In a headline event last week, the leading food producer in South Africa, Tiger Brands Limited (JSE: TBS), has created waves of excitement with its recent announcement. Noel Doyle, who has steered the company for the past three years, has decided to pass the torch, opening the door for a new era under the capable guidance of Tjaart Kruger, the former CEO of Premier Foods. This decision sent ripples through the market, with the company’s share price surging by an astounding 11%. Investors are showing their faith and optimism in this change, seeing it as a breath of fresh air that could potentially revitalize a company that has been navigating the turbulent waters of the domestic food and retail industry.

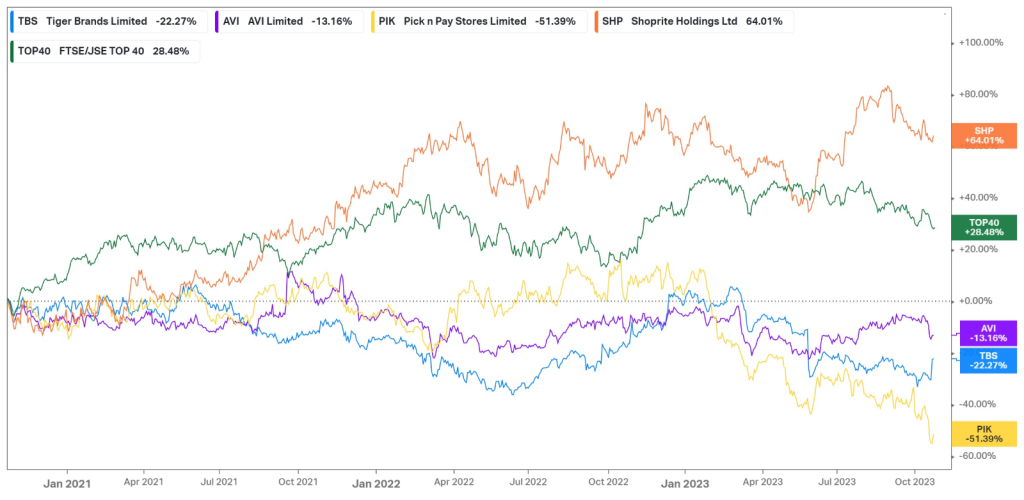

Over the last three years, Tiger Brands has suffered a 22% contraction in its share price, with similar performances seen across the board in the food and retail industry. Pick n Pay, which reported its first interim loss in its recent earnings report, has faltered over 51% over the same period while also bringing in new management, in the shape of their former CEO Sean Summers, to try and turn their fortunes around. This development highlights a trend in the industry as companies look toward experienced management teams to guide them through the challenges posed by civil unrest, record-high unemployment, a rise in the cost of living, and increasing prices of raw materials. Additionally, the increasing amount of power blackouts is pressuring the bottom lines of retailers and food producers, as they spend billions of rands to mitigate the impact of the daily power blackouts. So, where to from here for Tiger Brands?

Technical

On the 1W chart, the share price peaked at a psychological supply zone close to R224.03, where a retracement past the 61.8% Fibonacci golden ratio of R170.37 has led to the price bottoming out at R147.57. The announcement of the management change triggered a trend reversal, with the share price breaking through the channel resistance as it looks to retrace the recent downturn.

The 25-SMA (green line) supports the upside, with the R170.37 resistance nearing. If this resistance gets cleared, the 100-SMA (orange line) could offer additional resistance before the price can reach the prior Fibonacci midpoint of R181.54. With the estimated fair value at R192.40, clearing this resistance could trigger the convergence, providing a 15.8% potential upside from current levels.

However, this ascent could be delayed if the resistance at R170.37 prevents additional upside. A retracement of the breakout could occur toward the R147.57 level, where the initial buying pressure was triggered. In that case, a lack of support could send the price to the neckline resistance at R133.84 in the longer term.

