Costco Wholesale Corporation (NASDAQ: COST) pleasantly surprised the market with its latest quarterly earnings report, achieving a remarkable double beat and delighting shareholders with its most generous special dividend ever, set at $15 per share. The upbeat report triggered a surge in share price to reach an all-time high, underscoring the company’s strong competitive standing in the market following a successful year of adeptly navigating challenging market conditions.

In the first quarter of 2024, revenue demonstrated a robust 6.2% growth, reaching $57.80 billion, surpassing the market consensus of $57.79 billion. Likewise, the company’s earnings per share exhibited impressive resilience, climbing from $3.07 to $3.58, outperforming the forecast of $3.42 and showcasing a formidable display of financial strength.

Technical

On the 1W chart, a breakout occurred at the symmetrical triangle, with the bullish momentum confirmed by the crossing of the shorter-term 25-SMA (green line) above the 50-SMA (blue line) and 100-SMA (orange line). However, at its all-time high, the potential for a pullback triggered by profit-taking behaviour is there, with the RSI indicating overbought conditions.

If the pullback occurs, the first potential level of support is established at $611.80. Should the price move lower, the 25-SMA backed support at $569.45 could be a psychological barrier to the downside momentum, while the 61.8% Fibonacci retracement golden ratio could further prevent a sustainable downturn at $548.65, where the market could hold some buyers.

However, Costco holds an estimated fair value of $706.71 on a discounted cash flow basis. From its current price, this presents a 3.8% potential upside, with the possibility of a widening divergence should the pullback occur.

Fundamental

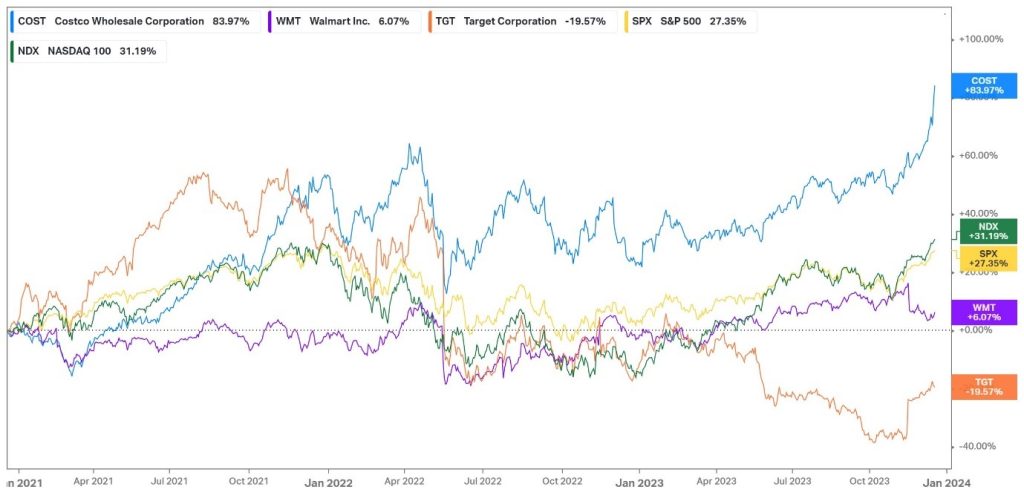

The retail industry, in general, has faced some notable headwinds over the last few years. The biggest of them, perhaps, is the aggressive monetary policy tightening campaign by the Federal Reserve that has heavily impacted consumers’ disposable income. In addition, the resumption of student loan repayments in the US has left another hole in the consumer’s pocket, forcing retailers to engage in price-cutting initiatives to maintain the volumes in their stores. With its membership model, Costco has stood tall in offering a wide variety of goods at affordable prices. Since the COVID-19 pandemic, the company has gained a lot of foot traffic in its stores as consumers traded down to value alternatives, and it has done well since then in keeping these consumers in its stores. Over the last three years, its share price has appreciated over 83%, outperforming all of its industry peers, as well as the Nasdaq 100 (31.19%) and the S&P 500 (27.35%). However, the question now arises: As the price trades at its all-time high, is there still room for appreciation, or is the company’s valuation becoming stretched with its current financial metrics?

