Eli Lilly and Company (NYSE: LLY) reported its latest quarterly performance last week, showcasing an ongoing display of dominance. The pharmaceutical juggernaut surged ahead with a remarkable 5% increase in its stock price, marking yet another remarkable stride.

At the heart of its success is the tremendous surge in demand for dietary drugs, catapulting the company’s revenue to a staggering $9.5 billion. This figure soared high above the consensus forecast, leaving behind the prior estimate of $6.94 billion in the dust. Eli Lilly has demonstrated a phenomenal ability to surpass expectations, setting new benchmarks for its industry peers. While adjusted earnings per share took a temporary dip, sliding to $0.10 from the previous $1.98, it’s crucial to note that this decline was due to non-recurring charges associated with in-process research and development (IPR&D). Excluding these exceptional charges, Eli Lilly would have delivered solid bottom-line growth, exemplifying its underlying strength and potential.

As we journey forward, the question that lingers in the air is whether Eli Lilly can sustain its remarkable upward trajectory. With its consistent ability to defy expectations and capitalize on surging demand, the path ahead promises to be an exciting one.

Technical

On the daily chart, a clear uptrend has emerged, confirmed by the emergence of the 25-SMA (green line) above the 50-SMA (blue line), above which the share price has recently broken. Higher highs and higher lows confirm the trend’s strength despite a recent pullback, with support from the multiple SMAs paving a path to continued upside.

However, resistance at $610.32 presents a hurdle to the current momentum, which could result in another temporary retracement in the price. In this case, the 50-SMA support at $571.77 could be crucial, offering support above the dynamic support of the uptrend at $552.98. Lower support is established at $543.08 and $522.12 if the pullback sustains, which could be potential interest levels in the upcoming sessions.

In contrast, failure of the resistance at $610.32 could clear the path for the share price to converge with its estimated fair value of $629.85. From current levels, this presents a 5% potential upside on the current fundamentals.

Fundamentals

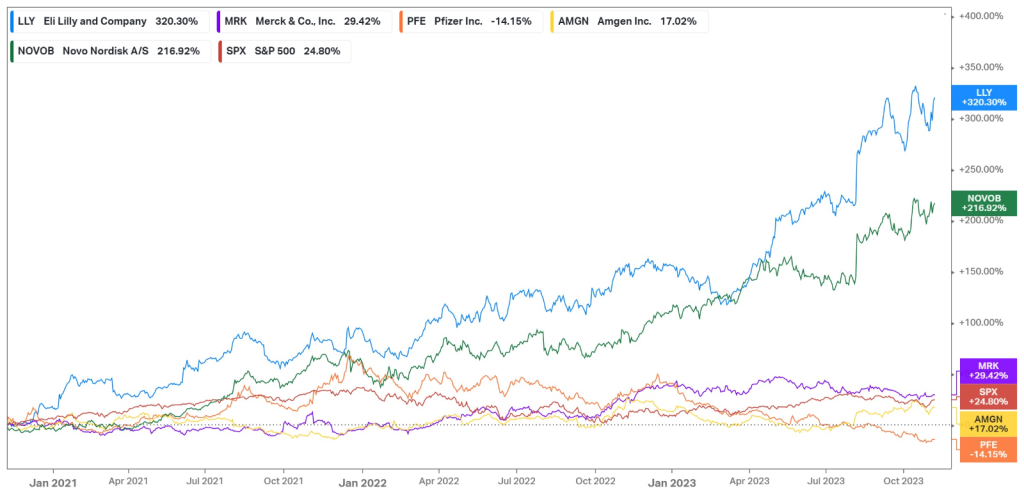

Over the last three years, Eli Lilly and Novo Nordisk have emerged as clear frontrunners in the industry, realizing impressive price returns of 320.30% and 216.92%, respectively. These returns outperform the S&P 500 (24.80%) quite convincingly over this period while leading competitors like Merck & Co (29.42%) and Amgen (17.02%). The main driver of the optimism was the immense takeoff of dietary drugs like Ozempic, Wegovy, and Mounjaro, which has taken the pharmaceutical industry by storm. On top of its growing top line, the pharmaceutical industry also provides insulation against the potential downturn in the business cycle, which contributes to the company’s attractiveness as the economy navigates a lot of uncertainty.

