As the curtain rises on another thrilling earnings season, Wells Fargo (NYSE: WFC) steps into the spotlight with a performance that truly commands attention. This financial juggernaut has delivered a dazzling double triumph, leaving audiences in awe. The company has skillfully navigated a challenging monetary landscape with grace and finesse, reaping the rewards of increased net interest income.

Yet, amid this symphony of success, a subtle note of caution resonates. A shadow looms over the stage as Wells Fargo grapples with a shrinking deposit base, casting a hint of uncertainty on the horizon. For some consumers, the path to repaying their loans seems to be a bit more challenging. As we advance, the question arises: Can Wells Fargo’s star continue to shine brightly in this ever-changing financial landscape, or will the market’s return to normality test their mettle and resilience?

In the latest quarterly report last week, Wells Fargo reported a 7% revenue increase toward $20.86Bn, easing past the $20.07Bn consensus. The top-line beat trickled through to the profitability, resulting in a surge in earnings per share (EPS) from $0.86 to $1.48, shattering the $1.24 forecast.

Technical

On the 1D chart, a descending channel is present, with the recent formation of a death cross fuelling the trend, as the 200-SMA (orange line) crossed above the 50-SMA (blue line). However, the recent earnings report enticed an optimistic gap up in the share price, where the 25-SMA (green line) now offers resistance close to $40.96.

Following the 3% surge on Friday, the 50-SMA resists the upside, converging with the Fibonacci midpoint and dynamic resistance of the downtrend at $41.81. This could prove a psychological resistance, where a pullback within the channel may occur toward $40.52, the 61.8% Fibonacci golden ratio. If support is not found at this level, the channel trend could continue toward $38.42 and $37.18, with neckline support established at $35.98.

However, should the buying pressure enforce a breakout at the $41.81 resistance, a sustainable uptrend can form if the price clears the $43.64 resistance. The estimated fair value of $48.60 could then come into play if the supply zone close to the previous peak fails to halt the momentum at $47.27. This provides a lucrative 18.6% potential upside from current levels.

Fundamental

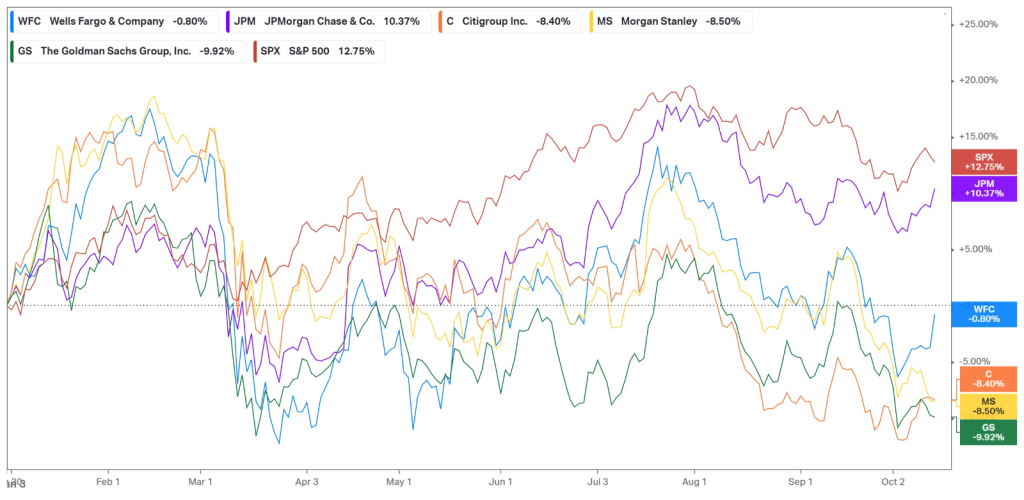

It has been a turbulent year for the banking sector, with the failure of Silicon Valley Bank igniting a banking crisis that hit the smaller US banks, causing multiple failures. Since then, the major banks have shown resilience, with the benefit of higher interest rates filtering through to the share price performance. However, with the volatility in the macroeconomic environment causing uncertainty, the sector has been up and down, as lower deposits and rising credit risks have offset the net interest income benefits. With management of major players in the industry acknowledging that the current top-line performance might not be sustainable, investors have been weary of pushing the valuations too far, as a possible pullback in the financial sector seems inevitable. Year to date, Wells Fargo has been relatively flat, underperforming relative to the broader S&P 500 (12.75%) and industry leader JPMorgan (10.37%).

