottom line to sustainable growth. This is shown below with the elevated levels of capital expenditures in recent quarters. The company’s expenditure on innovations such as Sixty60 has been highly effective. Currently, this service is dominating the delivery market, and are on track to launch a R99 per month subscription model, which will be a first for grocery retailers, in order to grab additional share in this market. The Sixty60 sales grew 81.5% in the latest financial year, adding to the rapid growth rates over the last few years. Additionally, the company is expanding its store base and is planning to add 200,00 square meters in new distribution centres over the next two years, with 314 additional stores in the pipeline for the new financial year, which started on the 3rd of July.

Summary

Shoprite has been outperforming its peers over recent years, eating away at the market share in the industry with its innovative offerings and customer focus, intending to provide its consumers with affordable value. While macroeconomic headwinds are pressuring its growth and spending, the company has an estimated fair value of R283.44, presenting an 11.07% potential upside from current levels.

Sources: Koyfin, Tradingview, Yahoo Finance, Shoprite Holdings Ltd.

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.