Shoprite Holdings Limited (JSE: SHP) celebrated a prosperous 2023, witnessing a commendable uptick of nearly 22% in its share price over the span of twelve months. The latest operational update for the initial quarter of its 2024 fiscal year accentuated its robust performance, with group sales experiencing an impressive surge of 13.2%. Within its largest segment, Supermarkets RSA, the company opened 43 new stores, staying firmly on course to unveil a total of 195 new stores throughout its 2024 fiscal year.

The remarkable performance extended beyond sales growth, as the segment’s market share expanded by 124 basis points. This achievement marked an impressive 55 months of consecutive market share gains, showcasing the company’s sustained momentum in the retail landscape. Adding to the allure of this food retail giant’s success is its ability to navigate and thrive despite macroeconomic headwinds that have forced many of its competitors into contractionary territory over the past year.

Technical

On the daily chart, an ascending channel was in play, where a breakdown occurred that drove the price through the 25-SMA (green line). However, the 50-SMA (blue line) provided support, initiating a retracement that could determine the directional trend of the price as we advance.

Resistance at R266.58 could be a level to watch in the upcoming sessions, as it could be a pivot point for the price to bounce off toward a new downtrend. For a sustainable bearish run to occur, the price may need to clear the 50-SMA support at R260,40, which could open a path toward the Fibonacci midpoint and 61.8% Fibonacci golden ratio at R254.36 and R248.69, respectively.

However, if the price clears resistance at R266.58, it could signal an unsustainable breakdown, making it possible for the price to regain momentum within the original channel pattern. Resistance at R271.23 and R278.22 could then be in the spotlight before the estimated fair value on a discounted cash flow basis of R281.86 could be reached.

Fundamental

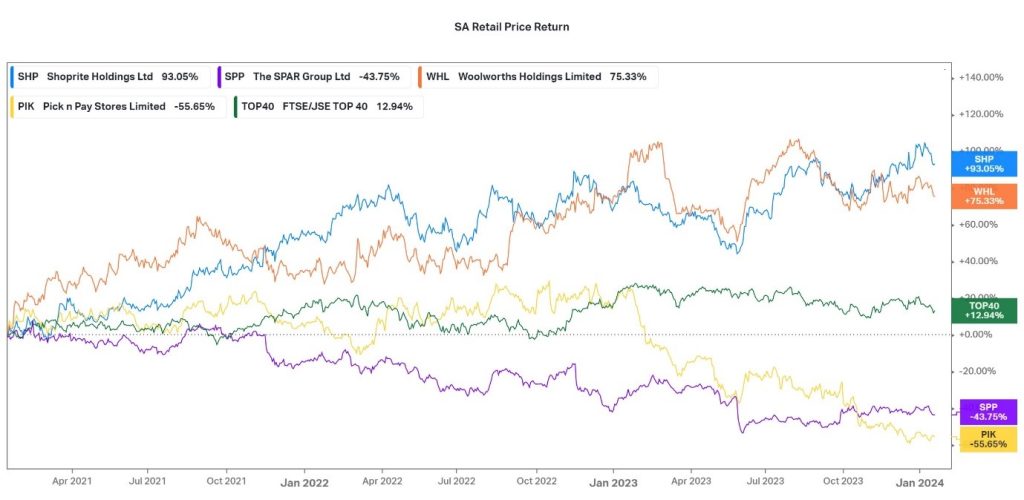

The chart below shows Shoprite’s dominance over the last three years, as it outperformed its main competitors and the JSE Top 40 Index with a 93% price appreciation. Evidently, Shoprite and Woolworths (75.33%) have been the frontrunners in the industry. The outperformance could be due to the business models employed by these companies, as Shoprite caters for a wide variety of LSM groups through their diversified offerings, a factor of crucial importance considering the tight spending environment caused by rising inflation and interest rates over the last few years, which caused consumers to trade down to cheaper value alternatives. On the other hand, Woolworths caters for higher-income shoppers, who are less sensitive to adverse macroeconomic conditions due to higher levels of disposable income. The strategic positioning of these companies has aided them in weathering the macroeconomic storms better than their industry peers, leading to outperformance in their share price.

