Intriguing times are upon us as the market anticipates PPC Ltd.’s (JSE: PPC) recent quarter performance report, due on the 20th of November 2023. PPC has cemented itself as a steadfast participant in Africa’s cement and building materials arena.

As the eagerly anticipated quarterly earnings report release approaches, the market could closely scrutinise the company’s revenue growth, cost management strategies, and overall outlook. The diamond in the cement crown awaits those who explore this enigmatic world, recognising PPC Ltd’s strengths and evaluating its merit within their investment portfolios.

Technical

The daily chart shows that PPC Ltd’s current price at R2.80 hovers above a significant historical level. While it flirts with this level, the stock holds an “undervalued” status after the discounted cash flow model estimated a fair value of R3.28 (green line) ahead of its earnings release.

The technical indicators reveal a stock poised for upward momentum. The stock finds itself above both the 100-SMA (blue line) and the 200-SMA (red line), signalling strength and resilience. However, it’s essential to note that it’s currently trading below the 50-SMA (green line), a level that might serve as a pivot point.

The Relative Strength Index (RSI) stands at 47.02, with a gradually declining RSI-based Moving Average (MA) at 45.42. This gives rise to expectations of a sustained push towards R3.00, which could offer a potential for a 9.5% upside as the share converges towards its estimated fair value. For those wary of market fluctuations, the immediate support level sits at R2.57, with a potential buy-the-dip level at R2.36.

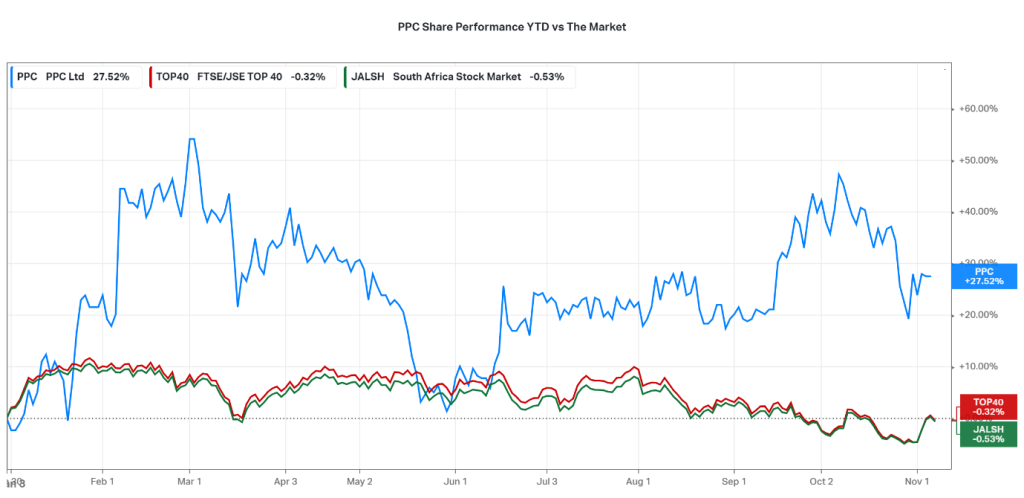

Share Performance Year-To-Date

PPC Limited has displayed remarkable resilience and positive growth in its share price over the year-to-date period. As of the current date, the company’s share price has appreciated by an impressive 27.52%. This significant increase is a reflection of the company’s ability to navigate challenges in the construction and cement industry while capitalising on opportunities for growth.

This is in stark contrast to the JSE All-Share Index (green line) and JSE Top 40 Index (red line), which have both returned negative returns of -0.53% and -0.32%, respectively.

Source: FairMarkets Australia – Koyfin, Mfanafuthi Mhlongo

Fundamentals

Positive outlook for the cement industry:

The global cement industry is expected to grow in the coming years, driven by urbanisation and infrastructure development.

Looking at the cement industry in South Africa and the rest of Africa could continue to boost investor sentiment towards the company and industry as a whole. The cement industry’s trajectory points towards sustained growth, bolstered by urbanisation and the pressing need for infrastructure development. PPC Ltd’s strong market presence, coupled with its commitment to innovation and expansion, underscores its readiness to harness this growth.