Fundamental

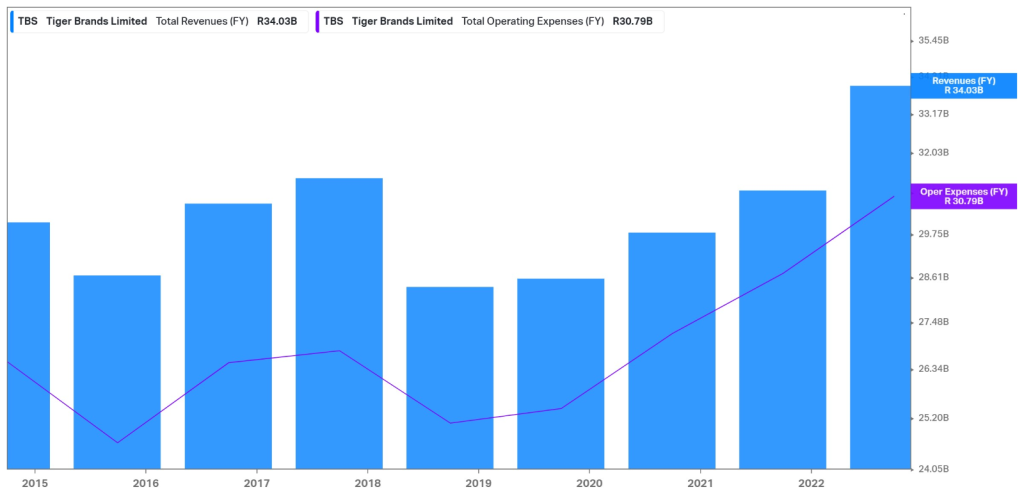

The high inflationary environment in South Africa has drastically increased the input costs for food producers and retailers in South Africa. While Tiger Brands reported a 16% rise in revenue toward R19.4Bn in its latest interim report, the top-line growth was driven by price inflation of 17%, with its purchasing volumes contracting by 1%. As the company attempts to pass the rising input costs onto its consumers, its average basket sizes and volumes are declining. The company further admitted that its cost-saving initiatives were insufficient to counter the rising cost inflation. At the same time, a further R76M was spent in the six months leading up to the report to counter the effects of load shedding. As a result, the graph below shows a rising top line but an even stronger rise in operating expenses, which is preventing bottom-line expansion. As a result, its gross margins contracted from 29.2% to 27%, while its operating income decreased by 9% to R1.4Bn.

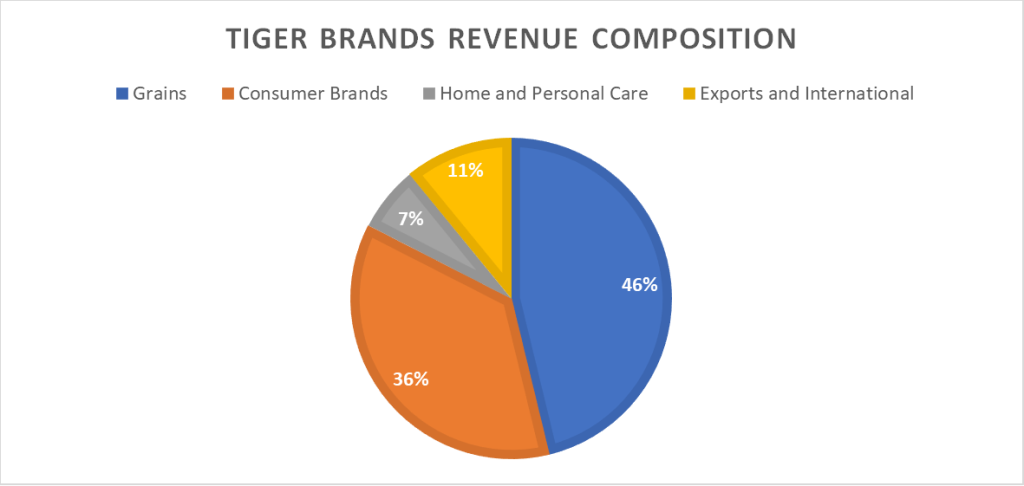

Looking at the revenue composition of the company, its main top-line generator is grains. In the latest interim report, this segment advanced its revenue by 22% to R9Bn, driven by price inflation of 22%, while volumes remained flat. The Consumer Brands segment, which includes groceries, snacks & treats, beverages, baby, and out-of-home products, showed strong performance across the board. Revenue was up 10%, with 10% price inflation and unchanged volumes, while snacks and treats outperformed after recovering from the impact of industrial action in the previous period. Total revenue in its exports and international segment was up 10% at R2.1Bn, with price inflation of 17% being backed by a 10% increase in volumes. Finally, its home and personal care segment, the smallest revenue contributor, increased by 16% to R1.3Bn, driven by strong performance in the personal care business, which increased by 33% to R372M, benefitting from both a 13% increase in price inflation and a 20% rise in volumes.