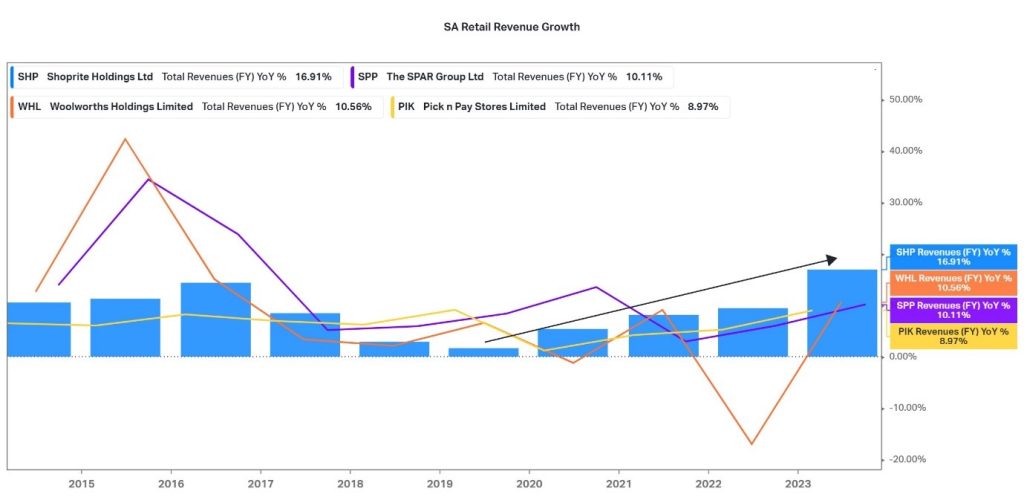

The chart below shows the revenue growth of major industry players in the food retail sector in South Africa over the last couple of years. A new trend has emerged with Shoprite, as it went from generating one of the lowest sales growth numbers within the industry to the highest, showing a clear uptrend in the pace at which it generates sales. In its latest financial year, its sales expanded by 16.9% to R215.0 billion (Bn), driven mainly by its Supermarkets RSA segment, which represents 81% of total sales, and expanded by 17.8% over the 52-week period. Customer visits in its stores expanded by 14.1%, while the average basket spend expanded by 3.3%. In its first quarter of 2024, the revenue in this segment expanded by 13.3%, contributing to the overall 13.2% group revenue expansion for the quarter. The revenue growth can be attributed to its attractive value offering at affordable prices, with its selling price inflation of 10.1% remaining lower than the official food inflation, which lures consumers to its stores in search of more affordable grocery offerings. As this trend continues, Shoprite remains well-positioned to continue expanding its top line, enabling it to grab additional market share in the years to come.

