After reporting a disappointing annual report in August, Impala Platinum Holding Limited (JSE: IMP) added to its recent struggles that have contributed to a 61% year-to-date contraction in its share price. CEO Nico Muller mentioned the rapid decline in palladium and rhodium prices, which adversely squeezed its profit and forced the company to slash its dividend and focus on cost-cutting. The industry-wide contraction has hit other industry players just as hard, with Anglo-American Platinum CEO confirming his expectations for the lower metal prices to persist, painting a dire picture for the industry’s prospects as we advance.

Impala’s revenue for the year to June 30 contracted from R118.33Bn to R106.59Bn, causing basic earnings to slump from R32.05Bn to a measly R4.91Bn. Headline earnings declined 41% to R18.8Bn, with the company cutting its full-year dividend by 65% to R5.85 per share. Management’s guidance for the upcoming year did little to console investors, as the low revenue and earnings are expected to persist in the upcoming year.

Technical

On the weekly chart, a descending triangle breakdown has resulted in a sustainable downtrend, currently trading close to the 78.6% Fibonacci retracement at R77.11. A death cross has formed, with the 200-SMA (orange line) crossing above the 50-SMA (blue line), while the 25-SMA (green line) trades far below, confirming the bearish momentum.

With volume remaining elevated, the current trend could continue, with the first level of support at R50.89. Neckline support at R15.40 could then come into play in the longer term if the momentum is sustained, potentially resulting in another 80% downside from current levels if fundamentals remain unchanged.

However, with the RSI indicating oversold conditions, the downtrend could be at risk of a reversal, where resistance at R124.81 could be a level of interest at the 61.8% Fibonacci golden ratio. The 25-SMA resistance could limit the upside, where a breakout could confirm a sustainable trend reversal toward R158.31 and the estimated fair value of R185.76, presenting a 115.04% potential upside if the current fundamentals shift in the company’s favour.

Fundamental

In the latest year, Impala saw its share price contract by 54.80% but still performed slightly better than its counterpart in Anglo American Platinum, which saw a 55.31% reduction in its share price over the same period. However, it becomes evident why these decreases have occurred when looking at the price performance of the platinum group metals (PGM) since November last year. Rhodium has declined over 70% during this time, with Palladium following closely with a 48.7% contraction. Platinum has weathered these conditions better, only declining by 4.10%, but barely offsets the effect of the other metals on the company’s bottom line. With no potential signals suggesting a turnaround in this performance, the metals and mining companies in South Africa could face some challenging times ahead, with cost-cutting in the spotlight as the companies strive toward maintaining margins in the current operating environment.

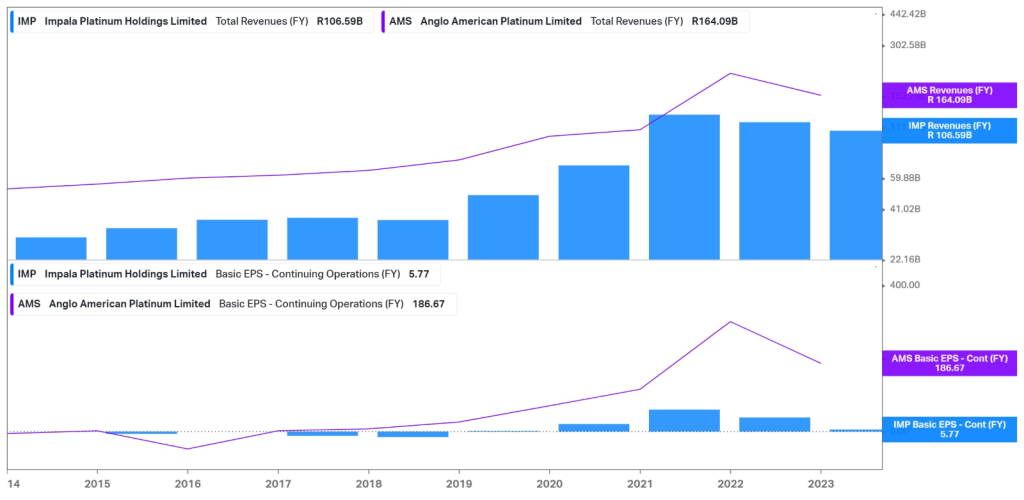

The graph below shows the top-line decline in the latest financial year, showing a sharp decline across the industry over the last two financial years since performance peaked during 2021 and 2022. Impala had been making record returns when Russia initially invaded Ukraine earlier last year, which boosted metal prices to unprecedented levels. Rhodium soared to $31,000 per ounce, with Palladium trading close to $3,400 per ounce. At the moment, Rhodium trades closer to $4,100 per ounce, while Palladium has slumped to a five-year low of around $1,152 per ounce. These rapid declines caught Impala’s management off guard, as the slower-than-expected growth in China delivered a massive hit to metal prices. While it was expected that the 2022 peaks could not be sustained, the rate of the decline was the issue, leaving the company with a massive reduction in both its top and bottom lines.

Higher inflation, lower refined production, and a retracement in rand pricing further weighed on the company’s margins, which have similarly decreased, as shown below. Rolling power cuts in South Africa hit production, resulting in Impala’s platinum metal output falling by 4% to 2.9M ounces. Its gross profit margin fell from 34.89% to 20.96%, while its EBIT margin similarly fell from 34.39% to 20.17%. Management also warned of group unit costs that could rise another 6% to 10% in the upcoming quarters, which could further strain its margins. However, production is set to increase again if the company can incorporate the assets from Royal Bafokeng Platinum, which they recently acquired. Refined PGM output is expected to rise to between 3.3M and 3.45M ounces, which could offset the higher costs as we advance.

Summary

Domestic metal and mining companies have felt the strain from the rapidly declining metal prices, which is eating into their margins. At the same time, Eskom’s increased load-shedding considerations limit the production potential. However, acquiring Royal Bafokeng Platinum could provide the resources necessary to return to scale and offset some of the rising input costs that are weighing on the bottom line. As we advance, levels to look out for are support R77.11, where the company could enforce a reversal on the oversold RSI toward resistance at R124.81. The estimated fair value at R182.60 still offers a 115.04% potential upside if the fundamentals improve in the longer term.

Sources: Koyfin, Tradingview, Impala Platinum Holdings Limited

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.