Following Target Corporation’s impressive 17% surge in share price post their recent earnings report, investors were hopeful that Walmart Inc. (NYSE: WMT) would follow suit, leading to a remarkable ascent to a new record high in its share price. However, the outcome of Walmart’s third-quarter earnings report took a different turn. Despite surpassing expectations with a 5.2% revenue increase to $160.8 billion (above the consensus of $159.55 billion) and a 20% rise in earnings per share (EPS) to $1.53 (surpassing the $1.52 consensus), the market response was unexpected—a sharp decline of over 8%, which resulted in a $35Bn loss in the company’s value.

This significant one-day price drop, the most substantial since July 2022, was attributed to management’s cautious outlook on the health of the US consumer. Acknowledging a weakening in consumer spending towards the end of October compared to earlier in the quarter, management highlighted a more cautious consumer approach as the holiday season approached—an especially critical period for retailers.

Now, the question arises: is the market’s reaction an overblown response, or does it signal the beginning of a potentially challenging phase for the world’s largest retailer?

Technical

On the 1D chart, the earnings selloff sparked a breakdown at the ascending wedge. The share price gapped below the 25-SMA (green line), 50-SMA (blue line), and 100-SMA (orange line). Support was eventually found at $156.04, and with the pre-market movement on Friday edging higher, there could be a recovery in an attempt to retrace some of Thursday’s losses.

If the market opens higher and moves toward resistance at $159.12, a retracement could occur. The first hurdle could then be the 100-SMA at $160.31 before meeting the shorter-term moving averages around $163.24. This resistance could be challenging to exceed, as the 50-SMA and 25-SMA could hold sellers to push the price back down.

Conversely, a breakdown below $156.04 in the Friday session could confirm the sustainability of the gap down, bringing the demand zone close to $154.09 into play. The Fibonacci midpoint and golden ratio from the mid-November peak would then come into the equation at $153.09 and $149.11 in the longer term. However, the estimated fair value lies at $167.69, offering a 7.5% potential upside from current levels, which could stretch if additional breakdowns at the current support take place.

Fundamental

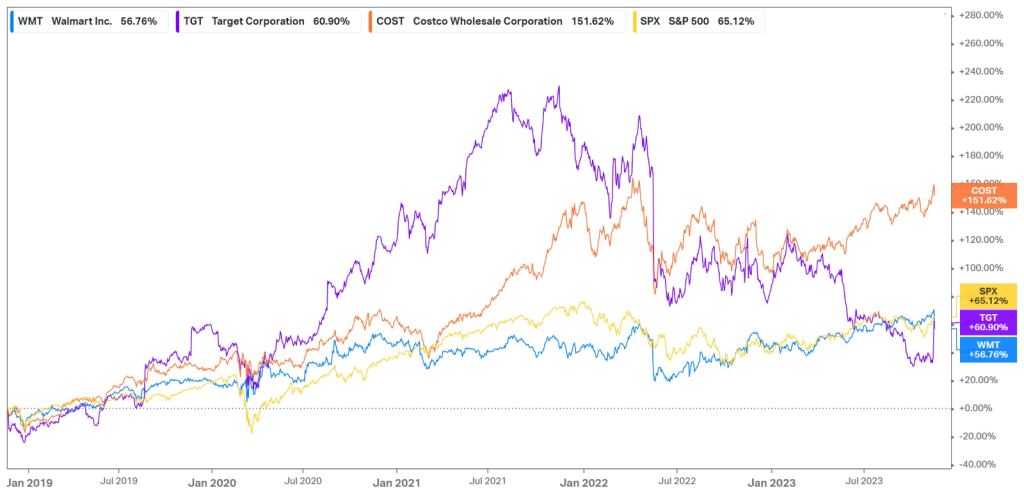

Walmart’s shares reached an all-time high earlier this week, but its share price performance over the last five years has not necessarily been smashing it out of the park. However, the nature of Walmart is such that it is a mature, low-margin business that does not necessarily hold the most potential for rapid share price appreciation but contributes to an overall portfolio’s risk-return attributes due to its stability in the face of volatility. Over the last five years, it has returned just under 57% in terms of share price appreciation, which underperforms all of its competitors, and the S&P 500, which returned over 65% during the same period. However, as seen in the chart below, these returns came with much less volatility. Especially over the recent year, when consumer inflation has constrained the consumer’s budget, the company has provided investors with safety due to its ability to pass rising input costs onto consumers and its portfolio that relies primarily on staple items, providing profit stability in a challenging environment.

