Pick n Pay Stores Limited (JSE: PIK) made headlines this week with an announcement that left investors and industry experts discouraged. For the very first time in the company’s history, they reported an interim loss for the period ending on August 27, 2023. The sombre tone set by the management, who labelled these results as ‘disappointing,’ cast a shadow over the company’s future. As a consequence, the company’s share price took a significant nosedive.

In the aftermath of this stunning revelation, the company’s shares plummeted by a staggering 13%, leaving shareholders and analysts grappling with a harsh reality. The confluence of inflationary pressures, mounting operational costs, and an increasingly competitive landscape cast a daunting shadow over the company’s future prospects. Despite a respectable 5.4% growth in turnover, Pick n Pay Stores Limited faced a dire predicament as its trading profit nosedived by a staggering 97.5%. The impact was painfully evident, as the pro forma headline loss per share skyrocketed to a daunting 129.30 cents, a significant 245.7% drop from the previous period’s 88.76 cent profit. To make matters worse, the company’s decision to withhold dividends only fueled further discontent among its shareholders, triggering a severe sell-off that sent its share price into a free fall.

Technical

On the 1D chart, a steep downtrend has left the share price scrambling, with the recent selling pressure adding to the recent downturn. The 100-SMA trades above the 50-SMA and the 25-SMA, confirming the bearish sentiment, as the price looks toward support at R24.88.

If the price reaches this support level, a retracement is on the cards to reverse the recent leg down. However, a breakdown at R24.88 could see a test of the 161.8% Fibonacci extension at R23.89. Since the price is already close to multi-year lows, a move below this support could send the price plummeting further toward neckline support at R19.43.

However, if the price remains above R24.88, a retracement toward the dynamic channel support is on the cards, where resistance at R30.98 could come into play. The estimated fair value on a discounted cash flow basis is R32.05, representing a 23.4% potential upside from current levels if the company reverses its recent fortunes.

Fundamental

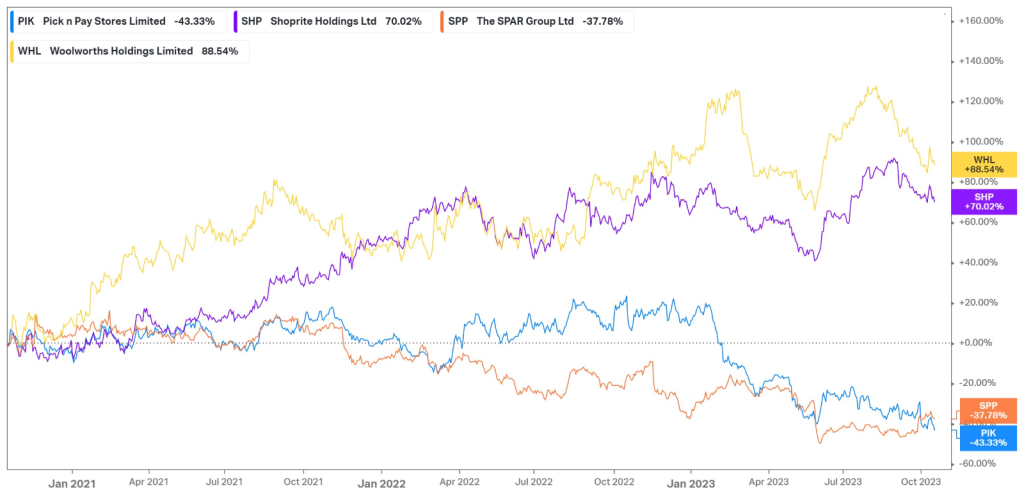

It has been a challenging couple of years for South African retailers, and 2023, in particular, has proved no different. Food inflation reached its highest level in fourteen years in March at 14%, while interest rates have reached their highest level since 2009. As a result, the consumer has been under severe pressure, with this pressure filtering through to the retailers. On top of this, record levels of load-shedding have pressured the bottom line due to increased costs to keep generators running. Pick n Pay, in particular, has dealt with its own set of headwinds, as massive underperformance in its core business has not met expectations. As a result, its former CEO Pieter Boone stepped down from his role less than two and a half years after starting, as the company feels a change in leadership is necessary to get the retailer back on track. Due to the combination of these headwinds, the company has lost over 43% in value over the last three years. In contrast, competitors like Shoprite, with its value alternative offerings, and Woolworths, with a more resilient consumer base, have stolen some market share, resulting in a 70.02% and 88.54% share price appreciation over the same period, highlighting the competitive landscape in the industry, in which Pick n Pay has fallen behind.