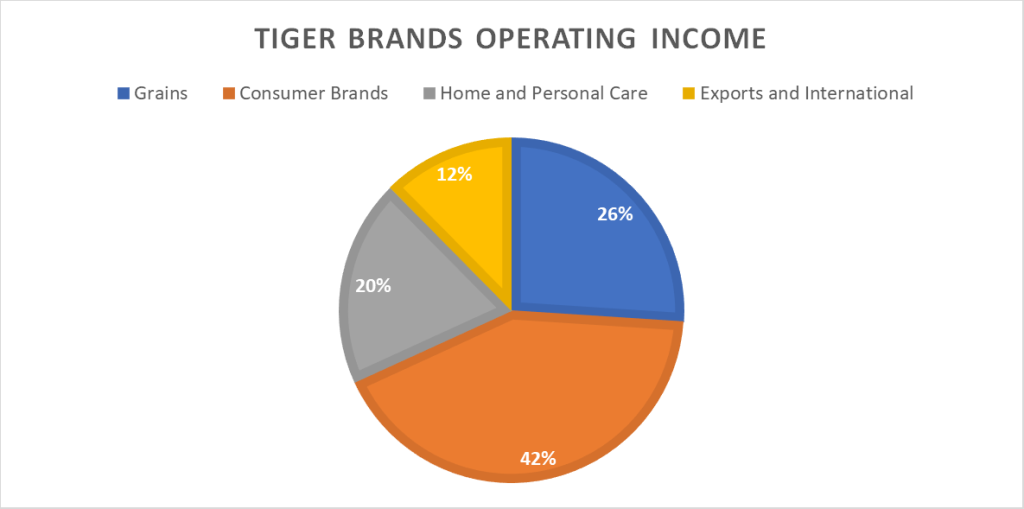

However, these segments did not contribute to the bottom line to the same extent as its revenue. While grains contributed the most to the top line, its operating income declined by 19% to R343M, as significant increases in raw material costs and conversion costs related to load shedding affected its profitability. Consumer brands contributed R555M to the company’s operating income but still suffered a 15% bottom-line decline, driven by underperformance in the grocery and baby segments. Enhanced factory performances allowed the home and personal care segment to expand its operating income by 21% to R256M, making it the third-largest contributor to the company’s bottom line in the latest interim period.

Summary

Despite reporting a 16% rise in revenue in its latest interim report, Tiger Brands faced multiple challenges that resulted in a 9% contraction in its operating income. As a result, its margins declined, with its operating margin falling from 8.9% to 7%, while its headline earnings per share (HEPS) remained relatively flat at 731 cents. As we advance, investors are optimistic that with new management at the helm, the company can rely on his experience and knowledge of the industry to navigate these headwinds more efficiently and reverse the company’s recent fortunes. The estimated fair value of R192.40 presents a 15.8% potential upside from current levels.

Sources: Koyfin, Tradingview, Reuters, Tiger Brands Limited

Piece written by Tiaan van Aswegen, Trive Financial Market Analyst

Disclaimer: Trive South Africa (Pty) Ltd, Registration number 2005/011130/07, and an Authorised Financial Services Provider in terms of the Financial Advisory and Intermediary Services Act 2002 (FSP No. 27231). Any analysis/data/opinion contained herein are for informational purposes only and should not be considered advice or a recommendation to invest in any security. The content herein was created using proprietary strategies based on parameters that may include price, time, economic events, liquidity, risk, and macro and cyclical analysis. Securities involve a degree of risk and are volatile instruments. Market and economic conditions are subject to sudden change, which may have a material impact on the outcome of financial instruments and may not be suitable for all investors. When trading or investing in securities or alternative products, the value of the product can increase or decrease meaning your investment can increase or decrease in value. Past performance is not an indication of future performance. Trive South Africa (Pty) Ltd, and its employees assume no liability for any loss or damage (direct, indirect, consequential, or inconsequential) that may be suffered from using or relying on the information contained herein. Please consider the risks involved before you trade or invest.