The banking sector has been enjoying the cycle of high-interest rates, which has boosted its revenue. A pause in hikes is the consensus amongst analysts ahead of the Federal Reserves meeting on Wednesday as more hikes may strain consumers and lead to low growth in business and consumers defaulting in this high-interest rate environment.

Technical

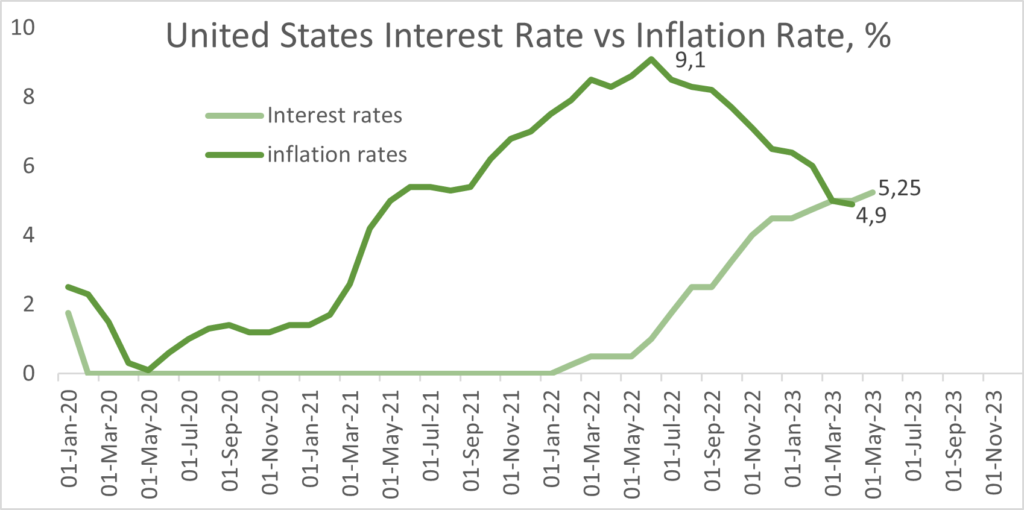

United States inflation data

Investors now have their attention set on the United States’ economic data releases due this week, with the CPI print on Tuesday, which is forecasted to fall to 4,1% in May from 4,9% in April. The inflation numbers will be a key matrix in whether the Federal Reserve will continue to raise rates with a majority of investors believing that the Federal Reserve will leave the interest rates unchanged at 5.25%. The Federal Reserve has stated that its main objective has been to curb inflation and has done a great job, despite a delayed start as they had believed that it was transitory at the time, in bringing the inflation rate down from highs of 9,1%. It is worth noting that the United States has an inflation target of 2%, which still leaves a long way to go.

Figure 1: Comparison between the United States interest rate and inflation rate

United States Dollar vs South African Rand

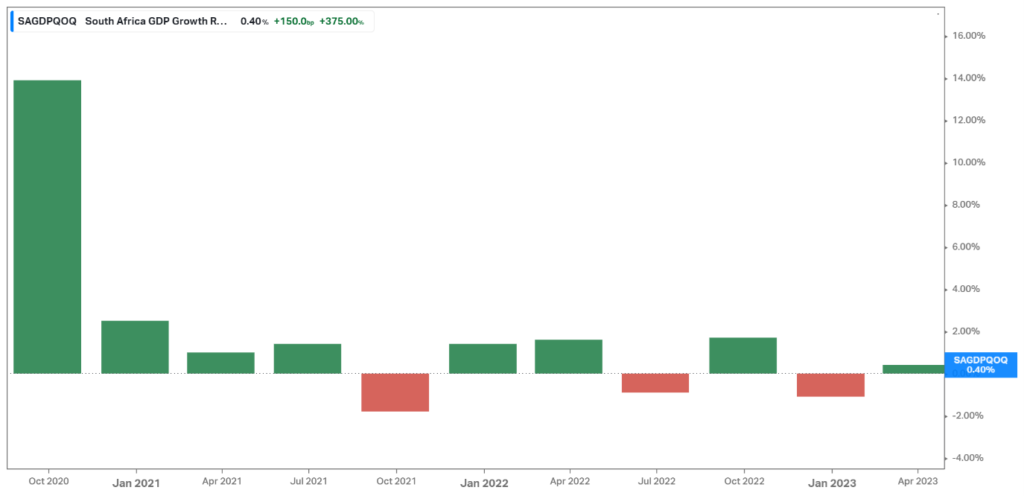

At the beginning of the year, we observed a theme of reducing inflation globally and avoiding a recession in the second half of the year as it was seen that inflation was not transitory as previously assumed. Despite the many factors our country has been facing, we narrowly escaped a recession for South Africa last week, with the growth in the GDP of 0.4% giving South Africa some breathing room. SA Inc has been struggling with 48 JSE-listed companies trading at 52-week lows at the beginning of June 2023, however, the trend is seemingly changing direction. The Euro Zone has been unable to tame the inflation beast and fell into a technical recession last week, leaving their Central Bank with a mammoth task at hand.