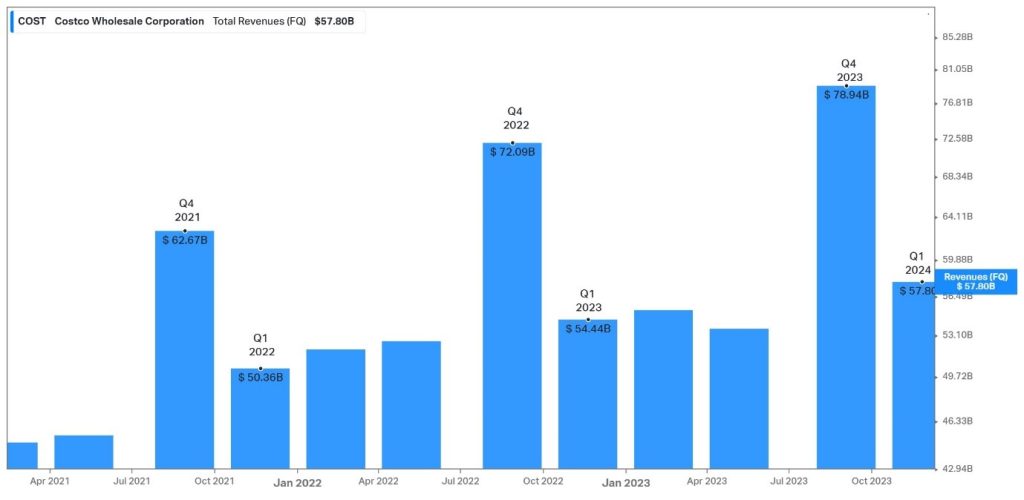

The company’s quarterly revenue over the last few years is shown below. Clearly, its fourth-quarter sales are the strongest every year, but the company has shown a notable improvement in its year-over-year revenue in the current quarter, which is the first quarter of fiscal 2024. Comparable sales for the quarter were up by 3.8% from the prior year, driven by an 11.2% improvement in its international business. In the US, comparable sales advanced by 2%, while its Canadian business showed a 6.4% advance in its same-store sales. Another area of strong improvement came from its e-commerce business, which grew by 6.3% year-over-year. This business contains more bigger-ticket items, and the growth in the segment suggests that consumers are slowly starting to spend on discretionary products again. Management acknowledged that appliance sales were up over 20%, while TV sales were up in the high single digits. Due to lower freight costs, the company was able to maintain lower prices for these bigger ticket items, which could be a likely driver of the increased demand as the Federal Reserve shows promise of potential rate cuts in the upcoming year, which could bode well for consumer spending trends and the retail industry in general.

A crucial factor playing into the optimism around Costco’s operations is its membership model. In the latest quarter, membership fee revenues were up by 8.2% at $1.08Bn, while the company expanded its paid household members by 7.6% to an astonishing 72M paid household members. Its Costco cardholders were up by 7.1% at 129.5M, highlighting the impressive customer base the company has built up. This could likely help them maintain the foot traffic in its stores when customers start reverting back to bigger-ticket purchases and a more discretionary-based spending trend should interest rates edge lower in the near future. Additionally, the market is expecting an increase in its membership fee soon, which could provide an additional boost to its top line once the increase is implemented across its impressive customer base.

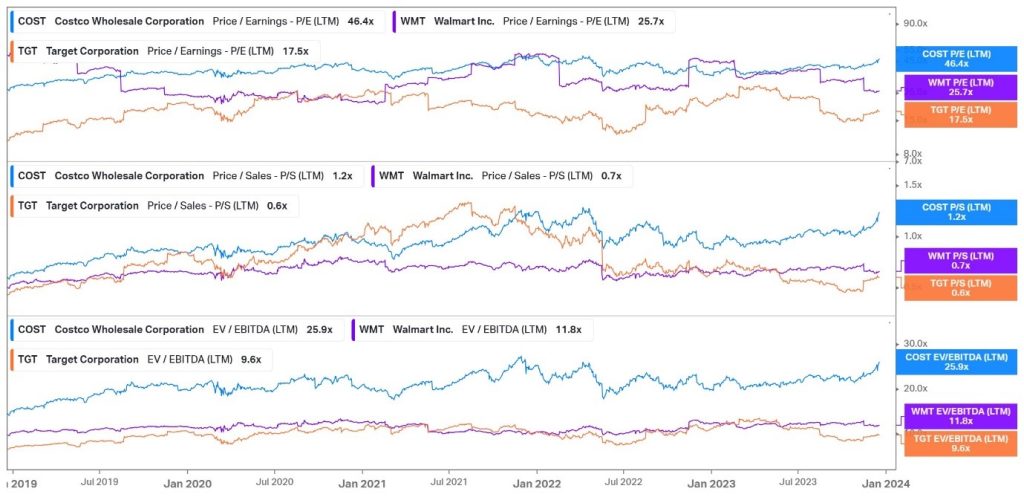

There is clearly a lot to be excited about when it comes to Costco and its positioning in the market. However, due to its 84% expansion over the last three years and the optimistic response to its latest earnings report, the shares are trading at an all-time high. While this does not mean that there is no more potential for upside, it seems to be teetering on the edge of being overvalued on a comparable basis compared to its industry peers. Its P/E (46.4X), P/S (1.2X) and EV/EBITDA (25.9X) multiples are all the highest among its peers, suggesting a slight premium to its price. Whether this premium is justified by its forward-looking prospects remains up to interpretation.

Summary

Costco Wholesale Corporation is trading at all-time highs after delivering a double beat in its latest quarterly earnings report. Its estimated fair value of $706.71 presents a 3.8% potential upside should the current momentum continue in the upcoming sessions.

Sources: Koyfin, Tradingvew, Reuters, Yahoo Finance, Costco Wholesale Corporation, Investor’s Business Daily

Piece written by Taan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.