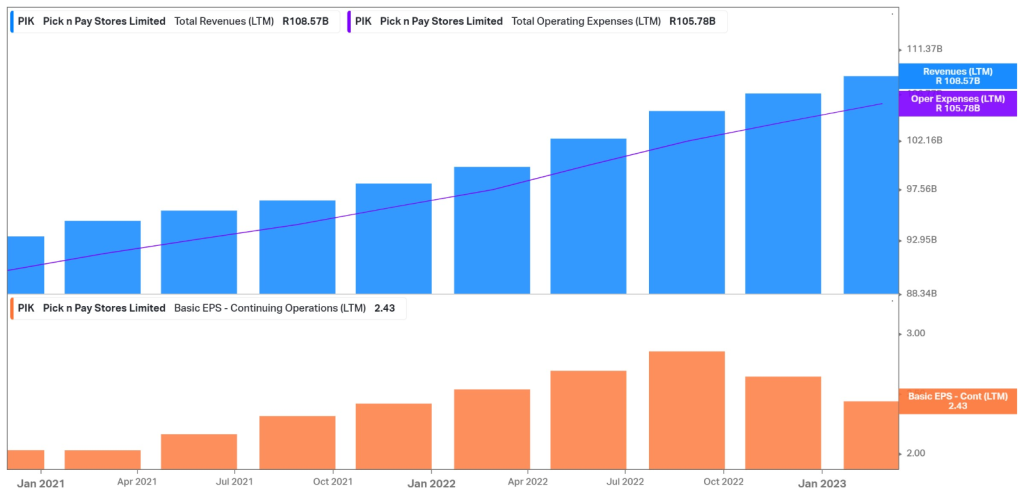

The graph below shows the company’s revenue for the latest twelve months leading up to the latest interim report. Evidently, its top line is hardly the problem, as it has been growing year over year. The issue is, however, the operational expenditures that are increasing at a faster pace, which has caused a subsequent reduction in its earnings per share over the last few years until it has recently swung into loss territory. For the latest interim period, the group’s turnover increased by 5.4% to R54.1Bn, mainly driven by Boxer, South Africa’s leading soft discounter, which advanced 16.1% to R17.38Bn, adding 27 new stores to its portfolio of 454 Boxer stores, which now contributes 33% of the company’s top line. Pick n Pay Clothing grew 13.8% from its standalone stores and opened 20 new company-owned stores, while online sales on its asap! and Pick n Pay groceries platform on the Mr D app grew 76.3%.

However, trading expenses were up by 13.7%, contributing to the massive fall in trading profit from R1.25Bn to R31.8M. Included in this was R565M in abnormal costs, which include R259M in employee restructuring costs, R190M net incremental energy costs, and R116M in supply chain costs. Excluding these costs, trading profit for the period would have been R596.8M, which is still a stark contraction from the prior period. Additionally, expenses related to load shedding remain one of the biggest cost challenges facing the company, as it spent R396M on diesel to keep its generators running during power outages after spending R652M in the prior financial year.

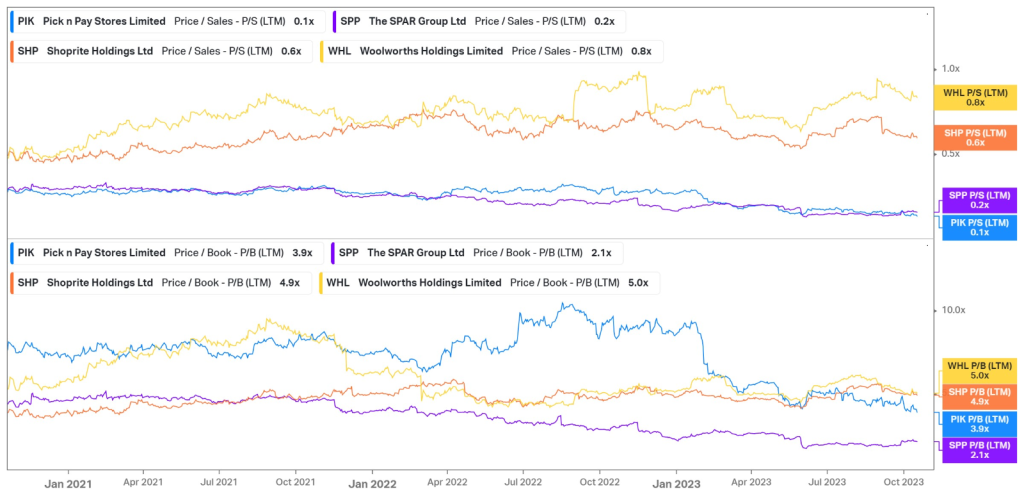

After its significant share price depreciation over the last few years, one would expect a lower valuation on the company’s share price, especially considering the current headwinds. Its Price/Sales (P/S) multiple is currently at 0.1X, reflecting relative undervaluation compared to its industry leaders, such as Shoprite (0.6X) and Woolworths (0.8X). Similarly, its Price/Book multiple of 3.9X falls below Shoprite and Woolworths but reflects a slight overvaluation relative to Spar (2.1X). With the group appointing Sean Summers, who previously led the group through a very successful period, as the new CEO, there could be a potential opportunity inherent in the current share price if the leadership change can return the company to its previous success.

Summary

After delivering a disappointing interim earnings report, which resulted in a discontinuation of its dividend payments, Pick n Pay’s share price faltered by over 13%. However, with new leadership taking over and the holiday sales period edging closer, there could be a potential opportunity at a lower valuation, with the estimated fair value of R32.05 offering a 23.4% upside potential from current levels.

Sources: Koyfin, Tradingview, Reuters, BusinessDay, Pick n Pay Stores Limited

Pieces written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.