In the retail ring’s latest round, Costco Wholesale Corporation (NASDAQ: COST) packed a profit punch that reassured its investors of its ability to weather adversity. This retail titan has proven once again that it’s the master of delivering unbeatable value, providing shoppers with a shopping cart full of savings in a challenging economic landscape. While some market watchers exhibited a raised eyebrow regarding unchanged membership fees, the company seems poised to keep its winning streak alive in the coming financial quarters.

Revenue for the quarter amounted to $78.94Bn, advancing from the $72.09Bn in the year-ago period while exceeding the market’s forecast of $77.96Bn. Similarly, its bottom line advanced from $4.20 in earnings per share (EPS) to $4.86, easing past the $4.78 consensus. While facing numerous headwinds, such as higher interest rates and the resumption of student loan repayments, the company’s value proposition has left it well-positioned to navigate the uncertainty.

Technical

On the 1D chart, an ascending triangle has formed, as the share price has failed to breach the critical resistance at $568.10 to continue its upside momentum. While the 50-SMA (blue line) trends above the 25-SMA (green line), the bears have the upper hand, but the strong recovery from Wednesday’s lows has left the share price above the daily pivot support at $555.44, suggesting the intraday momentum favours the upside.

Resistance at $564.81 (R2) is currently preventing the share price from retesting the psychological triangle resistance at $568.10, but a breakthrough above these levels could send the price toward $571.80. Breaching this level could confirm the continuation of the prior uptrend, opening a path to convergence with its estimated fair value of $585.04, which presents a 4% upside from current levels.

However, if resistance at R2 caps the upside, a pullback toward $551.63 could trigger a breakdown at the dynamic triangle support. Lower support is established at $546.07 (S2) and $541.53 before a potential move below the 100-SMA (orange line) could signal longer-term bearish momentum. A sustained downtrend could reach $511.25, where the potential upside to the estimated fair value reaches an enticing 14.4%.

Fundamental

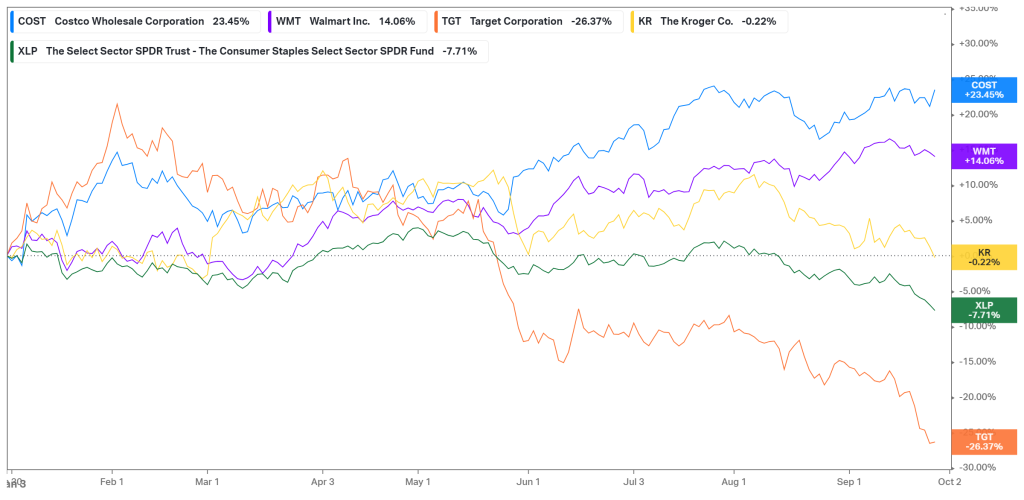

Year-to-date, Costco has returned 23.45% to its shareholders in the form of price appreciation, exceeding both the broader consumer staples sector (-7.71%) and all of its competitors within the industry. Costco and Walmart (14.06%) provide value alternatives that have attracted shoppers in a period of high interest rates, where customers had no choice but to tighten their belts on spending. Trading down to more affordable options has seen Costco and Walmart grab market share from other retailers with a more discretionary tilt, resulting in their outperformance so far this year. However, with inflation easing and the Federal Reserve potentially nearing the end of its hiking cycle, industry conditions could soon return to normality, where customer retention will become vital in the forward-looking performance of the company.

