Exxaro Resources Limited (JSE: EXX), a prominent player in the energy sector, has recently sounded the alarm bells with a dramatic plunge in both its revenue and profits, setting the stage for a high-stakes battle in the tumultuous South African market. The company finds itself at a pivotal crossroads, grappling not only with the rollercoaster ride of commodity prices, which have descended from the lofty heights of 2022, but also with an array of logistical challenges that have compounded its woes. As we advance, this narrative is one of resilience and determination as Exxaro confronts an arduous six-month journey, striving to reshape its fortunes and orchestrate a remarkable turnaround within the dynamic and demanding energy sector.

For the six months ended 30 June 2023, the company reported revenue of R18.9Bn, a 15% reduction from the R22.3Bn in the year-ago period. As a result, its profit plunged 33% from R9.2Bn to R6.3Bn. Headline earnings per share (EPS) followed suit, dropping 28% from 3426 cents to 2443 cents, rounding off a challenging six months, during which the interim dividend on the company’s stock fell from 1593 to 1143 cents per share.

Technical

On the 1D chart, a descending wedge has experienced a breakout to the upside, forming a new uptrend, confirmed by the crossing of the 25-SMA (green line) above the 50-SMA (blue line). The intraday momentum also tilts to the upside as the share price trades above the daily pivot point at R175.07.

In the near term, resistance is established at R179.16. On current momentum, clearing this resistance could trigger the path to convergence with its estimated fair value of R185.83. From current levels, this presents a 4.4% potential upside.

However, the possibility of a pullback remains on the cards if resistance at R179.16 halts the upside momentum. In this case, a reversal toward support at R170.61 and R166.50 could reverse the recent gains, where neckline support is established at R158.31. At this level, the potential upside to its estimated fair value is stretched to 17.4%.

Fundamental

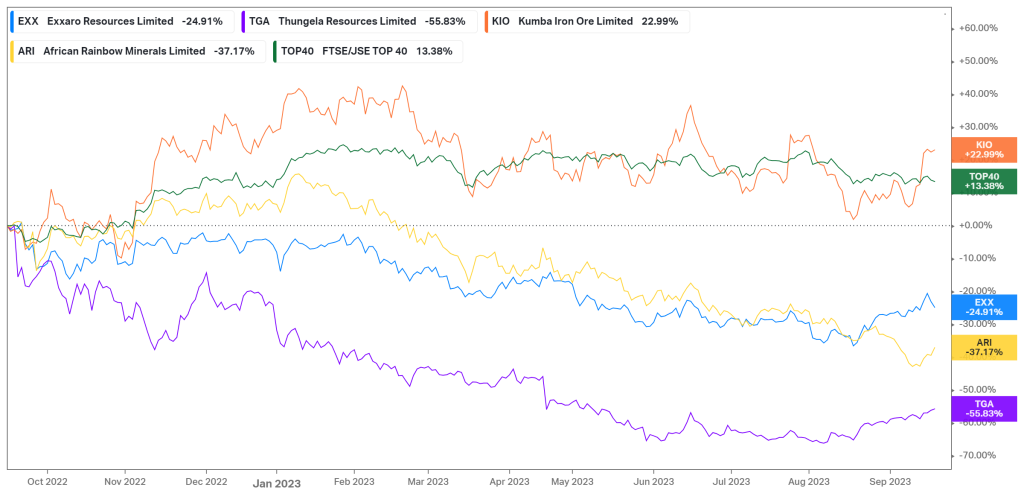

Due to its logistical and commodity price challenges, Exxaro (-24.91%) and its industry peers, Thungela Resources (-55.83%) and African Rainbow Minerals (-37.17%) have been under intense pressure over the last year. Only Kumba Iron Ore (22.99%) has realized a positive price return over the same period due to its exposure to iron ore, which has not faltered in the same capacity as coal. With the JSE Top 40 returning 13.36% during this time, it is no secret that the South African energy market has underperformed significantly. However, with these major price reductions, could there be an opportunity to gain exposure to this industry at lower valuations?

