The year has kicked off on an exhilarating note for the FAANG companies if one is to look at the share price performance. Google, Netflix, and Meta (Formerly called Facebook) have set the pace for this earnings season with their impressive results. Now, market participants have their eyes out for the last two companies of the set to release their results this Thursday.

Netflix, the streaming service, kicked off this earnings season and reported second-quarter financial results that came in mixed. Although revenue was 2.7% higher than the year-ago period, it missed estimates despite new initiatives like the crackdown on password sharing and the recently launched ad-supported tier. The operating margin hit 22.3% in the quarter, surpassing the company’s projection of 19%. Meta reported second-quarter results and revenue that exceeded analysts’ expectations, highlighting a recovery in the digital advertising market. The company’s revenue rose 11% over the prior year, marking the first time of double-digit growth since the end of 2021. Before the first quarter, the company’s revenue had decreased three times in a row as it dealt with the economy’s slowdown and Apple’s iOS privacy reform, which restricted ad targeting options. Google’s ad revenue only grew 3.3% from a year earlier after we had requested that they share their statistics; nonetheless, this is an improvement over the first quarter, when ad revenue decreased. Despite rivalry, Google’s YouTube and Cloud divisions both experienced revenue growth.

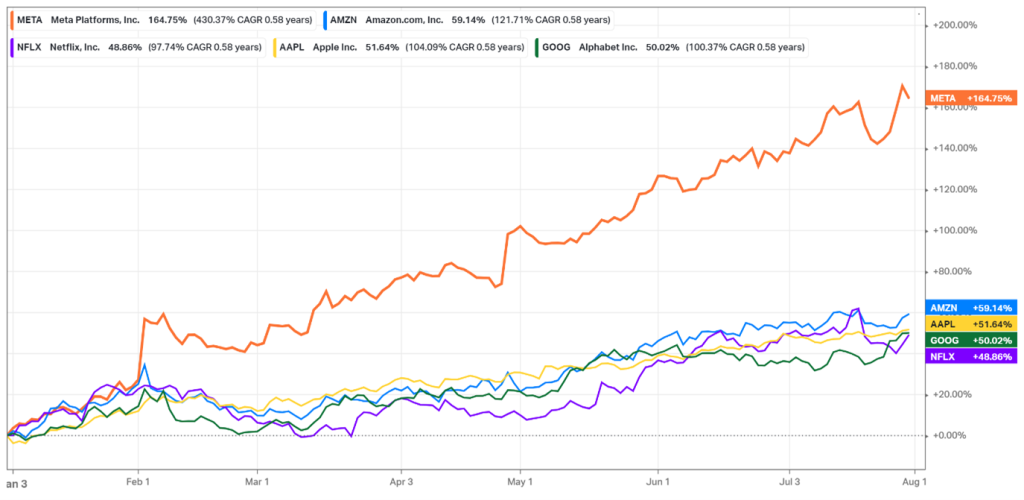

Figure 1: Year to Date performance of Meta, Apple, Amazon, Netflix, and Google

Above is how the companies have been performing since the beginning of the year, with Meat well ahead of the pack with a 164.75% increase in the share price. The other four had also had an excellent start to their year and are up by approximately 50%.

Technical analysis

Figure 2: Amazon’s daily candle stick chart from July 2021

The share price fell to a level last tested at the start of the Covid 19 pandemic in January of this year. But after that, the stock enjoyed a tremendous run, and in 2021, it reached an all-time high of $188.65. After reaching lows in January 2023, the share price, which had been on a downward trend from all-time highs, has begun to turn. The 200-day moving average and the 50-day moving average created a death cross shortly after the beginning of 2022 and broke free only in June 2023.

The share price is just below the resistance level at $136 a share, which has been tested several times. The price action failed to break through in mid-July of this year. The share price has just bounced off the 50-day moving average, and with the results on Thursday, we could see the share price continue to the upside and pass the resistance line at $136 a share.

Fundamentals for Apple and Amazon

Amazon

On revenue of $131.5 billion, analysts expect Amazon to earn $0.35 per share in the second quarter. Both of those numbers would be better than year-ago numbers, and they might be a welcome improvement over the first quarter’s mediocre performance, which showed flat e-commerce product sales in the face of macroeconomic pressures. The majority of the work to support the entire company’s growth was still done by the Amazon Web Services (AWS) division.

The e-commerce giant’s strategy for growth is working. Additionally, thanks to some recent operating expense cuts, Amazon now has a leaner cost profile, which will enable it to expand its earnings more quickly in the coming quarters. Reducing its global staff, closing unproductive operations, and reprioritizing resources to right-size the organization are some of the most recent cost-saving efforts. To continue getting stronger and leaner. Amazon Web Services has also been the company’s leading profit producer. Anchored by the AWS cloud platform, the company’s services segment is still enjoying exponential growth, offsetting recent weakness in the retail part.

Apple

The most recent average estimates predict that Apple will have earned $1.19 per share this quarter on revenue estimates of $81.6 billion. Both of those numbers would represent marginal drops from prior-year levels. It took record iPhone sales to keep earnings relatively unchanged compared to year-ago levels and to support overall revenue.

There are persistent indications that consumers are beginning to struggle, partly due to increasing interest rates, even though some inflationary pressures have subsided. The consumer economy has been robust due to continued good employment trends. The market undoubtedly believes that the company has room to grow. Market participants are also enthusiastic about the potential of the next iPhone 15, which will go on sale in September. However, it goes beyond iPhones alone. The long-awaited mixed reality headgear, Vision Pro, presented at the company’s Worldwide Developers Conference, will also interest the market.

Summary

Market players are now watching on Thursday to see what Amazon and Apple will announce in their results and whether they will fulfil expectations in light of the FAANG company’s significant comeback in 2023. Investors are more bullish about Amazon’s performance than Apple’s because they are less confident in the $3 trillion company’s ability to withstand macroeconomic challenges.

Positive or negative, the FAANG companies’ success has confirmed the resurgence of mega-cap Big-Tech dominance in the stock market.

Sources: CNBC; yahoo finance; The Motley Fool; Market watch; Nasdaq; Reuters Apple and Amazon

Author: Odwa Magwentshu, FMVA

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.