In its most recent earnings update for the fiscal year ending in June 2023, Discovery Limited (JSE: DSY) pleasantly surprised its investors by announcing the resumption of dividend payouts, marking a significant milestone since the challenges posed by the COVID-19 pandemic back in 2020. Despite a year characterized by formidable challenges, intricacies, and volatility, Discovery showcased its formidable financial prowess through robust cash flow generation and a resilient balance sheet. This financial strength and stability ultimately convinced the company’s leadership to reward shareholders with a valuable 110 cents per share dividend.

The company reported a 24% increase in its normalized operating profit, which now sits at R11.66Bn, resulting in normalized headline earnings of R7.68Bn, up 32%. The rise in operating profit was mainly attributed to solid growth in premium income, with its core new business annualized premium income (API) advancing 12% to R22.8Bn. However, despite the solid performance, management acknowledged that macroeconomic uncertainty would persist through the upcoming year, with the share price contracting close to 1% on the day of the release.

Technical

On the 1D chart, a descending channel has formed, with the crossing of the 25-SMA (green line) below the 50-SMA (blue line) confirming the bearish pressure. The daily pivot point at R145.73 provides resistance to the upside, as intraday momentum also favours the downside, putting the temporary breakout from the channel at risk of an immediate correction.

From the late July peak, the 50% Fibonacci retracement offers support at R144.90, which could aid a potential break through the pivot point. In this case, a leg above the resistance at R148.02 and R148.78 (R2) could confirm a sustainable uptrend from the channel breakout toward R151.14 and R153.93. The estimated fair value of R157.47 is then within reach, presenting an 8.3% potential upside from current levels.

However, failure to move above the pivot point could result in a temporary pullback within the prior channel at R142.68 (S2). If the Fibonacci golden ratio at R141.38 fails to provide support, the downtrend could continue toward R138.67, where the potential discount from the estimated fair value stretches to 13.57%.

Fundamental

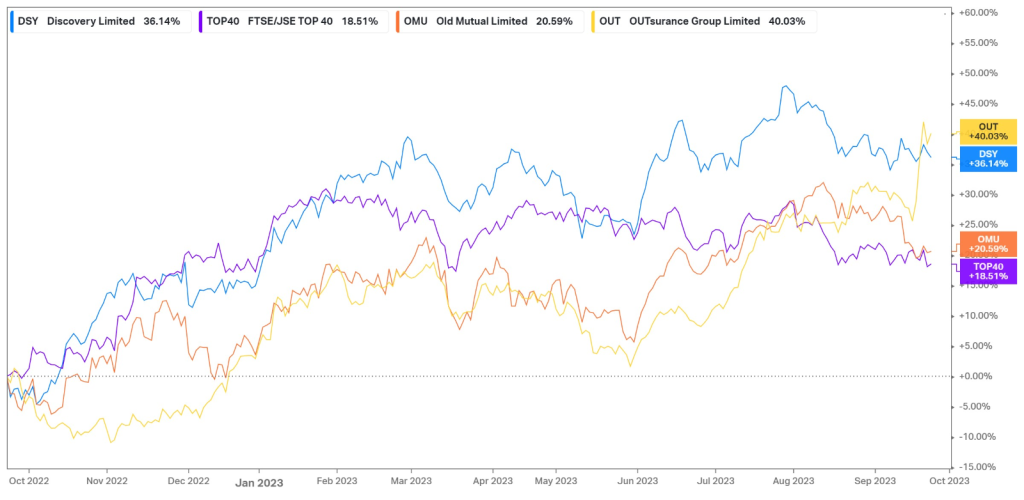

Over the last year, Discovery’s share price has appreciated an impressive 36.14%, lagging behind OUTsurance (40.03%) but outperforming both OldMutual (20.59%) and the JSE Top 40 Index (18.51%). Despite a steep rise in interest rates in its key insurance markets, namely South Africa and the UK, the company has displayed resilience across all of its business segments. Prolonged inflationary pressures and rising interest rates affected the company’s bottom line, but its liquidity, solvency, and cash flow generation remained robust. Additionally, a weaker rand over the period aided the profitability of its Vitality Global segment, while healthy customer retention and premium income rounded off a solid operational year, showing encouraging signs of resilience in the face of challenging economic conditions.