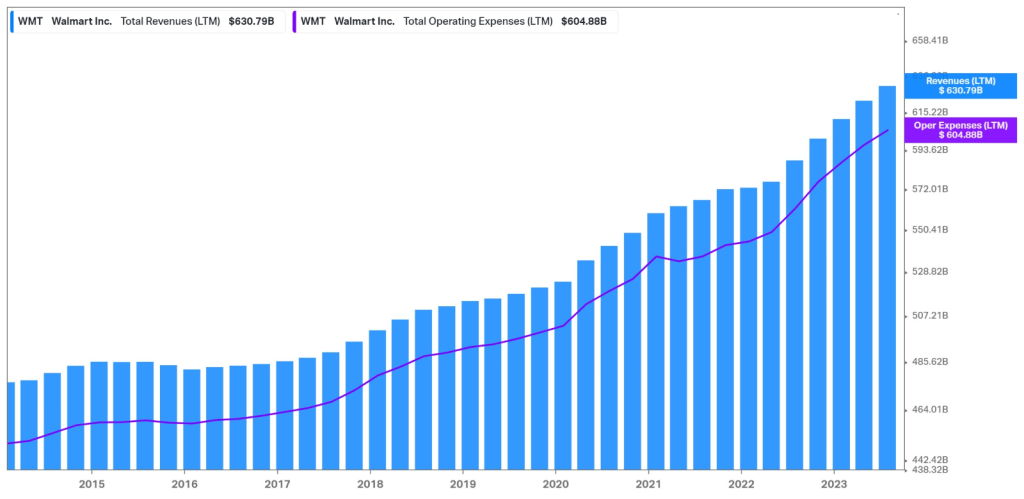

The graph below shows the company’s stable growth in revenue over the last ten years. As expected, the operating expenses grew at a similar rate. However, the concern among investors now lies in the fact that management mentioned that the company may be managing a period of deflation in the months to come. While this may be an optimistic development for consumers, it could weigh on the company’s top line as prices on its baskets of goods fall. While expenses will also decline eventually as input costs fall, it may happen with a lagging effect, which could strain its margins in the upcoming quarters, as its revenue falls at a quicker rate than operating expenditures. Additionally, management struck a cautious tone in addressing the consumer’s health, as they continued to gain shoppers in the latest quarter, but the amount spent per visit grew at a slower pace than in previous quarters.

Nevertheless, Walmart reported healthy earnings, as revenue grew by 5.2% to $160.8Bn, reflecting strength across all of its operating segments. eCommerce net sales were up by 15%, led by pickup and delivery, while its US comparable sales saw a 4.9% incline, reflecting strength in grocery and health & wellness, which were partially offset by weaker performance in general merchandise. The strong top-line performance trickled over into its bottom line, where its operating income was up by 130% at $6.20Bn. However, despite raising its guidance on both its top and bottom line, investors were disappointed with management’s outlook. The full-year guidance for EPS was raised from $6.36 – $6.46 to $6.40 – $6.48, falling at the lower end of the market’s $6.50 consensus.

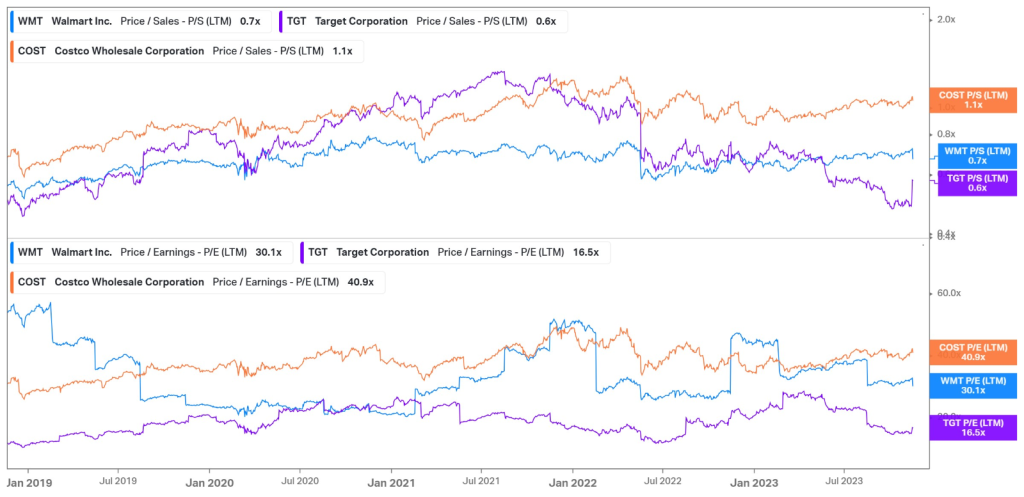

Looking at the company’s valuations, it becomes evident that Walmart is relatively fairly priced based on industry multiples. Its Price/Sales ratio of 0.7X falls in the middle of its industry peers, similar to the Price/Earnings ratio of 30.1X. Costco trades on higher multiples, which could reflect a higher expectation for growth due to the company’s slight discretionary tilt, which could boost sales and margins when prices start to contract, which it seems to be doing now. Walmart, on the other hand, trades slightly lower due to its low margin and stable growth prospects but still trades at a premium against Target, which has lost massive value in the last twelve months.

Summary

Despite a double beat in its latest earnings report, Walmart’s shares dropped over 8% on Thursday as a cautious outlook surrounding consumer spending dented investor sentiment. However, with the pre-market movements tilting in the bullish favour, we could witness a retracement in the Friday session, with resistance at $159.12 a key level to look out for as we advance.

Sources: Koyfin, Tradingview, Reuters, Walmart Inc.

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.