The commodity market faced a challenging start to the new year, particularly with metal prices enduring a prolonged downturn. This trend has impacted Glencore plc (JSE: GLN), resulting in a notable year-to-date decline of nearly 12%, coupled with a 6% dip just last week.

Amid this decline, the metal and mining giant experienced a rating downgrade from Deutsche Bank. Concerns regarding production, stemming from asset sales, mine closures, and operational challenges, prompted the downgrade. Despite these challenges, anticipation is building for February, as Glencore is poised to unveil its latest production report on the 1st and its full-year earnings report later in the month. The upcoming releases have the potential to influence a shift in the market’s perception of the stock’s future prospects.

Technical

On the daily chart, a breakdown occurred at the dynamic support of an ascending channel, pushing the price through the 25-SMA (green line), 50-SMA (blue line) and 100-SMA (orange line) in confirmation of the bearish tilt. However, the RSI signals potential oversold conditions, which could trigger a temporary retracement in the upcoming days.

The price currently trades near a demand zone at R97.18, where it looks to find support. Resistance at R99.92 stands in the way of a retracement, and any clearance of this level could signal a bounce back toward R102.39. The Fibonacci midpoint and 61.8% golden ratio at R105.16 and R107.01 could then be of importance, as additional legs higher could push the price back above the multiple-SMAs in a sign that the bulls are regaining the upper hand.

However, if the resistance at R99.92 prevents this, the price could hover around the demand zone at R97.18. Neckline support is established at R95.38 if the demand zone falters and could prevent another prolonged downturn in the upcoming days.

Fundamental

Over the last three years, Glencore’s share price has appreciated by over 72%, tracking the iShares Global Energy ETF with a relatively strong correlation. This performance is substantial when compared to other industry players such as Anglo American plc (-22.10%), Rio Tinto (-10.74%), and BHP (-2.49%), which has suffered more due to its less diversified exposure to specific metals, such as Palladium and Platinum, that have suffered even more in the current cyclical downturn. So, can Glencore continue outperforming its peers in the current macroeconomic environment?

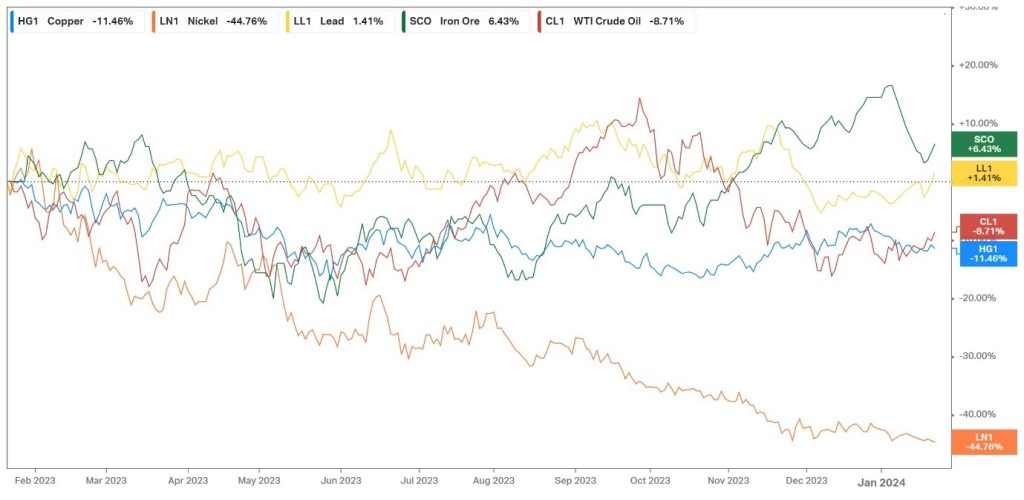

In its half-year report for 2023, Glencore reported a 20% reduction in its year-to-date revenue from $134.44Bn in 2022 to $107.42Bn. Its earnings per share (EPS) fell by 61% to $0.36, as its net income attributable to equity holders contracted by 62% from R12.01Bn to R4.57Bn. As previously mentioned, one of the main drivers behind this decline has been the price weakness in the metal market. In its half-year report, Glencore acknowledged the headwinds, citing significant weakness in the energy market, with the overall cycle of inflation, tighter monetary conditions and a slowdown in economic growth contributing to the declines. Copper, Cobalt, Nickel and Zinc experienced average period-over-period reductions of 11%, 59%, 13%, and 26%, respectively. The chart below shows the year-to-date performance of these metals, with the likes of Nickel and Copper futures declining by 45% and 12%, respectively, suggesting that the market has not eased off the pressure ahead of its next financial report slated for February.

Along with the weakness in metal prices, the company’s production prospects present another concern. In its latest quarterly production report, the company reported a 5% reduction in copper production to 735,800 tonnes, reflecting the sale of Cobar in June, while its Zinc production fell by 4% to 672,100 tonnes, as a result of the disposal of its South American zinc operations and the closure of Matagami. Nickel production was down 16% at 68,400 tonnes, mainly due to strikes at its Raglan mine in 2022. These production declines align with Deutsche Bank’s concerning outlook for production due to asset sales and mine closures. Furthermore, the company altered its production guidance for 2023, with its Nickel production forecast coming in 9% lower at 98kt – 106kt from the prior 107kt – 117kt due to a longer-than-expected recovery period following the Raglan strike action in 2022. This will be an interesting metric to keep an eye on in the upcoming production update to gauge whether the declines are as severe as the company initially feared.