Market Position in Africa and the Middle East:

PPC Ltd is not merely a spectator in the grand arena; it’s a gladiator. The company has strategically entrenched itself in South Africa, Botswana, Zimbabwe, and Rwanda, garnering an advantageous foothold. These regions are not just geographic locations; they are the gold mines of economic expansion and infrastructure development. PPC Ltd has built its empire on these shores, and its reign is set to continue, paving the way for growth opportunities.

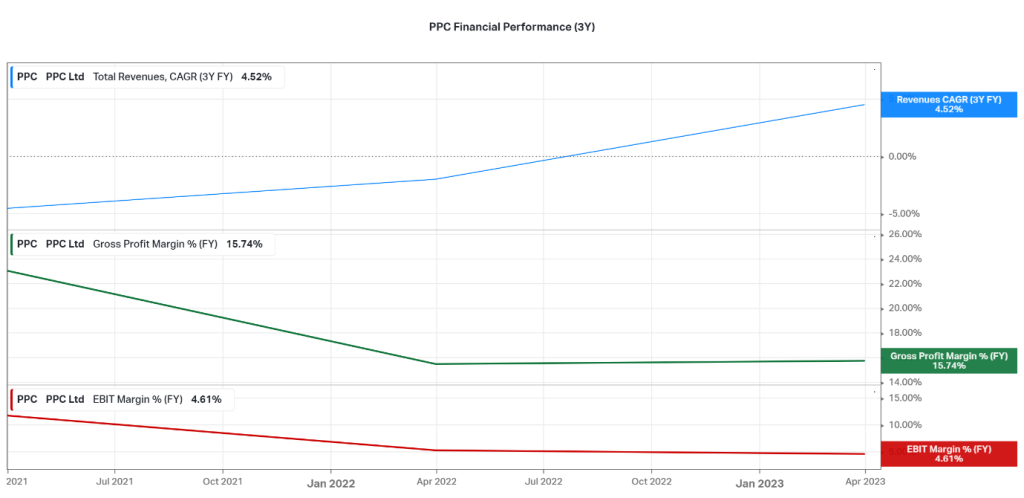

Improved financial performance:

PPC has reported improved financial results in recent quarters, with revenue and earnings growth exceeding market expectations. This has been driven by a number of factors, including higher cement prices, cost control, and favourable exchange rates.

Analysing the past three years, PPC Ltd has achieved a compound annual growth rate (CAGR) of 4.52% in total revenue, a testament to its upward trajectory. Its gross profit margin, standing at 15.74%, mirrors prudent financial management. Though its EBIT margin over the same period is at 4.61%, PPC Ltd has striven to optimise profitability amidst economic fluctuations.

Source: FairMarkets Australia – Koyfin, Mfanafuthi Mhlongo

Attractive valuation:

PPC shares are currently trading at a valuation discount to its peers. This makes the stock attractive to investors looking for value opportunities.

Currently, PPC Ltd’s shares are trading at an attractive valuation relative to its peers. This makes the stock appealing to investors seeking both value and growth potential. The P/E ratio of 6.3x indicates that investors are willing to pay 6.3 times the company’s earnings for each share, suggesting an undervalued stock.

Source: FairMarkets Australia – Koyfin, Mfanafuthi Mhlongo

Long-term Growth Potential:

The cement industry’s trajectory points towards sustained growth, bolstered by urbanisation and the pressing need for infrastructure development. PPC Ltd’s strong market presence, coupled with its commitment to innovation and expansion, underscores its readiness to harness this growth.

Potential Threats:

Acknowledging a balanced view, we must be mindful of potential threats. Economic downturns in regions of PPC Ltd’s operation pose a risk to sales and earnings. Given a substantial portion of its revenue is generated in foreign currencies, currency volatility looms as a significant concern. The competitive landscape, too, remains a factor capable of influencing prices and margins.

Summary:

PPC Ltd emerges as a potent contender in the cement and building materials sector, laden with untapped potential. While short-term adversities such as rising input costs and economic headwinds in South Africa may cast shadows, PPC Ltd’s commitment to sustainable growth innovation and its undervalued status presents an enticing investment prospect.

Sources: TradingView, Benzinga, MoneyWeb, MarketWatch, Reuters, KoyFin, PPC, Dow Jones Newswire, MT Newswire, CNBC.

Piece Written by Mfanafuthi Mhlongo, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.