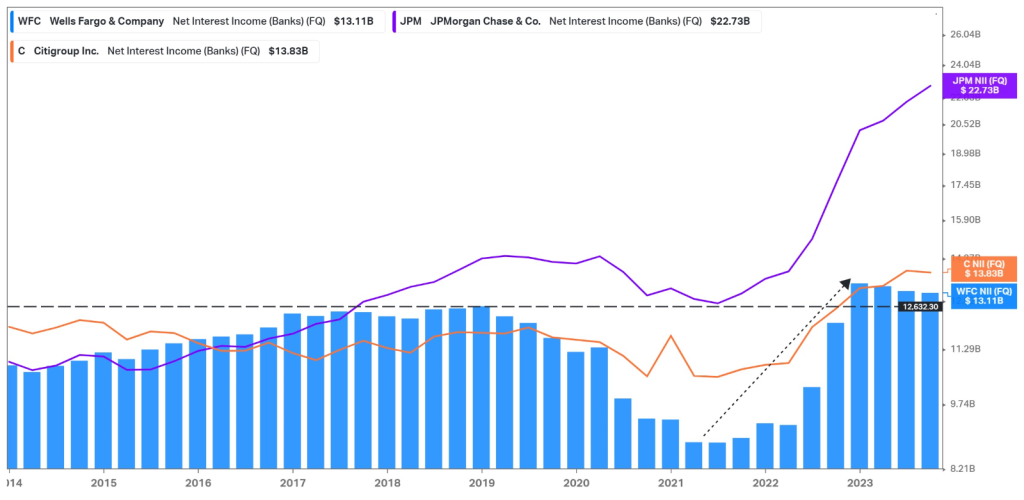

The recent surge in net interest income is shown in the graph below, as the top line had picked up significantly since the drop during COVID-19 when interest rates were historically low. In the latest quarter, Wells Fargo’s net interest income advanced by 8% year over year to $13.11Bn, resulting in consistent performance above its historical highs during the 2018 and 2019 financial years. If the Federal Reserve opts to enforce a dovish tilt on the monetary environment as we advance, we could see some mean reversion back to historical levels, which could result in a large top-line pullback. However, management is aware of this potential and has positioned itself to navigate any potential outcome in the macroeconomic environment in upcoming quarters. Its non-interest income also displayed strength, rising by 4% to $7.75Bn, with trading revenue and investment banking fees attributing most of the expansion. Corporate and Investment Banking revenue was up 21% at $4.92Bn, while its Commercial Banking rose by 15% to $3.41Bn. Similarly, Consumer Banking and Lending revenue increased by 3% to $9.58Bn. Finally, its Investment Management segment realized 1% growth, coming in at $3.7Bn to round off a well-balanced quarter away from its net interest income performance.