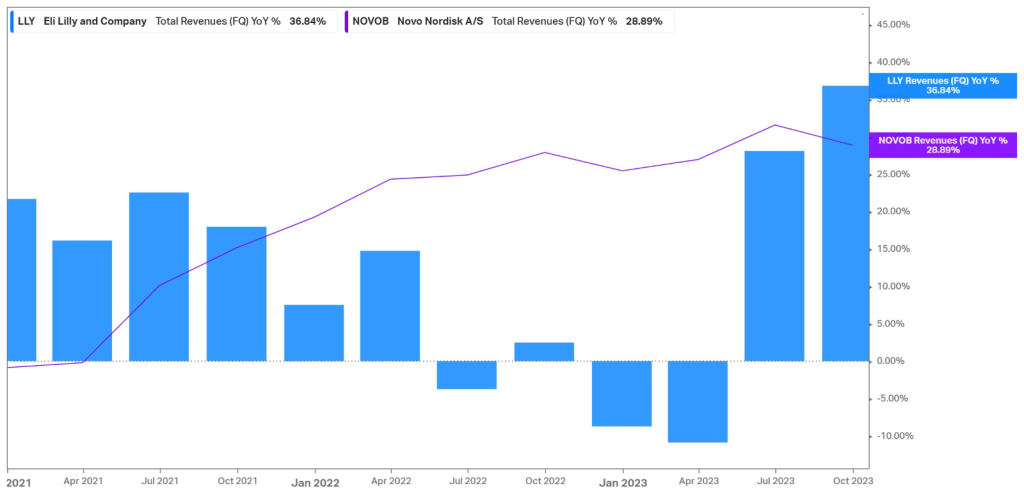

The graph below shows Eli Lilly’s impressive pivot in revenue growth over the last two quarters after two successive quarters of negative growth. This stands in contrast to its competitor, Novo Nordisk, which has shown a more stable revenue trend over the last few years. Nonetheless, the company’s diversified product portfolio, which focuses on neuroscience, cardiometabolic, cancer, and immunology, shows optimistic signs of expansion. In the latest quarter, its 37% growth in revenue was mainly attributed to Mounjaro, a diabetes drug that saw its top line increase from $187.3M in the same quarter last year to a massive $1.41Bn. Similarly, Jardiance, another diabetes drug, saw a 22% surge from $573.3M to $700.8M. Verzenio, which is a cancer drug, grew by 68% from $617.7M to $1.04Bn, while its more minor drugs, Tyvyt and Retevmo, expanded by 50% and 56%, respectively. Overall, volumes were up by 31%, while its price realization improved by 6%, rounding off a solid top-line quarter.

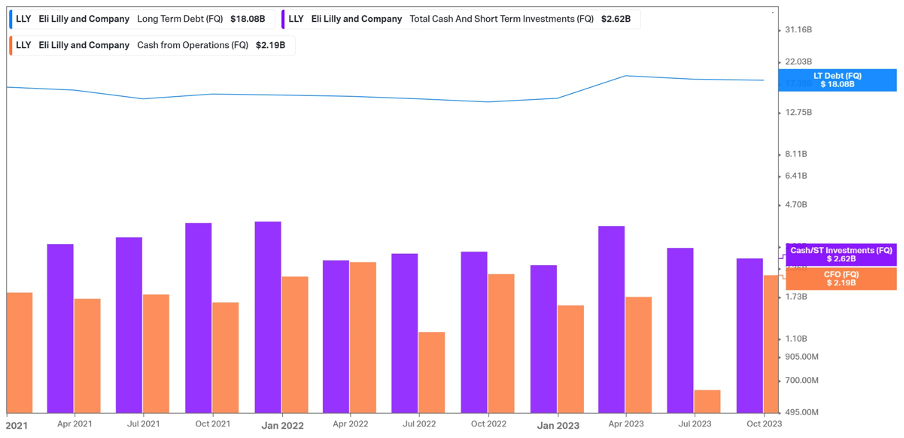

However, a concerning picture arises when looking closer at the company’s balance sheet. With a lot of growth opportunities in the industry coming from acquisitions and strategic investments, the company’s ability to capitalize on these opportunities could be impaired. Its long-term debt position of $18.08Bn lies far above what the company can cover with its current cash position and the cash it generates from its operations. As the debt comes due, the company may be unable to continue investing in growth avenues to the same extent as it currently is without further leveraging its operations. As a result, much focus could be placed on the sustainability of the current dietary drug storm as a revenue driver for the company as we advance, which could result in a stronger cash flow in the upcoming years.

This is further demonstrated by the graph below, which shows the strong uptick in the company’s R&D expenditures in recent quarters. While this generally paints a promising picture for growth, its slumping free cash flows do not. Without sufficient cash flows to back these R&D expenses and its investment into growth avenues, the company may have to continue funding these investments with additional debt, which could catch up to them long-term. However, this is not as much of a near-term concern but rather something to keep an eye on to determine whether the completion of the company’s acquisitions of DICE Therapeutics, Inc., Versanis Bio, Inc., Emergence Therapeutics AG, and Sigilon Therapeutics, Inc. would generate sufficient cash flows to service its current debt.

Summary

Driven by the immense demand for weight loss and diabetes drugs in the pharmaceutical industry, Eli Lilly has continued its 64% year-to-date price return after a stellar quarterly earnings report. With an estimated fair value of $629.85, there could still be more upside ahead if the company can generate sufficient cash flows from its acquisitions to service its large debt position and maintain its balance sheet health.

Sources: Koyfin, Tradingview, Wall Street Journal, Invesor’s Business Daily, Yahoo Finance, Eli Lilly and Company.

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.