In 2022, coal prices peaked due to a surge in demand from Europe, as a ban was imposed on Russian coal due to its invasion of Ukraine. Due to limited supply and rising demand, prices advanced rapidly, and Exxaro, which generates most of its revenue from coal, followed suit. In the latest earnings report, R17.56Bn of its R18.94Bn revenue came from coal, representing 93% of its total revenue. Unsurprisingly, there is a correlation between Exxaro’s share price and the price of coal due to this dependence. This relationship is shown below, as Exxaro tracks the performance of coal relatively closely. Over the last six months, prices have fallen as the market continued to return to normalization, but it seems to have bottomed out in August. During this time, Exxaro’s share price broke through the descending wedge and started its uptrend. The recent reversal in the coal price is bullish for the company, as it could trickle over into a revenue recovery in the second half of the year if current fundamentals hold firm.

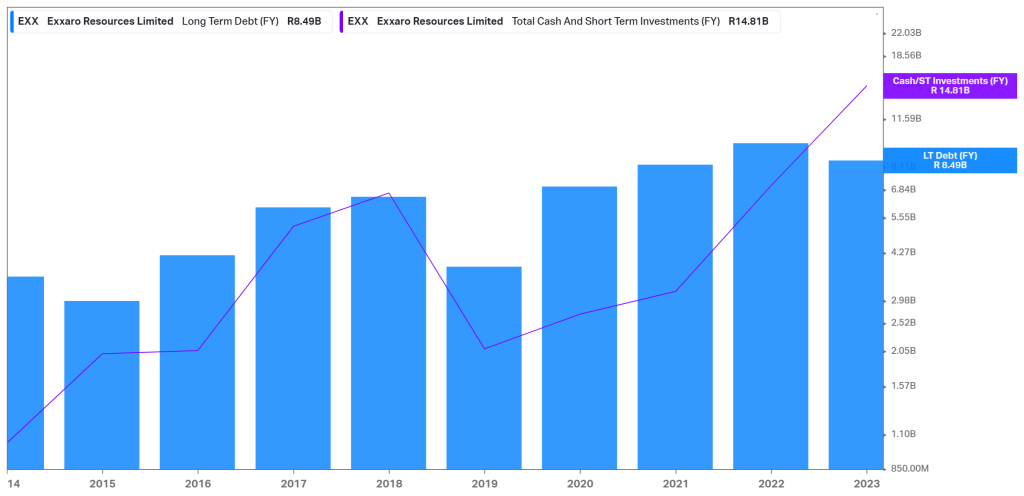

Regarding its balance sheet, executives have recently announced the company’s plans to build up a cash balance of up to R15Bn to fund acquisitions in its search for clean energy minerals. This venture toward finding cleaner energy sources reflects a seismic shift in the energy market, with Exxaro looking to reduce its dependence on coal. However, this could mean that the company is concerned about its ability to access debt markets to fund these potential acquisitions, which could cause concern for investors. However, its current debt structure shows that its cash and short-term investments more than cover outstanding long-term debt, as demonstrated below. The concern comes in when looking at the debt ladder. In less than six months, the company has R407M in interest-bearing securities coming due, with another R991M within six to twelve months and R756M between one and two years. Within two to three years, R3.12Bn of the company’s debt will reach redemption, which could result in cash outflows to retire the debt. In this case, for the company to maintain its goal of keeping the cash pile between R12Bn and R15Bn, management may have to sacrifice some earnings potential to shareholders in the form of dividend payouts to avoid sacrificing its ability to reinvest into the growth prospects of the business.

Headwinds in state-owned logistics firm Transnet continue to threaten the company’s top and bottom lines as we advance. Transnet is dealing with shortages in locomotives, cable theft, and vandalism of its infrastructure, which limits the capabilities of South African coal miners to haul minerals to port. Rand volatility is another risk to the company’s business, as it exports R5.67Bn of its revenue. R2.55Bn of these exports are attributed to Europe, mainly Switzerland and Germany, while another R2.82Bn goes to Asia, primarily Japan and Singapore.

Summary

While battling many headwinds, Exxaro reported a sluggish earnings report for the six months ending 30 June 2023, with revenue and profit dropping by 15% and 32%, respectively. However, with the coal price looking to recover, there could be a potential opportunity at lower valuations, as the estimated fair value presents a 4.4% potential upside from current levels.

Sources: Koyfin, Tradingview, Reuters, Exxaro Resources Limited

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.