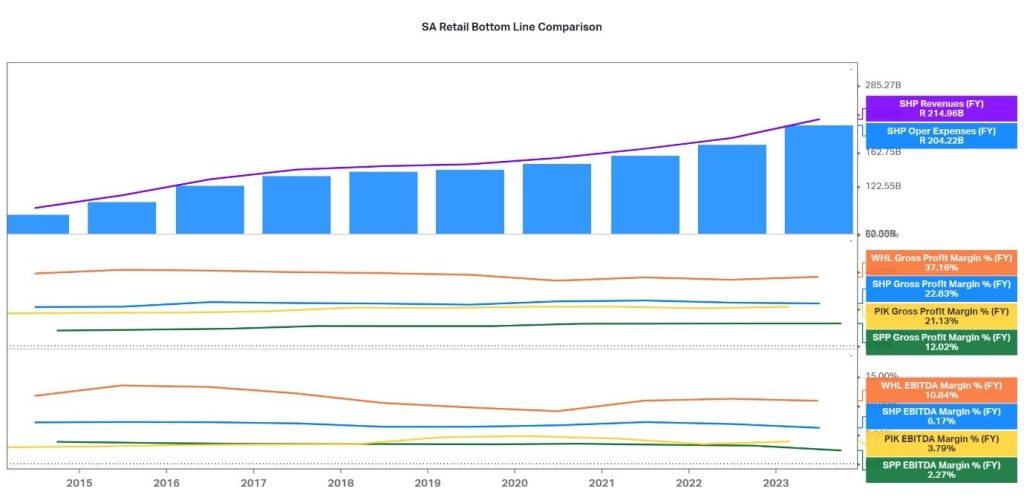

As much as its top line has shown promise, its operating expenses have increased at a similar rate. In 2023, the company bore a 36.7% increase in electricity and water costs, resulting from R1.3Bn spent on diesel to keep its generators running during periods of power outages due to the ongoing load shedding in its Supermarkets RSA segment. For the first quarter of 2024, the company spent an additional R281M in diesel, with these costs building up and eating into its bottom line. However, upon closer inspection of the graph below, Shoprite’s profitability remains optimistic regarding its positioning within the industry. As the largest and most profitable food retailer on the African continent, the company operates with a healthy gross profit margin of 22.83%, while its EBITDA margin sits at 6.17%. Compared to its industry peers, only Woolworths operates with higher margins due to the nature of its business. Shoprite’s diversified offering allows it to cater to the lower-income consumer while maintaining higher margins from its brands targeting higher-LSM groups, positioning it well in the industry to take advantage of changing consumer trends.

Summary

Shoprite may have started 2024 on the back foot regarding its share price movements, but the company remains well positioned within the industry going into the new year. Its diversified product offerings cater for a large portion of the South African population and enable it to weather macroeconomic headwinds more easily than many competitors. Its estimated fair value of R281.86 still presents a 7% potential upside from its current price and could soon be within reach if the breakdown of the recent ascending channel fails to be sustained.

Sources: Koyfin, Tradingview, Reuters, News24, Shoprite Holdings Limited

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd (hereinafter referred to as “Trive SA”), with registration number 2005/011130/07, is an authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act, 37 of 2002. Trive SA is authorised and regulated by the South African Financial Sector Conduct Authority (FSCA) and holds FSP number 27231. Trive Financial Services Ltd (hereinafter referred to as “Trive MU”) holds an Investment Dealer (Full-Service Dealer, excluding Underwriting) Licence with licence number GB21026295 pursuant to section 29 of the Securities Act 2005, Rule 4 of the Securities Rules 2007, and the Financial Services Rules 2008. Trive MU is authorized and regulated by the Mauritius Financial Services Commission (FSC) and holds Global Business Licence number GB21026295 under Section 72(6) of the Financial Services Act. Trive SA and Trive MU are collectively known and referred to as “Trive Africa”.

Market and economic conditions are subject to sudden change which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. Trive Africa and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered. Please consider the risks involved before you trade or invest. All trades on the Trive Africa platform are subject to the legal terms and conditions to which you agree to be bound. Brand Logos are owned by the respective companies and not by Trive Africa. The use of a company’s brand logo does not represent an endorsement of Trive Africa by the company, nor an endorsement of the company by Trive Africa, nor does it necessarily imply any contractual relationship. Images are for illustrative purposes only and past performance is not necessarily an indication of future performance. No services are offered to stateless persons, persons under the age of 18 years, persons and/or residents of sanctioned countries or any other jurisdiction where the distribution of leveraged instruments is prohibited, and citizens of any state or country where it may be against the law of that country to trade with a South African and/or Mauritius based company and/or where the services are not made available by Trive Africa to hold an account with us. In any case, above all, it is your responsibility to avoid contravening any legislation in the country from where you are at the time.

CFDs and other margin products are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how these products work and whether you can afford to take the high risk of losing your money. Professional clients can lose more than they deposit. See our full Risk Disclosure and Terms of Business for further details. Some or all of the services and products are not offered to citizens or residents of certain jurisdictions where international sanctions or local regulatory requirements restrict or prohibit them.