Figure 2: South African GDP growth rate

The Rand has also been showing strength last week and closed the week stronger by 4.11% after a move from ZAR19,56 to ZAR18,70 against the Greenback, after reaching its weakest point ever on the first day of June and traded at R19,91/US$ (in the orange circle). The pair has also closed below the 50-day exponential moving average and looking at the 200-day exponential moving average, which is near ZAR18/$. The currency move has been primarily due to macroeconomic events such as CPI and GDP numbers, which have been favourable relatively.

Figure 3: USDZAR price action from March 2022

Local inflation rates have been steadily going down with the latest print coming out at 6,8% which is close to the target range of 3% – 6%. The country has been fighting inflation aggressively from the peak of 7.8%, by increasing the interest rates which are currently at 8.25%. A high-interest rate environment is usually beneficial to banks.

Fundamentals

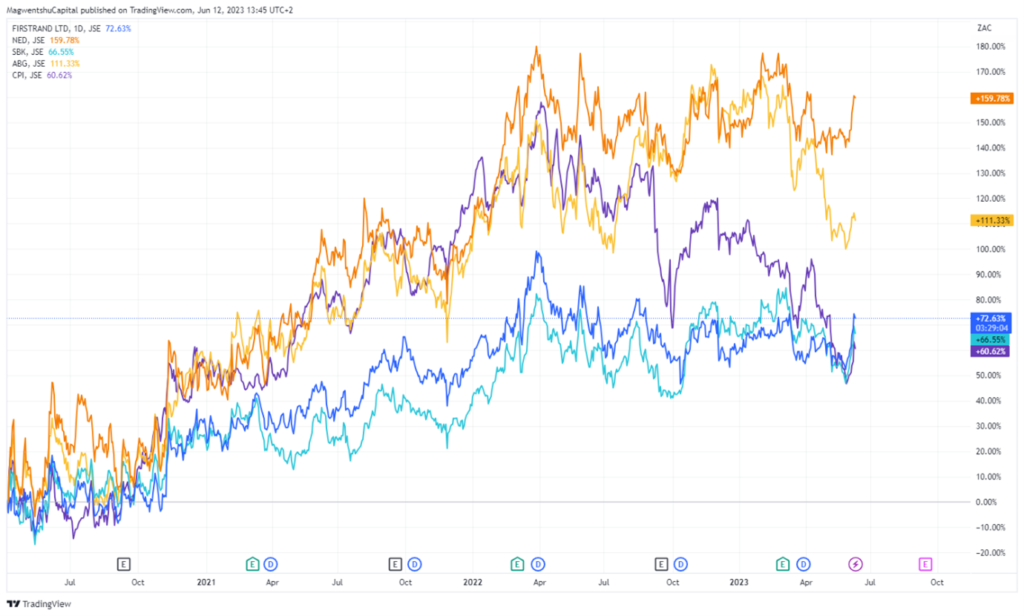

The chart below shows the normalised price action of the big 5 banks in South Africa following the Covid-induced crash, which occurred in March 2020. The chart below illustrates the price action from April 2020 to date. Nedbank Group Limited (JSE: NED) has had the best recovery of close to 195% to date (orange line) and on the opposite end with Capitec Bank Limited (JSE: CPI) having the hardest time at approximately 60% (purple line). Last week, South African Banks were amongst the best performers with FirstRand Limited (JSE: FSR) and Standard Bank Group Limited (JSE: SBK) climbing by 10,54% and 10,81%, respectively.

Figure 4: Normalised chart of the 5 banks since April 2020

The South African banking sector is believed to be robust and currently showing P/E ratios akin to value investing. Starting with ABSA Group Limited, which was the best-performing medium to large-cap share in 2022. The bank’s annual results showed an increase of 15.1% in the total revenue and a 65.6% increase in the dividend payout for the annual results for period which ended on the 31st of December 2022. The results were normalised following the separation for Barclays PLC. Secondly, FirstRand Limited’s (JSE: FSR) performance in their interim results, which were released in March 2023. The company expects the supply of savings to remain above the demand for credit given low confidence. The credit loss ratio is expected to continue to normalise. The company expects its normalised return on equity to June 2023 to remain at the upper end of its stated range of 18% to 22%. Another bank of note is Standard Bank Group Limited (JSE: SBK) which boasted record headline earnings in their latest annual results for the year which ended on the 31st of December 2022 at R34,2 billion. Revenues were boosted by cyclically higher interest rates.

Valuations

Figure 5: P/E valuations for the individual banks

Looking at the valuation of the banks using the Price to Earnings ratio, we see that ABSA Group Limited and Standard Bank Group Limited still have some potential upside of 34% and 13%, respectively. On the opposite end, Capitec Bank Holding Limited’s valuation shows a potential downside of 54% and FirstRand Limited with a downside of 26% according to the P/E valuation.

Summary

A pause in interest rate hikes by the Federal Reserve will be globally appreciated or even better the infamous ‘Powell Pivot’. The interest rates are currently favourable for banks however at the detriment of the consumer and prolonged high-interest rates could lead to banking clients defaulting on their commitments.

Sources: MoneyWeb, FirstRand Limited, Standard Bank Group Limited, ABSA Group Limited, Capitec Bank Limited, Nedbank Group Limited, KoyFin, Trading View and Trading Economics

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.