With the hotly anticipated release of the live-action Barbie movie sending excitement soaring, it’s time to dust off your fashion-forward thinking caps and get ready for a show-stopping surge in demand for the iconic dolls produced by Mattel, Inc (NASDAQ: MAT). As Barbie sashays her way into the limelight, watch how Mattel turns playtime into pay time, leaving shareholders and doll lovers alike feeling like Hollywood royalty. On top of that, the company will release its quarterly report next week in another blockbuster event that has investors itching with excitement.

After taking the reins in 2018 as the fourth CEO in four years, Ynon Kreiz faced a challenging landscape after the Toys R Us bankruptcy caused a sales slump and a slowdown in demand for Mattel’s toys. But Kreiz saw the silver lining, recognizing Mattel’s potential as a children’s-entertainment powerhouse rather than a toymaker, potentially rivalling Disney. Inspired by Marvel’s Hollywood triumph, he charted a new course, shifting from a toy manufacturer to an intellectual property (IP) powerhouse, destined to dominate the cinematic experience and spark a remarkable comeback story.

Technical

On the 1D chart, the share price has been under intense bullish pressure in recent weeks, triggering a breakout from the ascending channel. While the daily pivot point at $21.15 offers resistance to the upside, the momentum remains firmly under bullish control, with the share price trading above the 50-day moving average.

If the pivot point holds, the market could correct the recent rally to retest the breakout point at $20.29. A move lower could trigger a channel continuation, where lower support is established at $19.26. if the downward momentum persists on disappointing earnings, the channel support could become vulnerable to a breakdown toward $17.42.

However, a breakout at the pivot could see the upward momentum test the $21.61 level. From there, higher resistance at $22.10 (R2) could provide the final barrier to convergence with its estimated fair value of $23.79, presenting an 11% potential upside from current levels.

Fundamental

Mattel’s Q1 2023 earnings report, unveiled on April 26th, showcased both challenges and opportunities. Despite reporting a loss per share of only $0.24 and revenue of $814.6M, which surpassed estimates, the company faced a decline in both top and bottom lines due to retail headwinds and inventory challenges. Barbie brand’s gross billings plunged 41% YoY to $176.9M, impacting the gross margin, which shrank from 46.6% to 40%, resulting in a net loss of $106.5M for the quarter. Nonetheless, CEO Ynon Kreiz emphasized the company’s resilience as it grew market share globally in key categories – Barbie, Hot Wheels, and Fisher-Price. Encouraged by this strength, Mattel’s management expressed optimism by reiterating full-year guidance of $1.25 EPS with a 47% gross margin and expected free cash flow above $400M.

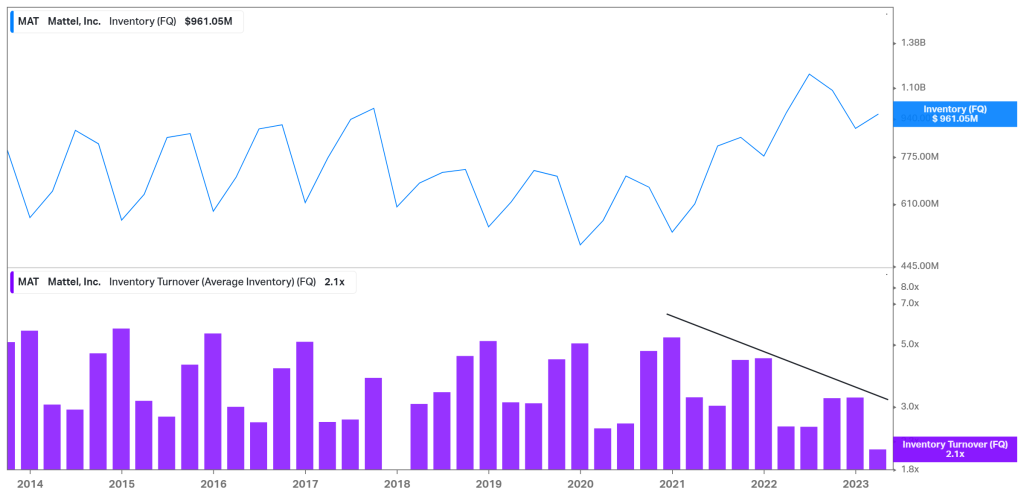

Inventory management has emerged as a significant challenge hindering the company’s growth, as depicted in the graph below. Despite experiencing higher turnover during holiday seasons, the overall trend has declined, raising concerns about lower turnover peaks in crucial quarters. In the latest quarter, turnover stood at 2.1X, indicating difficulties in clearing excess inventory. Nevertheless, a glimmer of hope shines through as the company reported a recent inventory decrease in Q4 2022, with management optimistic about rising consumer demand for their products moving forward.

Unsurprisingly, Barbie falls at the centre of the optimism. However, while remaining among the firm’s top three revenue drivers, the demand for Barbie products has been on the decline. In the latest quarter, gross billings slumped 41% from $298M in the second quarter of 2022 to $176.9M. However, Mattel has deferred the majority of its marketing to the months preceding the movie launch and, as such, predicts an improvement from the Barbie brand in the second quarter and full year. Management expects total sales to be in the range of $5.4Bn, implying growth in the upcoming quarters. With regard to Barbie sales, Mattel generated $1.5Bn in revenue last year. Compared to the $1.2Bn generated in 2013, the brand’s growth is a concern. However, with a new strategy pivoting around intellectual property over toys, the runway for growth is evident.