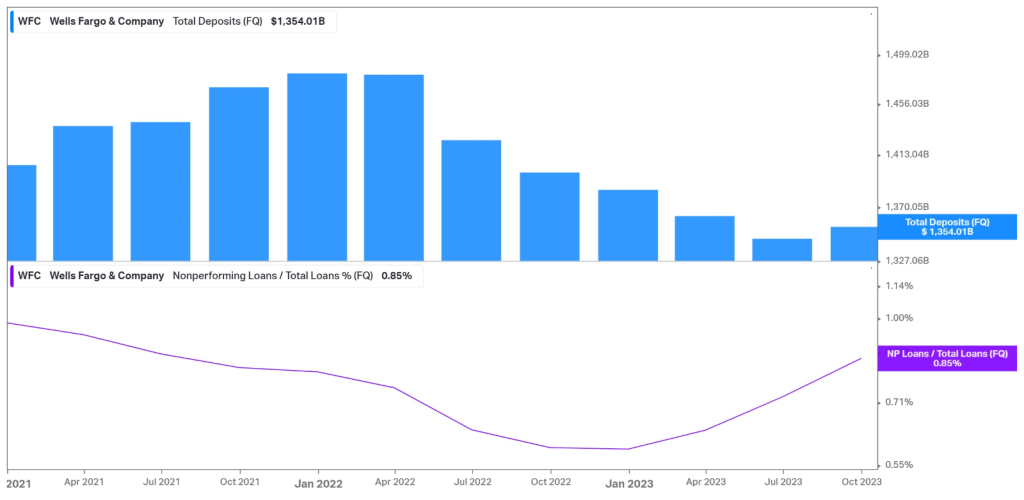

However, the graph below depicts a worrying visual. While the high-interest rate environment benefits its top line, the company’s deposits are slowing down every quarter. With lower deposits, the bank has a lower potential to issue loans, which could weigh on its top-line performance as we advance. In the latest quarter, its average deposits declined from $1.41Bn to $1.34Bn, resulting in a contraction of average loans from $945.4M to $943.2M. Additionally, the higher inflation and interest rates have strained the consumer’s budget, resulting in a larger proportion of the bank’s loans being nonperforming. In the recent quarter, its net loan charge-offs reached $850M, representing 0.36% of its average loans, which is a stark increase from the year-ago $399M, which represented 0.17% of its average loans. While the proportion of nonperforming loans to total loans remains relatively low at 0.85%, it is ticking up quarter by quarter from 0.6% earlier in the year, and we could soon reach an inflexion point, where the rising interest rate environment could result in credit losses on its loan book that outweigh its interest income benefits.

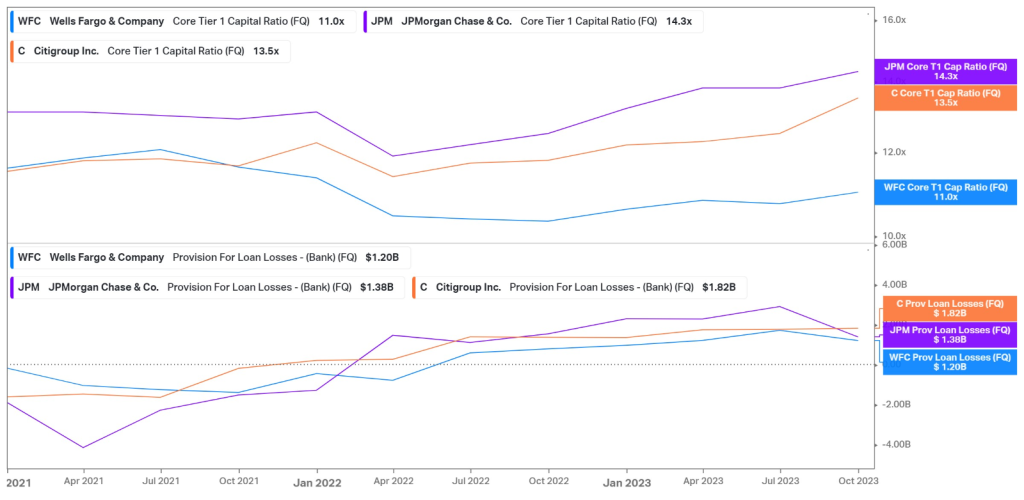

Despite the higher risk of its loans not being repaid, Wells Fargo remains resilient in its balance sheet health. Its core tier 1 capital ratio, while the lowest among its peers, remains far above regulatory requirements at 11%. It maintains sufficient capital to cover its obligations and holds the lowest provision for credit losses, which recently surged from $784M to $1.2Bn, and includes a $333M increase in allowance for credit losses attributed primarily to commercial real estate loans. With lower credit provision expenses, the company maintained a healthy bottom-line expansion, showing strength in its ability to maintain profitability, while preserving its solid balance sheet.

Summary

Wells Fargo reported a healthy double beat in its latest earnings report, as major US banks continue to benefit from higher interest rates. However, with the increasing risk of nonperforming assets and credit losses clouding its outlook, investors are maintaining caution in anticipation of macroeconomic developments. As we advance, clearance of resistance at $41.81 could open a path to convergence with its estimated fair value of $48.60, representing an 18.6% potential upside from current levels.

Sources: Koyfin, Tradingview, Yahoo Finance, Investor’s Business Daily, Reuters, Wells Fargo & Company

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.