South Africa’s largest retail bank, Absa Group Limited (JSE: ABG), is under renewed selling pressure after declining over 5% following the disappointing full-year financial report. While the group managed to scrape by with a 1% rise in headline earnings for the year ended December 2023, surpassing the R100 billion revenue mark for the first time, a closer look reveals concerning cracks in the facade. A wave of bad debts, totalling R15.5 billion, surged through Absa’s books, particularly in its core South African market.

This unexpected rise, coupled with a sluggish economic environment riddled with high interest rates and inflation, sent shockwaves through the investor community, leading to a 5% plunge in Absa’s share price. But is this a cause for panic or a potential buying opportunity?

Technical Analysis

The Absa’s daily chart paints a picture of a stock in temporary retreat. The recent disappointing earnings report triggered a sell-off, pushing the share price below its key moving averages – the 50-SMA (blue line), 100-SMA (orange line), and even the long-term 200-SMA (red line).

With the sharply declining RSI (36.38) recently breaking below the 50.00 level, short-term trading opportunities could arise toward the initial support at 15,432 cents. A successful bridge of the initial support on significant volume could trigger a run, with the 15,012 cents and 14,561 cents acting as the next significant levels lower.

However, a recovery above the 50-SMA would leave the initial resistance at 16,583 cents firmly in play. A break above the initial resistance on significant volume would leave the 17,217 cents, a discount of 5.66% from the company’s discounted cash flow estimated fair value of 18,192 cents (yellow line), within the bulls’ reach in the near term.

Fundamental

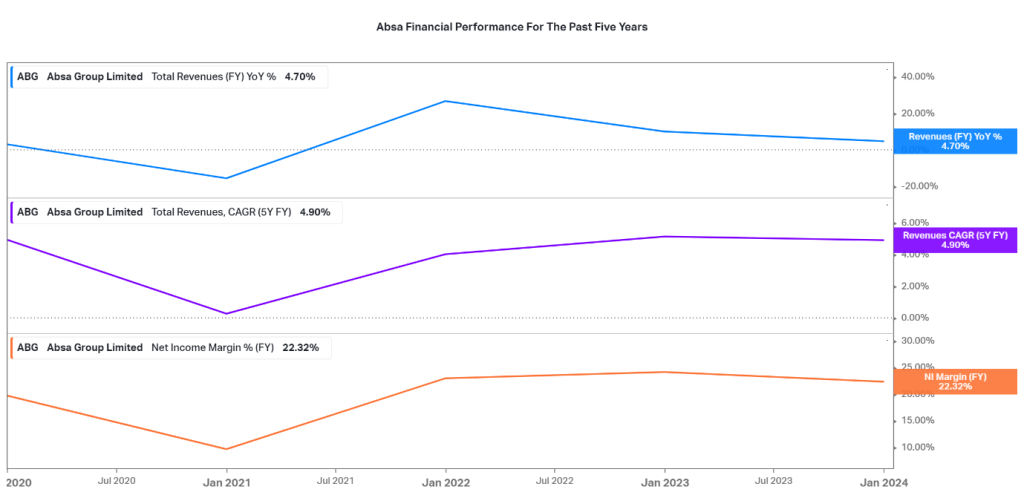

Absa Group’s fundamentals present a compelling case study in contrasting fortunes. On the surface, a steady 4.7% year-on-year revenue growth for FY2023, surpassing the R100 billion mark for the first time, paints a picture of stability. This is further bolstered by a strong five-year compound annual growth rate (CAGR) of nearly 4.9% in total revenue. Even profitability shows promise, with a net income margin for FY2023 exceeding 22%, a significant improvement compared to 2019.

Source: Trive Financial – Koyfin, Mfanafuthi Mhlongo

However, a closer inspection reveals cracks in the facade. The recent surge in bad debts, totalling R15.5 billion, primarily concentrated in the South African market, is a cause for concern and throws a wrench into Absa’s narrative of unblemished growth. This rise surpasses the average increase experienced by its major competitors – Capitec Bank, FirstRand Limited, Nedbank Group, and Standard Bank Group. While all these institutions witnessed a deterioration in their NPL ratios (picture below), Absa’s increase was steeper. This suggests that Absa might be facing challenges in effectively managing its loan portfolio in the current economic climate.

Adding fuel to the fire of caution is Absa’s high gross loans-to-total deposit ratio of 94.91% (picture below). This metric indicates that Absa relies heavily on borrowed funds to finance its lending activities. In a scenario of higher-for-longer interest rates, this dependence on external funding could continue to significantly impact Absa’s profitability. Interestingly, all of Absa’s major competitors have shown a decrease in this ratio over the past five years, suggesting a more conservative approach to lending.