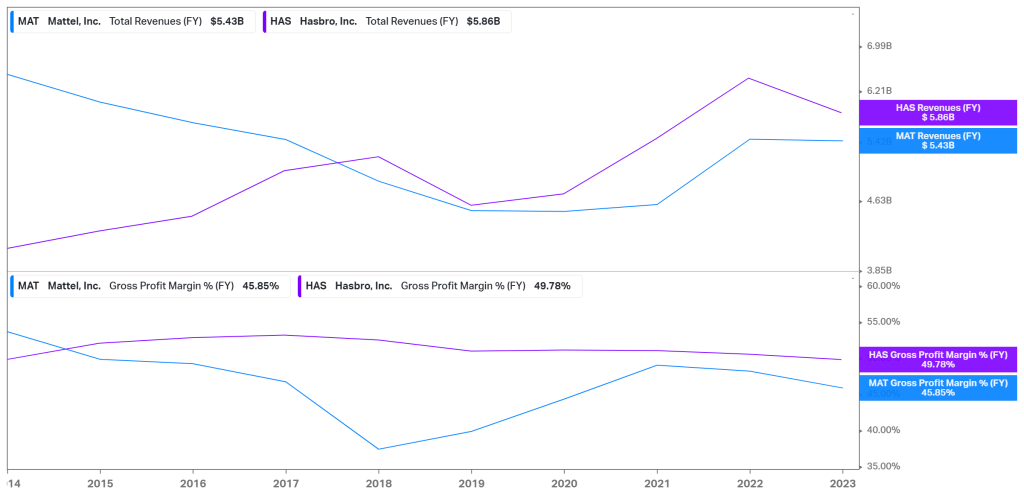

The company’s strategic efforts to clear excess inventories have ignited curiosity about its margins. An eye-opening graph shows a fascinating contrast between soaring top-line growth and the pressures on gross profit margins. While revenues have shown steady progress over the years, the same can’t be said for margins, which have felt the strain, with a notable slide from 46.6% to 40.0% in the latest quarter. The culprit? Inventory management costs, claiming 4.2% of that decline. As we eagerly await the next quarterly release, all eyes are on inventories and margins, especially with the Barbie doll demand resurgence poised to work its magic on the bottom line.

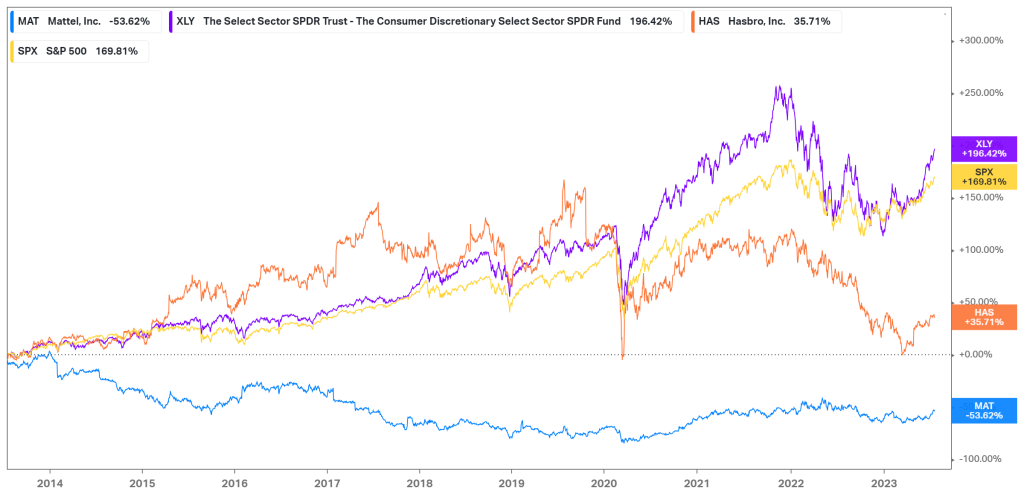

Over the past decade, Mattel may have returned a lacklustre -53.62%, lagging behind the surging S&P 500, while the consumer discretionary sector saw a jaw-dropping 200% expansion. A tough pill to swallow for investors, indeed! But hold on to your Barbie dolls because things might be turning around. Amidst a recent Barbie craze and a clever inventory strategy, a remarkable 20% resurgence since June has caught everyone’s attention. Could this be the dawn of a new era for the toymaker? As excitement fills the air, the question remains: Is this just market chatter, or is there a long-term growth story brewing under the surface?

Upon this new era, the company charts a fresh path to growth and toy sales with a groundbreaking potential for a Mattel Cinematic Universe featuring an array of beloved IPs. This visionary move extends beyond making toys based on popular movies to creating epic cinema adventures from its iconic brands like Hot Wheels, Masters of the Universe, and American Girl. With Barbie leading the charge under the brilliant direction of Greta Gerwig, industry analysts foresee box office success, with predictions soaring up to a dazzling $400M. Beyond toy aisles, this bold strategy ventures into the captivating realm of entertainment, unlocking the untapped value within their extensive IP treasure trove.

Summary

As we eagerly await the grand premiere of the Barbie movie, the spotlight now shifts to Mattel’s latest quarterly performance. Should their inventory management and margins show a positive turnaround, signalling a surge in demand for Barbie products, it’s a clear sign that the ingenious Mattel Cinematic Universe is set to create a dreamland for investors. In this case, the estimated fair value of $23.79 whispers of a delightful 11% potential upside from where we stand today.

Sources: Koyfin, Tradingview, The New Yorker, Statista, Mattel, Inc.

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.