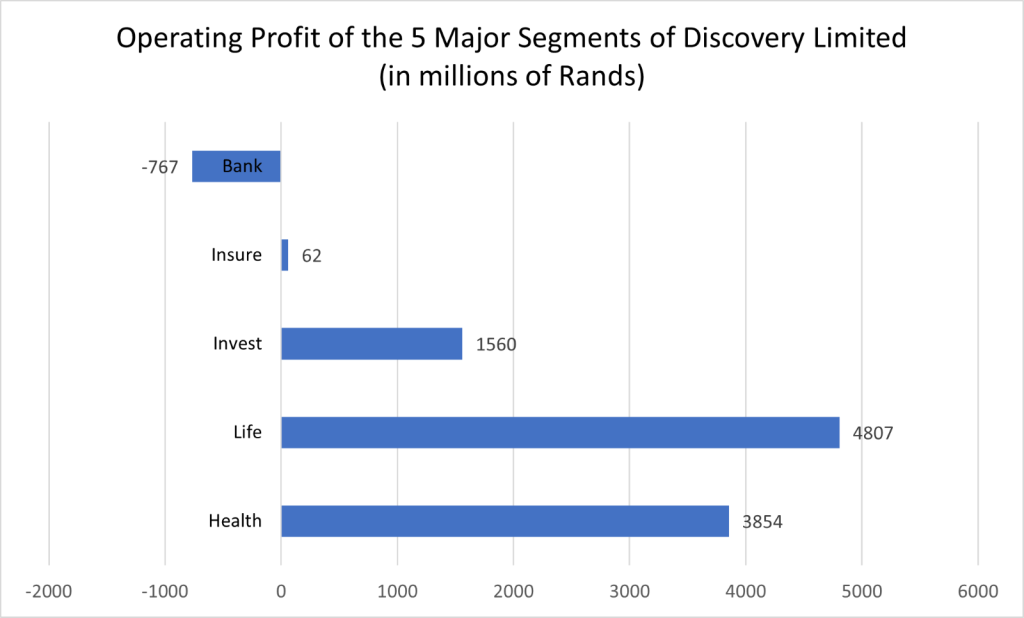

The graph below displays the operating profit breakdown of Discovery for its latest financial year, highlighting the fact that its Discovery Life segment remains the largest profit generator, with its profit expanding 19% to R4.8Bn. Following the high number of COVID-related claims in the prior period, this segment realized stronger cash flow generation, which aided the company’s return to paying dividends. Its second-largest profit generator, Discovery Health, advanced its bottom line by 7% to R3.9Bn and now holds 57.8% market share in the South African market. Discovery Invest produced R1.6Bn in operating profit, with assets under administration advancing 15% to R140Bn. In its smaller segments, Discovery Insure’s normalized operating profit advanced 138% to R62M, with gross written premiums expanding 10% to R5.3Bn. However, much focus was put on Discovery Bank, which suffered a loss of R767M. However, This loss does not reflect the bank segment’s full performance. The company managed to grow its number of accounts by 60% to 1.6M, with total clients expanding 49% to over 700,000. Retail deposits were 36% higher at R14.3Bn, while the company delivered on its medium-term target of averaging 1,000 new clients per day. Its credit applications were 56% higher, which led to the bank gaining market share, claiming that its share of new credit issued was 15.7% of credit card facilities in Q2 2023, compared to 10.9% in the prior year. Despite this loss in the Discovery Bank segment, the company’s overall South African operations grew its operating profit by 22%, with 21% growth in the UK, and the Vitality Global segment growing its profit by 74%, benefitting from a weaker rand during the year.

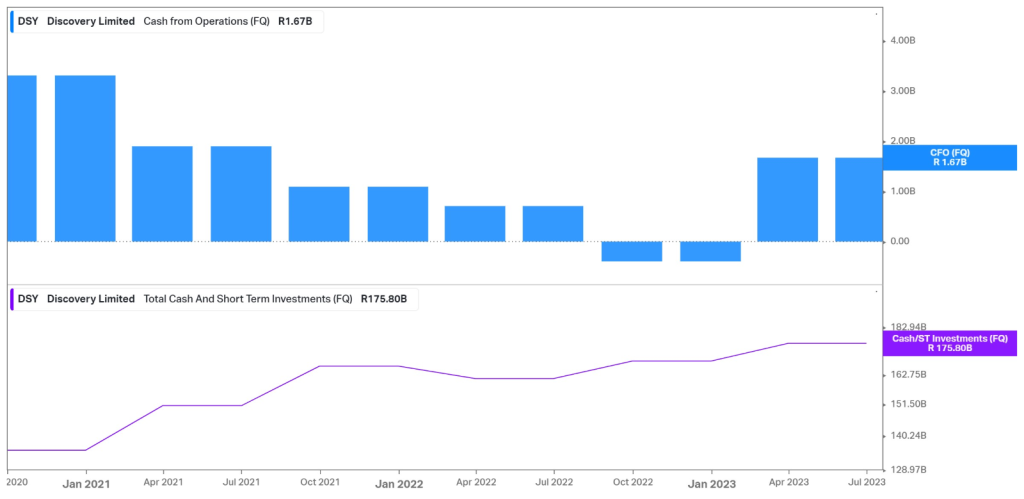

The company declared a R1.10 dividend per share after not paying a dividend in the final year. What allowed it to return to paying these dividends was its strong cash flow-generating ability. The graph below shows the company’s recovery to positive operating cash flows in the recent two quarters after recently falling into negative territory. In its latest financial year, the company generated R2.55Bn in cash from operations while holding cash and short-term investments worth R175.80Bn. This reflects a healthy balance sheet, with the long-term debt standing at R15.82Bn, reflecting the company’s ability to cover its liabilities while remaining solvent in its ability to cover its claims. Discovery operates with a debt/equity of 32.2%, falling from 45.8% a couple of years ago. Its interest coverage is strong, with an EBITDA/Interest expense of 3.9X and a Debt/EBITDA of 2.0X.

Summary

Discovery Limited recently delivered its latest full-year earnings report, showcasing resilient performance across its segments, resulting in a 24% rise in operating profit. Its core new business API advanced by 12%, resulting in solid cash flow generation. With its healthy balance sheet, the company declared a dividend of R1.10 per share, signalling confidence in its ability to weather harsh macroeconomic conditions. With its estimated fair value at R157.47, the company presents an 8.3% upside potential from current levels.

Sources: Koyfin, Tradingview, Reuters, Discovery Limited

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.