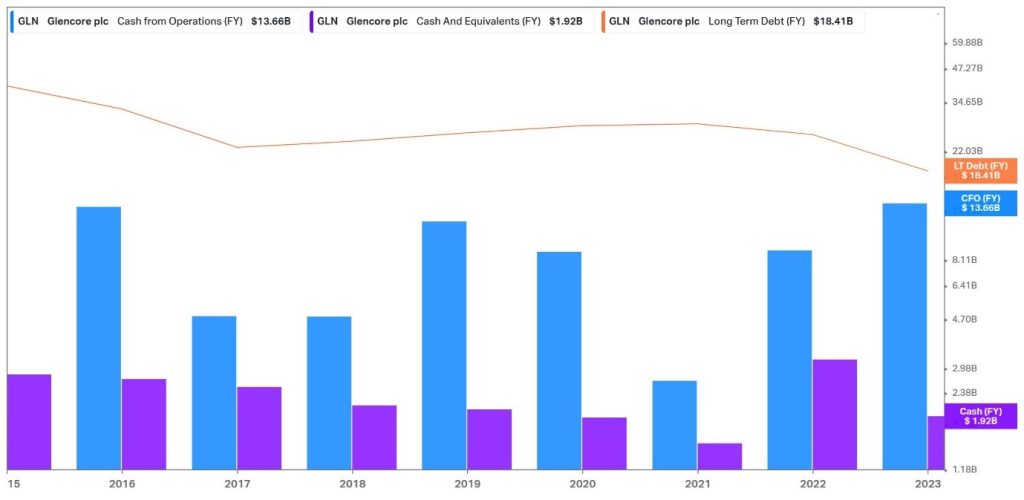

While the current environment is unfavourable for Glencore’s industry, the cyclical nature of the metal market is worth noting. Therefore, it is worth looking beyond what is currently happening and considering the company’s prospects in taking advantage of opportunities that present themselves when the market eventually bottoms out. The graph below indicates the balance sheet health of the company. The company’s cash from operations has gradually increased over the last few years, with its long-term debt position showing an opposite trajectory. With its cash from operations and cash and equivalents almost entirely covering its debt position, the company’s ability to acquire funding to take advantage of growth opportunities in the future remains strong and could act as a tailwind in the upcoming years once the metal market normalises.

Summary

Glencore has been under severe pressure in the opening weeks of 2024, with its share price contracting close to 12% in the opening three weeks. However, a crucial month lies ahead, as its latest quarterly production report and its full-year earnings could give investors further insight into the operational environment the company currently finds itself in. Investors could look toward any updates on its production guidance and additional developments in metal prices to gauge whether the recent contraction is close to finding a bottom.

Sources: Koyfin, Tradingview, Reuters, Glencore plc

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd (hereinafter referred to as “Trive SA”), with registration number 2005/011130/07, is an authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act, 37 of 2002. Trive SA is authorised and regulated by the South African Financial Sector Conduct Authority (FSCA) and holds FSP number 27231. Trive Financial Services Ltd (hereinafter referred to as “Trive MU”) holds an Investment Dealer (Full-Service Dealer, excluding Underwriting) Licence with licence number GB21026295 pursuant to section 29 of the Securities Act 2005, Rule 4 of the Securities Rules 2007, and the Financial Services Rules 2008. Trive MU is authorized and regulated by the Mauritius Financial Services Commission (FSC) and holds Global Business Licence number GB21026295 under Section 72(6) of the Financial Services Act. Trive SA and Trive MU are collectively known and referred to as “Trive Africa”.

Market and economic conditions are subject to sudden change which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. Trive Africa and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered. Please consider the risks involved before you trade or invest. All trades on the Trive Africa platform are subject to the legal terms and conditions to which you agree to be bound. Brand Logos are owned by the respective companies and not by Trive Africa. The use of a company’s brand logo does not represent an endorsement of Trive Africa by the company, nor an endorsement of the company by Trive Africa, nor does it necessarily imply any contractual relationship. Images are for illustrative purposes only and past performance is not necessarily an indication of future performance. No services are offered to stateless persons, persons under the age of 18 years, persons and/or residents of sanctioned countries or any other jurisdiction where the distribution of leveraged instruments is prohibited, and citizens of any state or country where it may be against the law of that country to trade with a South African and/or Mauritius based company and/or where the services are not made available by Trive Africa to hold an account with us. In any case, above all, it is your responsibility to avoid contravening any legislation in the country from where you are at the time.

CFDs and other margin products are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how these products work and whether you can afford to take the high risk of losing your money. Professional clients can lose more than they deposit. See our full Risk Disclosure and Terms of Business for further details. Some or all of the services and products are not offered to citizens or residents of certain jurisdictions where international sanctions or local regulatory requirements restrict or prohibit them.