Source: Trive Financial – Koyfin, Mfanafuthi Mhlongo

However, a silver lining emerges when we delve into Absa’s share price performance against major indices. Despite the recent dip triggered by the disappointing earnings report, Absa’s past three years performance remains positive, outperforming both the JSE Top 40 (orange dotted line) and the JSE All-Share Index (blue dotted line), who have appreciated 8.29% and 8%, respectively (picture below).

This outperformance becomes even more impressive when we consider the total return over the past three years. Absa significantly outshines the broader market, generating a return of over 40% compared to the single-digit returns of the JSE indices. This outperformance can be attributed, in part, to Absa’s strong presence in Africa’s fast-growing economies, offering a potential hedge against the sluggishness of the South African market.

Source: Trive Financial – Koyfin, Mfanafuthi Mhlongo

Absa’s annual report for the financial year ending December 2023 provides a deeper understanding of the company’s current state. While the headline earnings growth of 1% might seem underwhelming, a closer look reveals ongoing investments in digital transformation and strategic expansion into high-growth African markets. These efforts, while positive for long-term prospects, might be overshadowing short-term profitability due to upfront costs.

Absa’s fundamentals paint a picture with contrasting shades. While the group boasts impressive revenue growth and profitability, the recent surge in bad debts and a high loan-to-deposit ratio raise cautionary flags. However, its outperformance in the broader market and a strong foothold in Africa offer a glimmer of hope. The recently disclosed financials, coupled with Absa’s outperformance in the market, solidify its standing as a resilient and forward-thinking player in the financial sector. Investors and stakeholders are likely to find value in the bank’s strategic decisions and steady financial performance, positioning Absa for continued success in a dynamic market environment.

Summary

Absa Group presents a dilemma for investors; despite the current share sell-off, fundamentals suggest the potential for improved performance. Steady revenue growth and rising profitability are countered by a concerning rise in bad debt and a heavy reliance on borrowed funds.

The recent South African economic slowdown adds another layer of complexity. However, Absa’s strong foothold in Africa’s booming economies offers diversification. Their latest annual report hints at strategic investments impacting short-term gains but potentially fuelling future success.

Sources: TradingView, Absa, Business Live, MoneyWeb, KoyFin, BusinessTech.

Piece written by Mfanafuthi Mhlongo, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd (hereinafter referred to as “Trive SA”), with registration number 2005/011130/07, is an authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act, 37 of 2002. Trive SA is authorised and regulated by the South African Financial Sector Conduct Authority (FSCA) and holds FSP number 27231. Trive Financial Services Ltd (hereinafter referred to as “Trive MU”) holds an Investment Dealer (Full-Service Dealer, excluding Underwriting) Licence with licence number GB21026295 pursuant to section 29 of the Securities Act 2005, Rule 4 of the Securities Rules 2007, and the Financial Services Rules 2008. Trive MU is authorized and regulated by the Mauritius Financial Services Commission (FSC) and holds Global Business Licence number GB21026295 under Section 72(6) of the Financial Services Act. Trive SA and Trive MU are collectively known and referred to as “Trive Africa”.

Market and economic conditions are subject to sudden change which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. Trive Africa and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered. Please consider the risks involved before you trade or invest. All trades on the Trive Africa platform are subject to the legal terms and conditions to which you agree to be bound. Brand Logos are owned by the respective companies and not by Trive Africa. The use of a company’s brand logo does not represent an endorsement of Trive Africa by the company, nor an endorsement of the company by Trive Africa, nor does it necessarily imply any contractual relationship. Images are for illustrative purposes only and past performance is not necessarily an indication of future performance. No services are offered to stateless persons, persons under the age of 18 years, persons and/or residents of sanctioned countries or any other jurisdiction where the distribution of leveraged instruments is prohibited, and citizens of any state or country where it may be against the law of that country to trade with a South African and/or Mauritius based company and/or where the services are not made available by Trive Africa to hold an account with us. In any case, above all, it is your responsibility to avoid contravening any legislation in the country from where you are at the time.

CFDs and other margin products are complex instruments and come with a high risk of losing money rapidly due to leverage. You should consider whether you understand how these products work and whether you can afford to take the high risk of losing your money. Professional clients can lose more than they deposit. See our full Risk Disclosure and Terms of Business for further details. Some or all of the services and products are not offered to citizens or residents of certain jurisdictions where international sanctions or local regulatory requirements restrict or prohibit them.