For the full fiscal year, Costco reported net sales of $237.71Bn, up 6.7% from the $222.73Bn generated in 2022. Comparable sales advanced 3%, led by a 3.3% expansion in its main geography, namely the US, and a 2.8% rise in its other international segments. Net income for the year amounted to $6.29Bn, up from the prior $5.84Bn, which translates into $14.16 earnings per diluted share, a strong improvement from the $13.14 generated in the previous year. However, e-commerce sales declined by 0.8% for the quarter and 5.7% for the whole year as the company continues to face headwinds in that division.

The graph below demonstrates the company’s strong positioning in the industry, as it operates with the highest inventory turnover ratio (12.3x) among its peers. Costco has done well to attract customers to its stores, resulting in a more streamlined process of getting rid of its inventory. The higher turnover reflects the company’s increased efficiency in selling its merchandise. In the latest quarter, foot traffic increased by 5.2% as more customers flocked to the company’s value alternatives. However, there were declines in some big-ticket discretionary categories, which resulted in a lower average ticket size, which decreased by 3.9% in the last three months of its financial year. If the company can retain the customers it has accumulated in the upcoming quarters, normalization in the interest rate and inflation environments could aid the recovery in its ticket size, presenting an attractive opportunity for its continuous top and bottom-line growth.

One strategy the company has employed to retain its customers is its subscription-based model. Costco last raised its membership fees in June 2017, with a Costco Gold Star membership costing $60 per year and an Executive Membership costing $120. Many investors expected an increase in the membership fees in the latest report, but management opted to keep the fees unchanged for now. Membership fee revenue for the latest quarter amounted to $1.51Bn compared to the $1.33Bn in the same quarter last year. Annually, membership revenue increased from $4.22Bn to $4.58Bn, with the company having 71M paid household members, up 7.9% from last year, while boasting 127.9M cardholders, also increasing by 7.6% from the year-ago period, showcasing the customer loyalty that Costco has built up over the years.

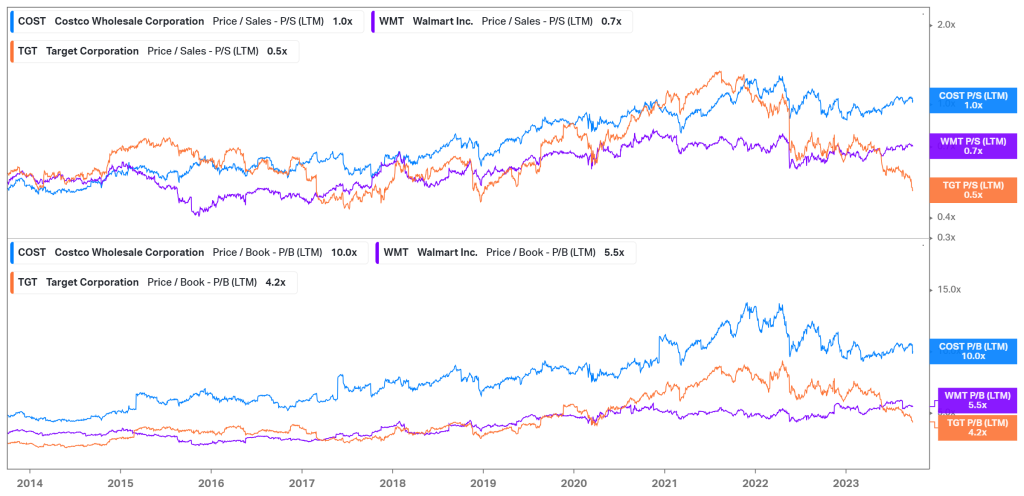

Despite the competitive positioning the company has built up within the industry, Costco remains slightly overvalued relative to its industry peers. With its share price advancing prosperously this year, its Price/Sales ratio of 1.0X has diverged from Walmart (0.7X) and Target (0.5X). Similarly, its Price/Book ratio of 10.0X trades almost twice as high as Walmart (5.5X) and Target (4.2X). While the company’s performance has been strong and possesses an economic moat in the industry, its valuations have stretched, as it costs more per unit of sales than its peers. Whether this premium on the share price is justified remains up to the discretion of the individual investor.

Summary

After posting solid results in its latest earnings report, Costco’s value proposition has placed it well in the industry regarding the current macroeconomic backdrop. With a potential increase in its membership fee offering an additional tailwind to its revenue stream, the estimated fair value of $585.04 remains well within reach, presenting a 4% potential discount at the current level.

Sources: Koyfin, Tradingview, Yahoo Finance, Reuters, Costco Wholesale Corporation

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.